LAST TWO WEEKS RECAP

Back from truly beautiful and interesting Peru, here‘s what I honestly did not miss but was nonetheless important, especially since we can now get a better picture with the shutdown and poor weather largely behind us. From 4,300 meters (14,000 ft) in Peru, the world looked really beautiful. Back at seal level, the details are not so charming…

OECD LEIs Flash Slowdown!

(…) These indicators show declining LEI values on a broad array of countries and regions with a time series of weakness in train as well for each. The top panel in the table below shows growth rates in the LEIs on conventional three-month, six-month, and 12-month horizons. The bottom panel shows sequential six-month growth rates as the OECD likes to look at the LEI signal over six-month periods.

The top panel shows a lot of weakness and declining indexes with annualized growth rates revealing weaker as well as weak growth in their most recent periods for the OECD-7 and for Japan. The U.S. the euro area and the whole OECD are just short of exhibiting the same continually decelerating pace.

The bottom panel shows changes over six months on average and then shows sequential six-month periods that reveal a great deal of weakness with declining LEIs everywhere and with the pace generally getting sequentially weaker as well. This is a picture of a broad slowing in the global economy. China echoes this weak (and weakening) growth performance.

(…) we have two weakening criteria in this [next] table: low-valued LEI readings and progressive deterioration. The third one is the low queue percentile standings in the far right hand column, where 50% indicates the median and all are weaker than that. In fact, the strongest does not reach its 25th percentile standing.

The chart shows how LEI growth rates plot against the historic U.S recession bands. The chart also shows that there is little difference between the OECD signals and the U.S. economic signals. As goes the U.S., so goes the OECD. That isn’t very surprising.

(…) The global slowdown is real. It is an industrialized country phenomenon and it is a developing economy phenomenon. China and the EMU are especially weak. But the U.S. is doing poorly as well despite its better GDP performance. Its current LEI index is low and its growth rate is gaining downward momentum rapidly.

The final chart looks the U.S. and China vs. the U.S. recession bars. Before 2000, the U.S. and China seemed to go their own way a lot. But since 2000, China and the U.S. have been more or less rising on the same cycles with China’s amplitudes generally exaggerated when compared to the U.S. China does not seem to have changed the game that much. Of course, there is nothing here that speaks to how one country’s cycle might have or might be affecting the cycle in another country. But if we view these as largely independent movements what we see is that they have become almost as well synchronized as the U.S. to OECD cyclical developments. And the conclusion from that, of course, is that these are not independent movements but rather codependent movements. (…)

Conference Board Leading Economic Index: “Economic Growth Likely to Moderate

The latest Conference Board Leading Economic Index (LEI) for March increased to 111.9 from 111.5 in February. The Coincident Economic Index (CEI) came in at 105.8, up from 105.7 the previous month.

The Conference Board LEI for the U.S. increased again in March. Positive contributions from initial claims for unemployment insurance (inverted), consumer expectations for business conditions, and financial components fueled the most recent gain. In the six-month period ending March 2019, the leading economic index increased 0.4 percent (about a 0.7 percent annual rate), much slower than the growth of 2.8 percent (about a 5.6 percent annual rate) during the previous six months. In addition, the weaknesses and strengths among the leading indicators have become equally balanced over the last six months.

The Conference Board CEI for the U.S., a measure of current economic activity, edged up in March. The coincident economic index rose 1.0 percent (about a 1.9 percent annual rate) between September 2018 and March 2019, slightly slower than the growth of 1.2 percent (about a 2.3 percent annual rate) for the previous six months. But, the strengths among the coincident indicators have remained very widespread, with all components advancing. The lagging economic index increased also by 0.1 percent last month. As a result, the coincident-to-lagging ratio remained unchanged. [Full notes in PDF]

But the LEI has been flattening since September

- LEI and Its Six-Twelve-Month Smoothed Rate of Change

U.S. Industrial Production Slips

There is really nothing strong in this table, is there? Everything is down big time sequentially.

