December U.S. JOLTS: Job Market Remains Tight

The Bureau of Labor Statistics reported that on the last business day of December, the total number of job openings rose 1.4% m/m from November to 10.925 million, a little above expectations. This was the third highest total openings on record, exceeded only by July and October 2021, and clearly well above pre-pandemic norms. The job openings rate, calculated as job openings as a percent of the sum of total employment and openings, was unchanged at 6.8%, the second highest on record.

New hires fell 5.0% m/m in December to 6.263 million, the lowest level since May 2021, with the hiring rate slipping to 4.2% from 4.4% in November.

The number quitting their job fell 3.6% m/m to 4.338 million in December from the record 4.499 million recorded in November. The quit rate, quits as a percent of total employment, edged down to 2.9% in December from a record 3.0% in November. Layoffs and discharges fell 10.7% m/m in December to 1.169 million, the lowest level on record. The JOLTS figures date back to December 2000.

Private-sector job openings rate rose 1.3% m/m in December to 9.882 million with the private-sector job openings rate edging up to 7.2% from 7.1%. Job openings increased in several industries with the largest increases in accommodation and food services (+133,000 or 9.5%), information (+40,000 or 22.6%), and nondurable goods manufacturing (+31,000 or 9.0%). Job openings decreased in finance and insurance (-89,000 or -21.9%) and in wholesale trade (-48,000 or -14.9%) and were little changed in manufacturing.

Private-sector hiring fell 5.4% m/m in December, its largest monthly decline since December 2020, to 5.87 million. Hiring fell in each major sector in December.

(…) Private-sector quits declined 3.6% m/m in December to 4.129 million. This was the second decline in the past three months. Still, quits remain quite elevated relative to before the pandemic, indicating ongoing labor-market tightness.

This tightness was further supported by an 11.9% m/m decline in private-sector layoffs and discharges to 1.097 million, the lowest on record. Sectoral declines were in construction; trade, transportation and utilities; professional and business services; and leisure and hospitality. Increases were recorded in manufacturing, information, financial activities and education and health services. In total, all private-sector separations fell 5.3% m/m to 5.548 million in December.

Job opening to unemployed ratio surges as demand outstrips supply

Source: Macrobond, ING

As a preview for January:

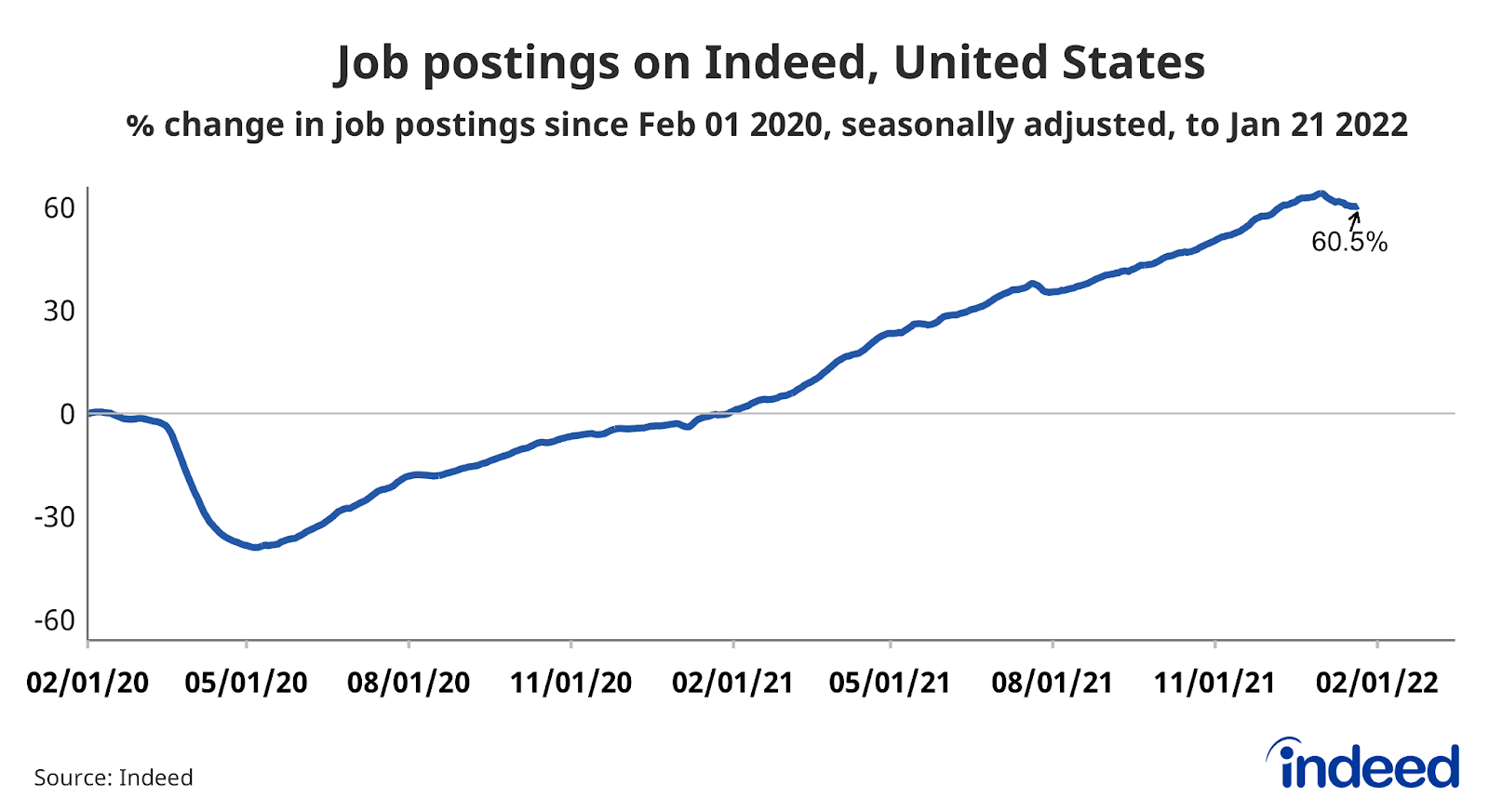

Indeed US Job Postings Tracker: Data Through January 21

Indeed Job Search Survey January 2022: A Tepid Rise in Job Search as New Year Begins

- The share of the population ages 18 to 64 actively looking for paid work rose by two percentage points from the previous month, according to the January 2022 edition of the Indeed Job Search Survey.

- All of the rise in January was driven by an increase in ‘non-urgent’ job search among the employed, potentially reflecting some start of the year exploratory job search. At the same time, urgent job search among the jobless continues to trend upward.

- The average job seeker is still more likely to want to start immediately than they were in June, as job seekers are likely enticed by the higher wages on offer.

- The reasons for a lack of urgency among the unemployed remained varied, with the top reasons in January being employed partners, financial cushions, COVID fears, and care responsibilities.

(…) Not only was the rise in job search entirely fueled by non-urgent search, the increase was entirely concentrated among the employed. (…) Perhaps job seekers who don’t desperately need a job as they already have one are putting out some feelers for a new job as 2022 begins.

The Fed Is Playing with Fire The Fed is so far behind that it can’t even see the curve and may have to slam on the policy brakes to regain control before it is too late. (Stephen Roach)

(…) Like the Fed I worked at in the early 1970s under Arthur Burns, today’s policymakers once again misdiagnosed the initial outbreak. The current upsurge in inflation is not transitory or to be dismissed as an outgrowth of idiosyncratic COVID-19-related developments. It is widespread, persistent, and reinforced by wage pressures stemming from an unprecedentedly sharp tightening of the US labor market. (…)

The forward-looking Fed still faces a critical tactical question: What federal funds rate should it target to address the most likely inflation rate 12-18 months from now?

No one has a clue, including the Fed and the financial markets. But one thing is certain: With a -7% real federal funds rate putting the Fed in a deep hole, even a swift deceleration in inflation does not rule out an aggressive monetary tightening to re-position the real funds rate such that it is well-aligned with the Fed’s price-stability mandate. (…)

I would argue that a responsible policymaker would want to err on the side of caution and not bet on a quick, miraculous roundtrip of inflation back to its sub-2% pre-COVID-19 trend. (…)

In the current easing cycle, the Fed first pushed the real federal funds rate below zero in November 2019. That means a likely -2% to -3% rate in December 2022 would mark a 38-month period of extraordinary monetary accommodation, during which the real federal funds rate averaged -3.1%.

Historical perspective is important here. There have been three earlier periods of extraordinary monetary accommodation worth noting: In the aftermath of the dot-com bubble a generation ago, the Fed under Alan Greenspan ran a negative real funds rate averaging -1.1% for 31 consecutive months. Following the 2008 global financial crisis, Ben Bernanke and Janet Yellen teamed up to sustain a -1.9% average real funds rate for a whopping 62 months. And then, as post-crisis sluggishness persisted, Yellen partnered with Jerome Powell for 37 straight months to hold the real funds rate at -0.9%. (…)

The -3.1% real federal funds rate of the current über-accommodation is more than double the -1.4% average of those three earlier periods. And yet today’s inflation problem is far more serious, with CPI increases likely to average 5% from March 2021 through December 2022, compared with the 2.1% average that prevailed under the earlier regimes of negative real funds rates.

