ECONOMY WATCH

- Initial weekly unemployment claims fell 12,000 in the week ended September 14 to 219,000, much better than the 230k economists were expecting and unchanged from one year ago. Continuing claims also fell by 21,000 to 1.829 million in the week prior, up 2.1% YoY but down 1.0% from its mid-August peak. Prior to previous recessions, these indicators were deteriorating much more significantly.

- The Philly Fed’s Manufacturing PMI moved back into positive territory in September. That followed a spike in the New York Fed’s M-PMI. Ed Yardeni says that “Assuming the other three regional Fed surveys follow suit, this bodes well for September’s national ISM M-PMI. It suggests rate cuts will be an additive force to an already recovering goods-producing sector. Also of note, the Philly Fed’s employment index jumped from -5.7 to 10.7 this month. Meanwhile, the prices paid indexes in both the New York and Philly surveys are climbing again.” However, the new orders index fell 16 points to -1.5.

- The Conference Board Coincident Economic Index increased by 0.3% MoM in August to a new record high. “The CEI’s component indicators—payroll employment, personal income less transfer payments, manufacturing and trade sales, and industrial production—are included among the data used to determine recessions in the US. All components improved in August, with industrial production recovering the most after July’s decline. The CEI is highly correlated with S&P 500 forward earnings, which rose to a record high in August too.” (Ed Yardeni)

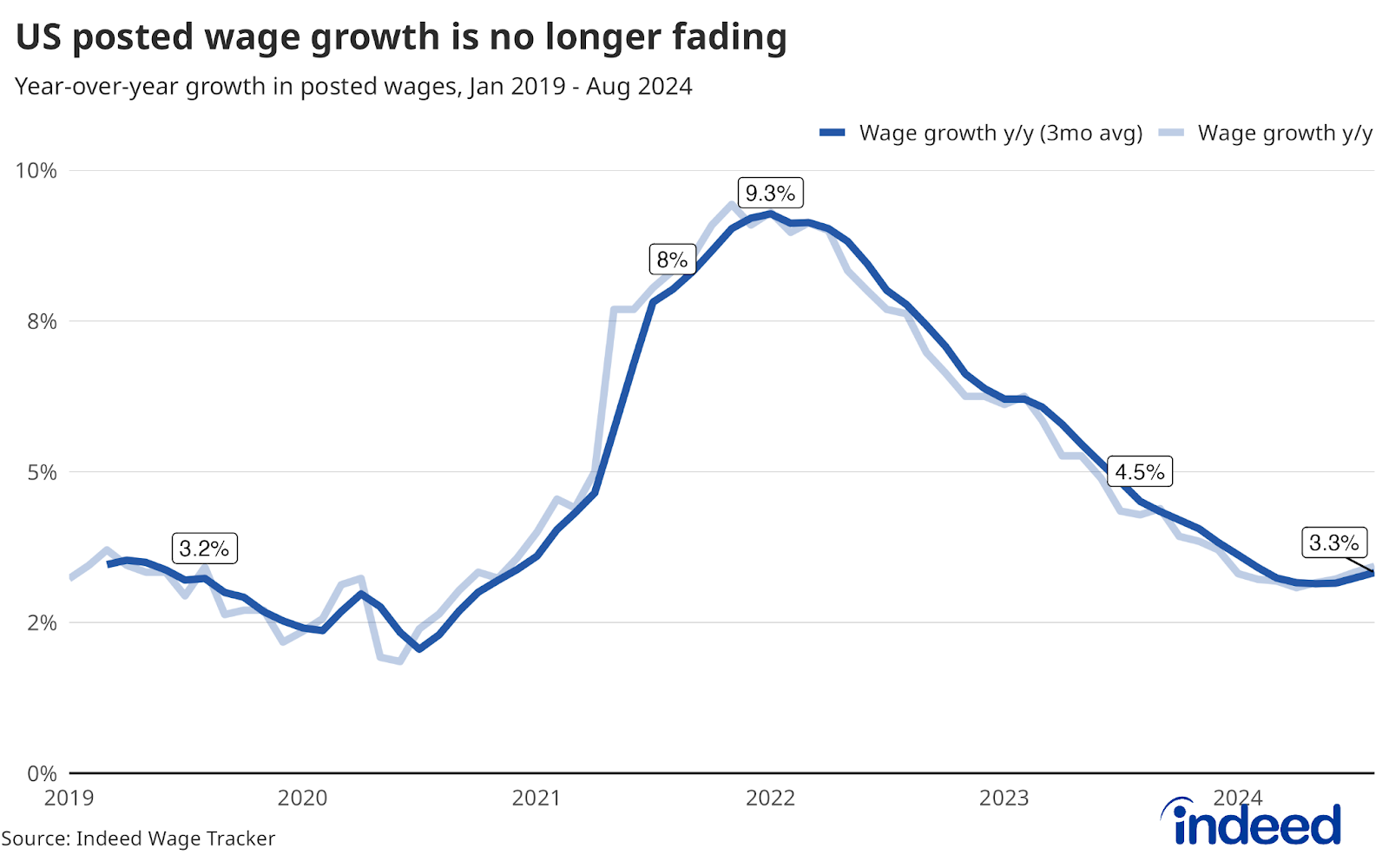

- Posted wage growth rose to 3.3% in August, according to the latest data from the Indeed Hiring Lab. This jibes with the stabilization in the Atlanta Fed Wage Growth Tracker between 4.5-5.0%. Let’s hope productivity growth remains strong.

Europe’s EV Sales Plunge Has Carmakers Seeking EU Relief

EV deliveries in the region’s biggest car market fell 69% during August, fueling a 36% drop across the region, the European Automobile Manufacturers’ Association said Thursday. The group urged the European Commission to take urgent relief measures ahead of 2025 fleet-emissions targets that could result in billions of euros in fines for carmakers that fail to meet them.

