Retail sales dragged down by weather and LA fires

We thought a soft January retail sales report was likely given the cold weather and the Los Angeles fires, but it is worse than even our pessimistic forecasts.

Headline sales were down 0.9% month-on-month in nominal terms (consensus -0.2%) while the control group that excludes the volatile autos, food service, building materials and gasoline and supposedly better tracks broader consumer trends fell 0.8% (consensus +0.3%).

As these are nominal value changes and we know prices rose 0.5% MoM according to the CPI report, this implies very weak volume sales growth. It is the volume measure that feeds through into GDP growth.

Auto sales fell 2.8% MoM, largely because of a big unit volume drop, which we already knew about, while furniture dropped 1.7%, electronics fell 0.7%, health spending fell 0.3%, clothing down 1.2%, sporting goods dropped 4.6% and internet sales fell 1.9%.

Surprisingly, eating and drinking out actually rose 0.9% – we had expected this to drop because of very cold weather and there was a sense that the Los Angeles fires would also have a depressing effect, but somehow this was one of the very few sources of strength. (…)

Keep in mind that retail sales rose 7.4% annualized in Q4 after 5.4% in Q3. January’s softness is no big deal in this context.

On a YoY basis, sales were up 4.2% in January, the average of the last 3 months and up from 2.3% on average in the previous 3 months. Labor income (black) is up 5.0% in the last 3 months.

Bank of America data:

Consumer spending started 2025 on solid footing, following a strong end-of-year performance in 2024. Spending per household was up 1.9% year-over-year (YoY) in January, following the 2.2% YoY rise in December, according to Bank of America aggregated credit and debit card data. While on a seasonally-adjusted (SA) basis spending per household was down 0.4% month-over-month (MoM) in January, the three-month seasonally-adjusted annualized rate (SAAR) was up a solid 2.8%. (…)

According to Bank of America aggregated card data, the wintery weather in the South had the greatest impact on in-person retail spending throughout the region. While in-person retail spending growth in southern states was a full percentage point lower than the overall US, it appears many Southerners stayed at home and shopped online instead.

We’re Headed Toward a Landlord-Friendly Era. Expect Higher Rent Prices. Prospect of rising apartment rents could further stoke inflation and give the Fed another reason to pause

A spike in rents during the early years of the pandemic sparked a historic apartment construction boom in 2023 and 2024. That crush of new inventory, especially in hot Sunbelt markets like Austin and Phoenix, led to oversupply and caused rents to fall in much of the country.

But more people now are renting longer, as mortgage rates stay high and the costs of homeownership remain unaffordable for many Americans. Landlords say that the new construction pipeline should be mostly drained by year-end, setting the stage for rents to rise nationwide later this year. (…)

Rising rents would complicate the inflation picture and likely give the Federal Reserve another reason to pause on future rate cuts. Shelter costs account for roughly a third of the consumer-price index, which means that a significant portion of the overall inflation measure is attributed to housing costs. (…)

Shelter costs increased 4.4% in January from last year. That was the smallest annual uptick since January 2022, and well below the peak period of 2023, according to the Bureau of Labor Statistics.

Now, the looming prospect of higher rents could reverse that progress. Rents have already been on a steady climb in certain parts of the country where new supply has been more muted, such as the Midwest, Northeast and parts of the West Coast.

By the end of this year, every major metropolitan market is expected to see positive rent growth, said Jay Lybik, national director of multifamily analytics at CoStar.

President Trump’s policy mix, meanwhile, might slow the pace of new construction even further. Migrant deportations and threats to hit Canada and Mexico with tariffs would likely boost the cost of construction labor and materials as well as delay building timelines.

The U.S. depends on Canada and Mexico for roughly 25% of its building material imports, according to the National Association of Home Builders. And undocumented workers make up about 13% of the construction workforce. (…)

And demand for rentals is rising steadily. The multifamily vacancy rate is now below its long-term average for the first time in about two years.

More tenants are in heated battles for vacant space. Last year, an average of nine prospective renters were competing for every open apartment unit on the market, according to RentCafe. (…)

Multifamily asking rents are still trending relatively flat nationally, but they are headed upward. On average, apartments were three dollars more expensive nationwide in January, the first increase in six months, according to property data firm Yardi Matrix.