U.S. Retail Sales Rebound Is Broad-Based

Total retail sales increased 1.6% during March following a 0.2% February dip. It was the largest monthly increase since September 2017. The 3.6% y/y sales pace, however, remained down from growth during 2018 and 2017.

There are possibly 3 ways to look at the recent retail sales data:

- the optimistic view only sees Q1 numbers with total retail sales up 9.1% annualized (+10.0% ex-autos):

- the less optimistic view includes November and December of 2018, the two most important months of the year. Last 5 months annualized: retail sales –0.4% (-0.1% ex-autos). As the chart shows, retail sales are not higher now than in July 2018. The last similar stalling in sales was in 2014-15 but that was primarily due to the sharp drop in oil prices in the second half of 2014. There was also a sharp drop in oil prices from $75 in October to $45 in December 2018. Does this explain that?

-

December’s collapse will eventually be proven wrong.

U.S. Business Inventories and Sales Growth Slows in February

Whatever the reasons, weak retail sales impact the whole goods economy, creating an inventory overhang which needs to be worked out, like in 2015-16:

Hence:

IHS Markit Flash U.S. PMI™:

The seasonally adjusted IHS Markit Flash U.S. Manufacturing Purchasing Managers’ Index™ (PMI™) registered 52.4 in April, unchanged from March’s reading. The latest data nonetheless signalled the joint-weakest improvement in operating conditions across the sector since June 2017. (…)

The latest increase in new business was the quickest for three months. Nevertheless, the expansion was well below those seen this time last year, with foreign demand also remaining relatively muted. As a result, production volumes expanded at a slightly quicker, albeit still modest, pace. (…)

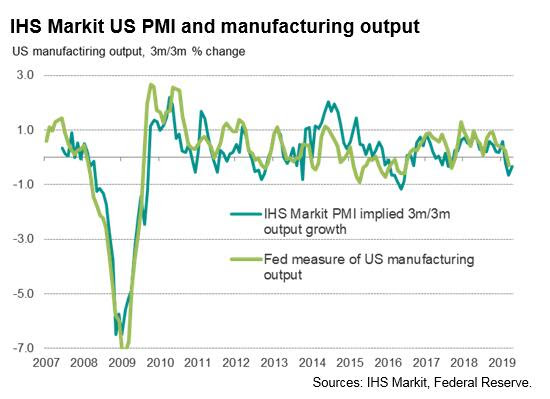

The manufacturing sector remained the weakest part of the economy. Although the survey’s output index ticked higher, it is still running at an historically subdued level consistent with the official manufacturing production data remaining in contraction at the start of the second quarter. The factory malaise in April therefore extends a downturn in the first quarter that had been correctly indicated by the survey.

A major contrast in April to the first quarter was a marked slowing of growth in the service sector, highlighting how the slowdown has now spread beyond the factory sector. The flash services PMI business activity index fell to 52.9 in April, down from 55.3 in March and its lowest since March 2017.

")

The slower overall increase in output was driven by widespread reports of softer demand conditions, with new orders growth easing for the second month running in April to the weakest for two years.

Having indicated an annualised GDP growth rate of approximately 2.5% in the first quarter, similar to that signalled for the fourth quarter of last year, the April survey implies that the rate of economic growth has slowed to 1.9% at the start of the second quarter.

")

-

Hiring slows amid growing gloom

The reduced inflow of new work meant firms reported less strain on capacity, putting a foot on the break for staff hiring. Employment across the combined manufacturing and service sectors rose at the slowest rate for two years. The survey’s headline employment index is indicative of non-farm payrolls growing by 130,000 in April, well below the 198,000 average indicated in the first quarter.

Expectations towards output growth over the coming year were also toned down in April. Companies’ expectations of future growth slid to one of the lowest seen since comparable data were first collected in 2012. Only mid-2016 has seen gloomier business prospects.

While the overall rate of growth and job creation being signalled remain relatively solid, the drop in optimism and weakness of order books means the slowdown likely has further to run.