All this underscores what could well be the riskiest policy bet the Fed has ever made. (…)

Now, read what the largest hedge fund in the world thinks:

2022 Global Outlook: The Success and Excesses Resulting from MP3 Policies

(…) As a result of these policies and their effects, policy makers—and particularly the Fed—will increasingly be confronted with a set of choices that will be as challenging as any since the 1970s. Because economies are now experiencing self-reinforcing growth, the natural workings of the economic machine will continue to sustain a high level of nominal growth that is likely to produce a level of inflation that is well in excess of policy targets.

For central banks, asymmetric policy alternatives leave an unlimited ability to tighten and a limited ability to ease on their own, which encourages delay and falling further behind, which is likely to make it increasingly difficult to balance economic growth and inflation. Given the inertia in the system, it is unlikely that the current level of nominal spending growth and its impacts on inflation can be contained without aggressive monetary tightening in the very near term.

In contrast to this unfolding story, the markets are discounting a smooth reversion to the prior decades’ low level of inflation, without the need for aggressive policy action—that it will mostly just naturally happen on its own. We see a coming clash between what is about to transpire and what is now being discounted. The inevitability of this clash is due to the mechanical influence of MP3 policies on nominal incomes, spending, asset prices, and inflation, as we describe below. (…)

Well worth your time to read Dalio’s entire piece.

David Rosenberg:

And with the fiscal policy vacuum and the tightening we are set to see in Fed policy, the nail is in the coffin for this expansion. Even in the best of times, when the Fed has tapped its foot on the brakes we’ve slipped into a recession 75% of the time in the past. The thing is, this time, the Fed is embarking on this inflation-crushing quest 80% of the way into the cycle (not 30%, which is typical) and with a yield curve that is two-thirds as flat as what is normal ahead of a tightening cycle.

U.S. PMI drops to lowest since October 2020 amid soft demand conditions and labor shortages

January PMITM data from IHS Markit indicated a relatively subdued improvement in operating conditions across the US manufacturing sector. The headline figure dropped to the lowest since October 2020, as output growth was muted. Demand conditions also softened further, with new orders rising at the slowest pace since September 2020. Muted client demand was reflected in only a fractional increase in employment. The softer rise in new orders allowed firms to partially work through backlogs of work, which expanded at the slowest pace for 11 months. Nonetheless, firms were at their most upbeat regarding the outlook for output since November 2020.

Meanwhile, inflationary pressures remained marked. The rate of cost inflation eased to the softest for eight months, however, as firms also moderated the pace at which selling prices increased.

The seasonally adjusted IHS Markit US Manufacturing Purchasing Managers’ Index™ (PMI™) posted 55.5 in January, down from 57.7 in December, but higher than the earlier released ‘flash’ estimate of 55.0. The overall upturn was the slowest seen for 15 months and muted in the context of the substantial expansions seen in 2021.

Output rose only fractionally at the start of the year, following substantial increases through most of 2021. Weighing on the upturn was the impact of the Omicron COVID-19 variant, raw material and labor shortages, and a reluctance among some clients to place orders amid hikes in selling prices and longer lead times. The rise in production was the slowest in the current 19-month sequence of expansion.

Contributing to the slower output increase were softer demand conditions. The rate of new order growth slowed to a 16-month low as domestic and foreign client demand weakened. New export orders fell for the first time since October 2020, as delays dampened interest from foreign customers.

Mirroring softer demand conditions, firms expanded their workforce numbers at the slowest pace in the current 18-month sequence of job creation. Panellists often mentioned that growth of employment was hampered by challenges retaining staff and labor shortages, however.

Although still sharp, the rate of expansion in backlogs of work eased to the slowest since February 2021. Slower new order growth partially enabled firms to process work-in-hand, but material and labor shortages continued to push backlogs up.

Meanwhile, business confidence regarding the outlook for output over the coming year improved and reached a 14-month high in January. Firms noted that optimism stemmed from hopes of reduced supply-chain disruption, easing labor market difficulties and greater client demand.

Prices pressures eased at the start of the year, as the rate of cost inflation eased to the slowest since May 2021. The pace of increase was still marked, as firms sought to pass on higher costs to clients. Similarly, the rate of charge inflation softened and was the slowest for nine months.

At the same time, vendor performance deteriorated markedly. The extent to which lead times lengthened worsened from that seen in December, but was less severe than the substantial delays in mid2021.