Europe’s auto industry has struggled with a drop in demand for EVs after governments pulled back financial incentives that had made the relatively expensive cars more affordable. With the battery-car market share shrinking to 14% in August — down from just over 15% last year — auto manufacturers are rethinking their strategies and timelines for shifting away from combustion engines.

The decline has been most pronounced in Germany, which is facing a spate of setbacks in its industrial core. Volkswagen AG, the continent’s biggest automaker, has scrapped a decades-old labor pact and is poised to close domestic factories in Germany for the first time due to lagging demand. BMW AG cut its full-year earnings guidance, partly citing sluggish EV sales. Elsewhere, chipmaker Intel Corp. has pushed back building a planned factory for which the country’s government had earmarked €10 billion ($11.1 billion) in subsidies.

The German economy may already be in recession, the Bundesbank said Thursday in a report. After shrinking slightly in the second quarter, output could stagnate or decline again in the third, according to the central bank. (…)

Across Europe, new-car registrations dropped 16.5% compared to a year ago to 755,717 million units last month with declines also in France and Italy. The UK was the only major market where EV sales rose, gaining 10.8%. (…)

McKinsey recently polled 15,034 individuals in France, Germany, Italy, and Norway:

- Of the car buyers in our survey who have not yet purchased an EV, 38 percent say their next vehicle will be electric. A little less than half of these potential buyers plan to buy a BEV, with the rest opting for plug-in hybrid electric vehicles (PHEVs).

- While almost 80 percent of European car buyers in our survey expect to get an EV in the future, 22 percent remain skeptical about these vehicles. Our survey suggests that the main reasons preventing skeptics from considering EVs involve high purchase prices, the inability to charge at home, and concern about real battery driving range—the actual driving range for a mix of trips and conditions, compared with a vehicle’s advertised cycle range based on the worldwide light-vehicle test procedure (WLTP).

- Among prospective buyers who do not yet own a BEV, the main concerns about EVs are slightly different from those that the EV skeptics have, especially home charging access being less of a concern. High purchase prices topped the list (37 percent), followed by insufficient battery driving range (36 percent), and battery lifetime (35 percent). Many respondents are also concerned about increases in electricity prices and availability of public charging infrastructure (28 percent for both). Overall, sustainability had a minor influence on purchase decisions.

- In our survey, consumers who would consider an EV but have not yet purchased one state that the driving range would need to be about 500 kilometers for them to switch from an internal combustion engine (ICE) vehicle to a fully electric BEV.

- In our survey, only 42 percent of existing BEV owners in Europe are satisfied or very satisfied with their car’s real driving range; for those who would consider switching back to ICE vehicles, this percentage fell to 30 percent. What’s more, most of the dissatisfied respondents indicate that they are likely to switch to an ICE vehicle, rather than search for an EV with a greater driving range.

- While the overall outlook for electrification is positive, our survey reveals that 19 percent of current EV owners in Europe say they are likely or very likely to switch back to a traditional combustion engine at their next purchase because of their current EV ownership experience. This is a reality check, but it must be considered in context. Globally, 29 percent of EV owners in our survey say they are very likely to switch back to an ICE vehicle at their next purchase, so Europeans are less likely to revert to traditional cars than people in other regions.

- Of the EV owners who are considering a switch back to ICE vehicles, 41 percent say that the cost of EV ownership is too high. (Their return to ICE vehicles could occur shortly, since they are closer to buying their next vehicle than other respondents, and 40 percent are planning to purchase a vehicle in 2024.) If they do, they may find that the residual value of their current EV is lower than expected and that demand for used EVs is relatively low compared with that for traditional cars.

- In our survey, 40 percent of current BEV owners in Europe state that the number of public EV charge points is insufficient. Only about 10 percent of BEV owners feel that the current charging infrastructure is ready to meet future demand; an additional 50 percent feel that it can meet current needs but believe that there will not be enough public charging stations if more EVs hit the road.

- Prospective buyers are increasingly considering non-European brands, and our survey shows that EV owners are broadening their considered set of brands for purchase. European brands such as BMW, Mercedes-Benz, Renault, and Volkswagen are still the most popular, with 51 percent of EV owners stating that they are likely to purchase from them. Southeastern Asian brands such as Hyundai, KIA, and Toyota were in second place with 39 percent, followed by American brands such as Cadillac, Rivian, and Tesla (30 percent) and Chinese brands such as BYD, Li Auto, NIO, and Xpeng (27 percent).

- Customers’ willingness to buy an emerging brand differs by country and segment. In the premium-brand segment, for instance, 33 percent of European respondents considering EVs state that they would be open to purchasing a Chinese brand in the future. Given the European Union’s recent decision to impose tariffs on imported EVs from China, it is still uncertain how successful such new EV brands will be in Europe.

- Compared with American brands and other Asian brands, Chinese OEMs have relatively low name recognition in Europe. In our survey, 55 to 80 percent of European respondents had never heard of them.

- Survey respondents tend to be skeptical about product quality and data security for new market entrant brands from China, although they do perceive them as offering good value for the money. The customers we interviewed at car clinics had similar concerns about Chinese brands, but after seeing the vehicles in person, they were also impressed by their innovative features and cutting-edge technologies, such as comfortable interiors, voice assistants’ conversational intelligence, and high-end multimedia offerings with advanced sound and displays.

- In our survey, about half of European respondents say that they would only consider purchasing a Chinese EV if its price was at least 15 percent below that of a similar domestic model. Roughly a quarter of European respondents say they would seek a price advantage of up to 10 percent, and only 25 percent would not require a price advantage.