World economies were pretty weak in 2018 in spite of the fairly resilient U.S. economy. If the latter is now working out its excess inventories…

The pace of eurozone economic growth slowed for a second successive month in April, according to flash PMI survey data, indicating that the economy remains in its worst growth spell since 2014. Manufacturing reported a further contraction and service sector growth cooled.

A solid service sector performance in Germany helped sustain the expansion, offsetting a sharp manufacturing downturn. France meanwhile stagnated and the rest of the region saw the worst growth since late-2013.

The IHS Markit Eurozone Composite PMI® fell from 51.6 in March to 51.3 in April, according to the preliminary ‘flash’ estimate. The latest reading was the third-lowest since November 2014, only marginally above the recent lows seen in December and January.

New order growth picked up only marginally, remaining close to stagnant. New export orders fell sharply, down for a seventh straight month to continue the worst period of export performance since comparable data covering both goods and services were first available in 2014.

Backlogs of work dropped for the fourth time in the past five months and have not shown any growth since last November. The reduction in backlogs was only fractionally smaller than in March, which had seen the steepest decline since December 2014. (…)

Business expectations about the year ahead continued to run at one of the gloomiest levels since late-2014, dipping for a second successive month to the lowest since January. Reduced optimism was often linked to the recent slowing in demand and lower sales enquiries, as well as downgraded forecasts for economic growth. Specific concerns focused on rising political uncertainty, including Brexit, trade wars and protectionism. The weakness of the auto sector was also again often cited as an area of concern.

Although input cost inflation across the euro area accelerated for the first time in seven months from March’s two-and-a-half year low, in part driven by higher oil prices, average prices charged for goods and services rose as at the slowest rate for 20 months as weak demand stifled pricing power. (…)

The data add to worries that the economy has failed to rebound with any conviction from one-off factors that dampened activity late last year, and continues to show only very modest growth in the face of headwinds from slower global demand growth and subdued economic sentiment.

The surveys indicate that quarterly eurozone GDP growth has slowed to just under 0.2%. A similar 0.2% rate of expansion is being signalled for Germany but France stagnated and the rest of the region has moved closer to stalling.

Manufacturing remained the key area of concern, with output continuing to contract at one of the fastest rates seen over the past six years. Forward -looking indicators showed some signs of improvement but remain deeply in negative territory to suggest the factory malaise has further to run.

The slowdown also showed further signs of engulfing the service sector, where growth cooled again to one of the weakest rates seen since 2016. Some encouragement can be gleaned from an improvement in employment growth, although even here the pace of hiring is among the lowest seen for two-and-a-half years.

The persistence of the business survey weakness raises questions over the economy’s ability to grow by more than 1% in 2019.

")

Japan: Stronger employment growth lifts PMI, but export demand continues to falter

- Flash Japan Manufacturing PMI® at 49.5, third straight month below the 50.0 no-change mark

- Weaker demand from domestic and international markets persists, leading output to fall further

Japan’s manufacturing sector remained stuck in its rut at the start of Q2, with the factors which have prohibited any growth such as US-Sino relations, growth fears in China and the turn in the global trade cycle, all remaining prominent risks. Export orders dipped at a stronger rate in April, domestic demand for goods was similarly weak and firms cut their stocks and scaled back production. Yet again, the service sector will need to pick up any slack to help keep Japan’s economy afloat.

Meanwhile, in China:

-

China’s Economic Data Shows Signs of Bouncing Back

-

China Growth Bode Well for Global Economy

-

Some Better-Than-Expected China Data Can’t Save the World Economy

-

China Officials Said to Be Preparing New Stimulus

U.S. to End Waivers on Iranian Oil Exports The State Department is expected to announce Monday the end of waivers for countries to import Iranian oil, part of the Trump administration’s effort to drive Iran’s exports to zero, people familiar with the decision said.

The U.S. had previously granted eight countries a 180-day waiver to continue to buy Iranian crude despite U.S. sanctions, provided that each took steps to reduce purchases and move toward ending imports. The deadline for renewing the waivers was set to fall on May 2.