Apartment absorption, a metric of rental demand that measures the change in how many units are leased, was higher last quarter than any other fourth quarter since at least 1985, according to real-estate firm CBRE. (…)

SENTIMENT WATCH

Risk appetite slumps in February as investors reassess policy impact

Risk appetite among US equity investors has slumped in February amid a re-evaluation of policy impact, according to the latest S&P Global’s Investment Manager Index™ (IMI™) survey. The IMI’s headline Risk Appetite Index has fallen from +15% in January to -27% in February.

The sharp decline signals a return to risk aversion on balance, contrasting with the revival of risk appetite seen in the prior three months following the Presidential election.

February’s reading takes risk appetite further from December’s 44-month high, down close to the level plumbed last September. In fact, since data were first collected in October 2020, only four months have recorded higher risk aversion than that currently being reported.

February has also seen investors’ expectations of US equity returns over the coming month turn sharply negative, falling further from the near-survey high recorded back in November to now sit at one of the most pessimistic levels in over four years of survey history.

The single biggest change to investors’ views on what’s driving the markets is a perceived deterioration in the political environment, which is now reported as the biggest drag on US equities barring only concerns over high valuations – albeit with concerns over the latter now at the highest since the survey began in October 2020.

However, February has also seen a major reassessment of the US macroeconomic environment, which investors now perceive to be only a negligible positive driver of equity returns. In contrast, the prior two months had witnessed investors consider the US economy the most important driver of equities. February is likewise seeing investors report the global macro environment as an increasing drag on US equities.

Concerns are focused on tariffs and the scope for escalatory trade protectionism to weaken economic growth both within the US and globally, with concerns also intensifying in relation to second-round effects, such as higher US inflation and an accompanying hawkishness from the Fed. Whereas late-2024 saw investors view central bank policy as a key driver of equity returns, Fed policy has now been viewed as a drag for two successive months.

Similarly, despite pledged tax cuts, fiscal policy is now perceived as a drag on equities in February, exerting its biggest pull for over a year.

That leaves shareholder returns and equity fundamentals as the only two significantly perceived market drivers in February. Moreover, in both cases, these are viewed as exerting a reduced influence compared with January, especially in the case of fundamentals, which has in turn been reflected in lower earnings expectations. When asked about the key risks to dividend growth, investors remained cautious, citing the uncertainty at play given the increased risks for prolonged tariff implementation.

Yet, equity flows are positive and rising everywhere…

- Investors Buy Stocks as Cash Levels Hit 15-Year Low: BofA Survey – Bloomberg: “Investors are bullish, long stocks and short everything else, with cash levels hitting 3.5%, their lowest level since 2010, Bank of America says. Strategists led by Michael Hartnett write equity investors rotate to bond-sensitive assets and Europe as 82% of respondents see no recession, 77% expect Fed cuts.”

While the nearly 300 participants to S&P Global’s Investment Manager survey with $3.5T AUM are getting cautious on earnings growth, actual earnings are literally booming:

EARNINGS WATCH

383 companies in the S&P 500 Index have reported earnings for Q4 2024. Of these companies, 74.4% reported earnings above analyst expectations and 17.5% reported earnings below analyst expectations. In a typical quarter (since 1994), 67% of companies beat estimates and 20% miss estimates. Over the past four quarters, 78% of companies beat the estimates and 17% missed estimates.

In aggregate, companies are reporting earnings that are 6.3% above estimates, which compares to a long-term (since 1994) average surprise factor of 4.2% and the average surprise factor over the prior four quarters of 6.6%.

Of these companies, 62.8% reported revenue above analyst expectations and 37.2% reported revenue below analyst expectations. In a typical quarter (since 2002), 62% of companies beat estimates and 38% miss estimates. Over the past four quarters, 62% of companies beat the estimates and 38% missed estimates.

In aggregate, companies are reporting revenues that are 1.1% above estimates, which compares to a long-term (since 2002) average surprise factor of 1.3% and the average surprise factor over the prior four quarters of 1.2%.

The estimated earnings growth rate for the S&P 500 for 24Q4 is 15.3%. If the energy sector is excluded, the growth rate improves to 18.7%.