China, India and Turkey were among Iran’s top customers and had been expecting to receive a renewed waiver to continue to buy Iran’s oil.

It wasn’t immediately clear whether the decision to end oil waivers would put a complete halt to permitted exports.

A “wind down” grace period would allow certain customers to continue to receive the oil it had already purchased, or agreed to buy, two people familiar with the matter said. It wasn’t immediately clear how such a mechanism would work.

“China consistently opposes U.S. unilateral sanctions and long-arm jurisdiction,” said Geng Shuang, a spokesman for China’s Foreign Ministry, at a regular news briefing on Monday. “China-Iran cooperation is open, transparent and in accordance with law, it should be respected.” (…)

U.S. sanctions targeting oil exports from Iran and Venezuela have tightened global supply and driven prices higher this year. Markets are closely watching the latest outbreak of chaos in Libya, which has been pumping more than 1.2 million barrels of oil a day. (…)

DESINFLATION…DEFLATION FEARS?

The other important stat was on inflation, rather disinflation.Core CPI was +0.147 in March, following +0.111% in February or +1.5% annualized combined. This after +2.5% annualized between October 2018 and January 2019, coinciding with slow consumer demand and rising inventories. Core Goods inflation was –0.2% in each of February and March, offsetting January’s +0.4%. Repeat of 2014?

Markit’s flash PMIs had some interesting findings on prices from the corporate viewpoint:

Cost pressures meanwhile remained subdued, with the rate of input price inflation across the private sector easing to the lowest since September 2016.

The drop in the surveys input price gauge suggests that inflationary pressures continued to moderate. The composite input price index covering both goods and services has a strong correlation with future CPI and PCE inflation rates, and signals that both annual consumer price and PCE inflation could drop below 1% in coming months as pricing power fades alongside weaker demand.

Related:

Related:

Fed Officials Contemplate Thresholds for Rate Cuts A cut isn’t imminent, but interviews, public remarks suggest Fed officials are talking about the conditions that might lead to such an action

(…) f inflation runs too far below 2% for a while, it would show “our setting of monetary policy is actually restrictive, and we need to make an adjustment down in the funds rate,” Chicago Fed President Charles Evans said Monday, referring to the central bank’s benchmark federal-funds rate. (…)

But if it turns out that core inflation, which excludes volatile food and energy categories, falls and stays near 1.5% for several months, “I would be extremely nervous about that, and I would definitely be thinking about taking out insurance in that regard” by cutting rates, he said.

Dallas Fed President Robert Kaplan didn’t endorse such a move outright but said Thursday that inflation running persistently around 1.5% or lower is “something I’m going to certainly take into account” when setting rates. (…)

Fed Vice Chairman Richard Clarida, speaking earlier this month on CNBC, appeared to be lowering the bar for such a move. He volunteered that a recession wasn’t the only situation in which the Fed had cut rates in the past, pointing to instances in the 1990s in which the central bank “took out some insurance cuts.” (…)

From the Fed’s recent Beige Book on prices and inflation:

- Prices were generally stable or rose modestly. (Boston)

- Businesses reported that both input price increases and selling price increases slowed considerably in the latest reporting period. (NY)

- Price increases remained modest for most firms. (Philly)

- Selling prices rose moderately in the District at a pace similar to that of the prior period. (Cleveland)

- On balance, price growth remained moderate since our previous Beige Book report. (Richmond)

- Firms across the District noted little change in pricing pressure since the last report. (Atlanta)

- Prices rose modestly in late February and March, and contacts expected prices to continue to rise at that rate over the next 6 to 12 months. Retail prices increased modestly. (Chicago)

- Prices have increased modestly since the previous report. (St. Louis)

- Price pressures increased modestly. A Minneapolis Fed business survey indicated that a slight majority of firms increased output prices in the first quarter of 2019 relative to the same period a year earlier; a similar proportion planned price increases in the second quarter. (Minneapolis)

- Respondents in the retail sector reported strong growth in input prices and moderately higher selling prices since the previous survey period. (KC)

- Selling price growth was modest to moderate, and passing on cost increases to customers remained difficult. (Dallas)

- Price inflation was unchanged on balance over the reporting period. (SF)

Your call as to what “modest” and “moderate” actually mean in numbers but given the Fed’s seemingly impossible dream of 2% inflation, it must be no more than 1.0-1.5%. I noticed more mentions of selling prices not rising in sync with input prices rising due to tariffs and metal surtax.