The estimated revenue growth rate for the S&P 500 for 24Q4 is 4.9%. If the energy sector is excluded, the growth rate improves to 5.5%.

The estimated earnings growth rate for the S&P 500 for 25Q1 is 8.5%. If the energy sector is excluded, the growth rate improves to 10%.

Analysts are revising downward, in all sectors but 3 (Comm. Services, Tech and Utes).

Preannouncements are not worsening:

Forward earnings don’t assume lower tax rates which, if enacted, could boost annual earnings by 5% according to Goldman Sachs.

2025 earnings are seen rising 11.3% and 18.3% for Comm. Services and Tech respectively. All other sectors: +9.2%, ex-Energy: +9.8%.

Trailing EPS are now $244.36. Full year 2024: $245.56. Forward EPS: $270.46e (down from $272.92 last month). Full year 2025: $270.95e.

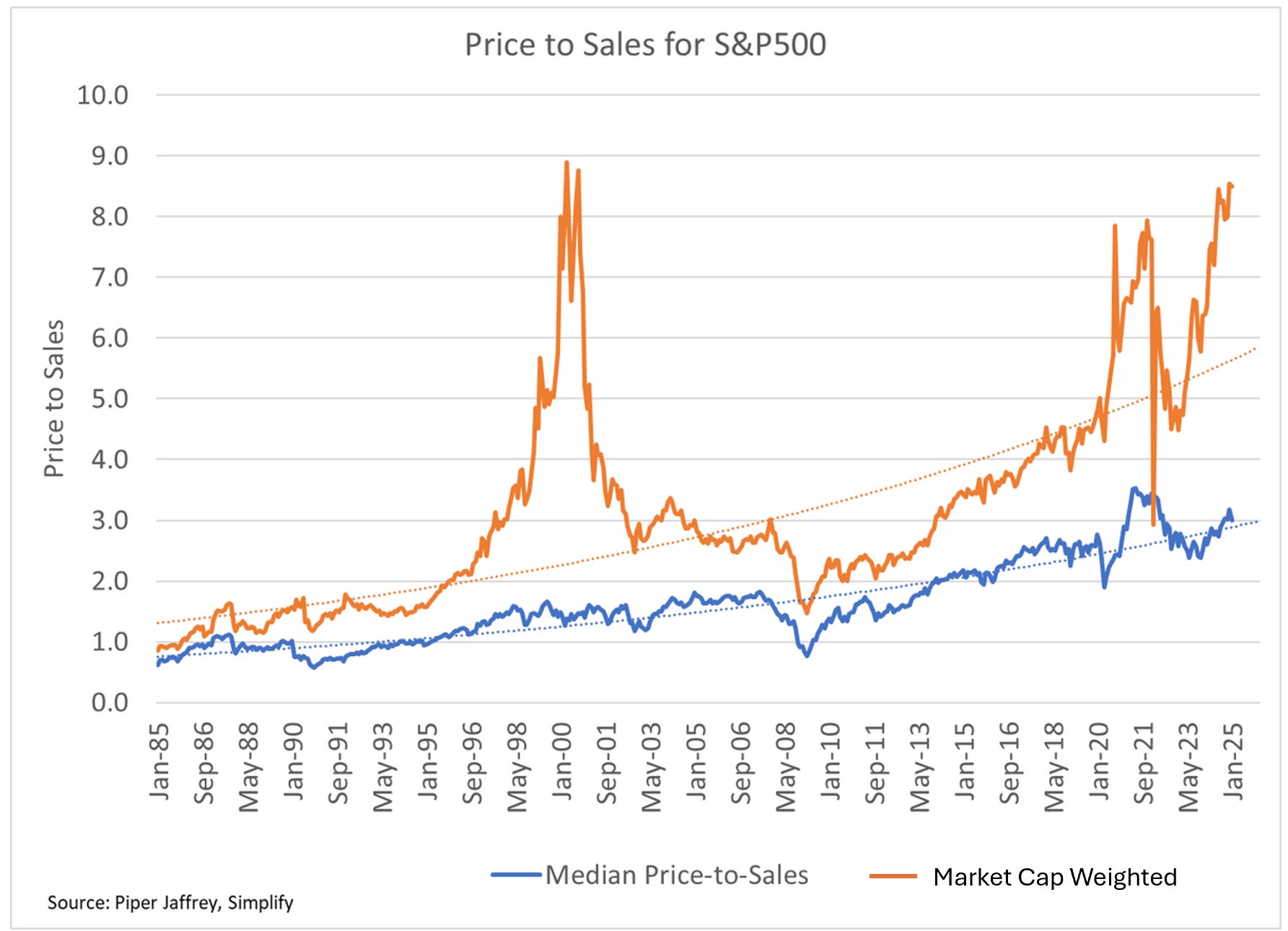

Always grateful to Ed Yardeni, the S&P 500 ex-Megacaps-8 P/E is 19.7. The red line above is at 20.0.

The Equal-weigh P/E is 17x. Sounds more reasonable … until you compare that with history:

Price/Sales charts like this one are very popular these days…

Source: @profplum99 Michael W. Green

… but P/S measures must always come with profit margins since a dollar of sales with 26% margin is worth much more than a dollar of sales with 12% margins, isn’t it?. Ed Yardeni has these 2 charts:

The Megacap-8’s P/S is 7.4x, nearly double pre-pandemic levels. Their profit margins grew from 18% to 26% in that period! Non-Megacap-8 margins have only crawled back to their 2018 level where they seem to be stalling.

The current narrative that equity markets are broadening is not supported by expected revenue growth rates, unless inflation materially slows down, or profit margins suddenly turn upwards.

Non-Megacaps are much more economy sensitive than tech companies, thus carrying many uncertainties (tariffs war, inflation, interest rates).

But the market has largely ignored rising policy uncertainty, so far.

Source: @markets Read full article

Source: @markets Read full article

US companies falling behind on loans at fastest pace in almost a decade Experts warn tariffs and stubbornly high interest rates could worsen debt distress in 2025

(…) US business borrowers were at least one month late on more than $28bn in bank debt at the end of 2024, up $2.2bn in the final three months of the year and $5.4bn from a year earlier, according to newly released bank regulatory data collated by BankRegData. The data does not include loans from direct lenders and private credit funds, which are an increasingly bigger portion of corporate lending. (…)

“Large companies are doing fine, but there are a growing number of small and midsized companies that the economy is not providing enough help.”

As of Q3’23, delinquency rates were not alarmingly high even for smaller companies:

- Junk Bond Guru Sees Rising Distress Ahead as Banks Tighten Lending (Thanks Terry)

The strong US economy has left distressed debt investors starved of opportunity but that may be about to change, according to veteran high-yield analyst Marty Fridson.

The latest Federal Reserve survey of senior loan officers showed banks raising standards by the most in three years when they’re lending to medium-sized and larger companies. That’ll put the squeeze on borrowers already grappling with higher funding costs and global volatility from escalating trade wars.

“At the margin, a tightening of credit standards puts more companies in serious risk of default,” said Fridson, a former strategist at Merrill Lynch whose debt analysis has been studied by Wall Street for decades.

There’s a correlation of about 0.7 between lending standards and the level of distress in credit markets, Fridson’s data going back to 1997 show. (…)

Of course, the latest Fed survey data may just be a blip — lending standards have been in decline since September 2023 and could loosen up again if banks see beyond trade war volatility and get confident that the US is on a sustainable long-term growth path. Other tailwinds include ample global demand for yield from US issuers and private markets, where there’s a lot of dry power available that offers a lifeline to some struggling borrowers.

But the biggest move up in lending standards since the fourth quarter of 2022 adds pressure to the weakest companies with nearby debt maturities. For some, refinancing costs are unsustainably high, just as new trade and immigration policy threaten to put pressure on input costs and therefore earnings, making debt markets less predictable.

At the same time, corporate bond spreads remain close to the pre-financial crisis tights they hit last year. The narrow gap between risk premiums on notes of different credit quality highlight the fact that there is much more demand for high-yielding debt than net new supply. (…)

An Investing Riddle: Stocks Are in Turmoil but Stock Markets Aren’t While the S&P 500 has been unruffled by DeepSeek and the tariff war, stocks in the index have been volatile and uncorrelated

Judging by the S&P 500’s 4% year-to-date gain, it is hard to glean that it has recently been hit by two big shocks: the rise of Chinese artificial intelligence and the Trump administration’s tariff war. Investors don’t seem concerned about uncertainty ahead either: The Cboe Volatility Index, or Vix, dubbed the market’s “fear gauge,” briefly hit 18.6 earlier this month, but has since fallen to 15. The historical average is 19.5.