Yet, the earnings season is off to a good start:

EARNINGS WATCH

Through Apr. 18, 77 companies in the S&P 500 Index have reported earnings for Q1 2019. Of these companies, 77.9% reported earnings above analyst expectations and 16.9% reported earnings below analyst expectations. In a typical quarter (since 1994), 65% of companies beat estimates and 21% miss estimates. Over the past four quarters, 76% of companies beat the estimates and 17% missed estimates.

In aggregate, companies are reporting earnings that are 5.2% above estimates, which is above the 3.2% long-term (since 1994) average surprise factor, and below the 5.4% surprise factor recorded over the past four quarters.

(…) Of these companies, 48.1% reported revenues above analyst expectations and 51.9% reported revenues below analyst expectations. In a typical quarter (since 2002), 60% of companies beat estimates and 40% miss estimates. Over the past four quarters, 67% of companies beat the estimates and 33% missed estimates.

In aggregate, companies are reporting revenues that are 0.3% above estimates, which is below the 1.5% long-term (since 2002) average surprise factor, and below the 1.1% surprise factor recorded over the past four quarters.

The estimated earnings growth rate for the S&P 500 for 19Q1 is -1.7% [from –2.0% on April 1]. If the energy sector is excluded, the growth rate improves to -0.3%. (…)

The estimated earnings growth rate for the S&P 500 for 19Q2 is 2.1% [2.8%]. If the energy sector is excluded, the growth rate improves to 2.3%. (Refinitiv)

So far, 26 of the 67 Financial companies in the S&P 500 have reported with a beat rate of 64.5% and a surprise factor of +5.5%, prompting analysts to boost their expected earnings growth for Q1 from +2.7% to +6.4%. Investors probably were also relieved to see that the 16 (of 96) consumer centric companies having reported beat by 6.7% on average.

Trailing EPS rose to $163.39 last week. Coupled with the decline in inflation also recorded last week, the Rule of 20 P/E declined to 19.8. For the record, the Rule of 20 Strategy did not trigger a change in its current 100% equity exposure as the S&P 500 Index touched 2914, one point below the trigger level of 2915 per last weeks’ data. The current trigger has risen to 2941.

Analysts have been a little less downbeat last week, particularly on large caps:

TECHNICALS WATCH

Technical signals on U.S. large caps are mostly positive (see below). Smaller caps have been another story:

Lowry’s Research keeps the small caps hope alive, noting that since the Dec. 2018 market bottom, small caps have displayed steady improvement by several measures of internal strength.

- The S&P Small Cap Adv-Dec Line is at a new all-time high, although it has yet to move significantly above its late Feb. 2019 recovery high and remains far below its Aug. 2018 all-time high.

- The percentage of OCO Small Caps at or within 2% of their 52-week highs is trending higher.

- The percentage of Small Caps at or close to their highs has been increasing.

- Also, it’s worth noting that the percentage of Small Caps Down 20% or more from their 52-week highs has been gradually trending lower. “This is in contrast to the deterioration in small caps occurring late in a bull market and reflected by a sustained rising trend in this percentage.”

From CMG Wealth’s Steve Blumenthal:

- 13/34–Week EMA Trend Chart: Buy Signal

- S&P 500 Index 200-day Moving Average Trend: Buy Signal

-

S&P 500 Index 50-day vs. 200-day Moving Average Cross: Buy Signal

- NDR Crowd Sentiment Poll: Extreme Optimism (S/T Bearish for Equities)

Source: Ned Davis Research

Source: Ned Davis Research