What is truly weird, though, is that while S&P 500 volatility has been contained, the stocks that are part of it have been bouncing wildly. Drops in some have offset surges in others, and vice versa. Take the “Magnificent Seven” technology-heavy companies: Collectively, they are down 2.7% from the close of Jan. 24, when China’s DeepSeek first spooked investors. But Alphabet is down 7.5% and Meta Platforms is up 13.8%. (…)

It isn’t that investors have sold all AI-related companies and bought everything else. Stocks within the Magnificent Seven have become less correlated to one another than during most of the past decade. (…)

Also, this isn’t just about technology. Wolfe Research created a basket of U.S. stocks that contains companies seen as particularly vulnerable to protectionist policies—including Caterpillar, Hasbro and Dollar General. An analysis of the basket shows low correlations, even as the pace of tariff pronouncements from the Trump administration has accelerated. The same thing is happening across sectors of the S&P 500 and within European equity markets. (…)

Xi’s Embrace of China Tech CEOs Spurs Hope of Big Economic Shift

Xi’s Embrace of China Tech CEOs Spurs Hope of Big Economic Shift

President Xi Jinping’s embrace of Chinese tech bosses in a rare public meeting is fueling hope Beijing is shifting its stance to give the private sector a freer hand as it fights a trade war with Donald Trump.

Four years after launching a regulatory crackdown that plunged the tech sector into turmoil, China’s top leader sat down publicly for the first time with Alibaba co-founder Jack Ma, whose firm bore the brunt of that campaign. Also on the guest list Monday were rising stars from robotics start-up Unitree, electric car giant BYD Co. and AI newcomer DeepSeek — firms rolling out world-beating innovations despite US export controls.

While a similar show of support from Xi in 2018 proved fleeting, developing national tech champions is core to Beijing’s plan for boosting the economy as it deflates a bubble in the property market that once drove about a quarter of growth. Underscoring the importance of spurring innovation, high-tech industries contributed to 15% of gross domestic product last year and are set to overtake the housing sector in 2026, according to Bloomberg Economics.

(…) the return of a high-profile business leader marks the first definitive sign that regulatory reset has concluded,” he added, referring to Ma. (…)

Xi’s meeting should now make it easier to secure equity financing in hardware technology, AI, and the new energy sectors, according to a senior executive from a privately owned chip gear maker, who said the attendee make-up had pointed to an emphasis in those areas.

The focus now is on an annual parliamentary huddle in March, where Xi is expected to set a growth goal of about 5%. It’s unclear how policymakers will get there, as Beijing still hasn’t articulated a plan for arresting sticky deflation, unlocking consumer spending and overcoming growing hostility to its export glut, from friendly partners as well as the US.

In the meantime, Xi is flexing some muscle by bringing together the nation’s big tech guns. (…)

The FT adds that Xi “took pains to emphasise the entrepreneurs’ importance to China’s economic strength, referring to the “two unshakeable principles” — meaning that both the public and private sector should be supported. But he also reiterated the ruling Chinese Communist party’s control over business, stressing that companies should be “ambitious in serving the country”. (…) The Chinese leader urged the business leaders present at Monday’s meeting to “actively fulfil social responsibilities” and “promote common prosperity”. (…)

The Chinese leader promised a level playing field for private businesses this week, and the resolution of persistent challenges such as high financing costs and late payment by state bodies as well as an end to arbitrary fees, fines and inspections. (…)”

- Addressing an audience which included Alibaba’s Jack Ma, as well as leaders of DeepSeek, CATL, BYD, Tencent, Xiaomi, Huawei and Unitree Robotics, Xi is reported to have said, “It is time for private enterprises and private entrepreneurs to show their talents” and that his government “must resolutely remove various obstacles” faced by private firms.

- Xi said that he would promote the healthy development of the private economy.

- “The private sector in China, which competes with state-owned companies, contributes more than half of tax revenue, more than 60 per cent of economic output and 70 per cent of tech innovation, official estimates show.” (Reuters)