Further hikes in input costs led to firms reining in their purchasing activity. Input buying rose at the slowest pace since February 2021 as firms utilised stocks of purchases in production. As such, the rate of growth in pre-production inventories eased to the slowest for ten months. Stocks of finished goods declined further, albeit at the softest pace in four months.

WHAT RESPONDENTS ARE SAYING

- “We are experiencing massive interruptions to our production due to supplier COVID-19 problems limiting their manufacturing of key raw (materials) like steel cans and chemicals.” [Chemical Products]

- “While there has been some improvement in materials making it to our factories and logistics centers, we are still constrained by (a lack of) qualified labor. Orders so far are not being cancelled, but we are concerned that customers may be losing patience.” [Computer & Electronic Products]

- “Transportation, labor and inflation issues continue to hamper our supply chain and ability to service our customers. Fortunately, it’s also hampering our competition as well. Ultimately, the biggest impact is at the consumer level, as (price increases) continue to get passed through.” [Transportation Equipment]

- “Our suppliers are having difficulty meeting scheduled releases as their suppliers experience delays and shortages, so lead times and inventories are struggling, resulting in lost production.” [Food, Beverage & Tobacco Products]

- “Lack of skilled production personnel, either from missing work due to (COVID-19) variants or leaving for better opportunities, making it more difficult to complete work. Working off a backlog.” [Fabricated Metal Products]

- “Strong backlog of orders coming into the new year. Potential to beat target revenue, depending on availability of purchased product.” [Electrical Equipment, Appliances & Components]

- “Bookings continue to increase as we are still dealing with a shortage of labor and supply chain issues.” [Furniture & Related Products]

- “Transportation restrictions and a lack of supplier manpower continue to create significant shortages that limit our production. This, in turn, limits what we can supply to customers, as well as on-time delivery.” [Machinery]

- “Integrated circuit availability is really causing issues. Shortages of raw materials and other electronic materials continue to hamper deliveries to our customers.” [Miscellaneous Manufacturing]

- “The supply chain crunch may be loosening a bit; however, specific original equipment manufacturer (OEM) parts and equipment now have lead times that we have not experienced before.” [Nonmetallic Mineral Products]

Eleven of 18 manufacturing industries reported growth in new orders in January, down from 13 in December.

- Commodities Up in Price: 35 vs 28 in December and 36 in November.

- Commodities Down in Price: 7 vs 8 in December and 5 in November.

- Commodities in Short Supply: 16 vs 10 in December and 21 in November.

US manufacturing growth is slowing, but not as rapidly as in China

Source: Macrobond, ING

U.S. Light Vehicle Sales Strengthen in January

The Autodata Corporation reported that light vehicle sales during January increased 19.3% (-10.0% y/y) to 15.16 million units (SAAR). Sales were at the highest level since June of last year but remained 18.1% below the April ’21 peak of 18.50 million units.

Sales of light trucks rose 21.6% (-7.1% y/y) last month to 12.05 million units, the highest level since last May. Purchases of domestically-made light trucks rose 20.8% in January (-7.4% y/y) to 9.40 million units. Adding to this increase was a 24.4% rise (-6.0% y/y) in sales of imported light trucks to 2.65 million units, though they remained below the April ’21 record of 3.30 million unit sales.

Trucks’ share of the light vehicle market increased to 79.5% last month but remained below an 80.4% share in October. For all of last year, the share was 77.5%, up from a low of 48.1% during all of 2009.

Passenger car sales rose 11.1% (-19.6% y/y) in January to 3.11 million units, the highest level since last August. Purchases of domestically-produced cars rose 10.1% last month (-21.8% y/y) to 2.08 million units following a 1.1% December increase. Sales of imported autos rose 13.2% in last month (-14.9% y/y) to 1.03 million units, the highest level since August.

Imports’ share of the U.S. vehicle market rose in January to 24.3%, though that remained down from a 27.9% September high. Imports’ share of the passenger car market rose to 33.1% last month but remained below the September high of 38.1%. Imports’ share of the light truck market increased to 22.0%, the highest level since September.

Regional sales breakdown of last year’s five largest EV sellers. Data: International Energy Agency via EV-volumes.com. Chart: Kavya Beheraj/Axios

Small Business Employment Watch

Small businesses represent nearly 95 percent of all U.S. employers. The Paychex | IHS Markit Small Business Employment Watch draws from the payroll data of approximately 350,000 Paychex clients to gauge small business wage and employment trends.

- The national index gained 0.39 percent in January, in line with its average monthly gain in the last six months of 2021. The gains were broad-based as all regions advanced in January. Annual weekly hours worked growth was essentially flat from December to January (-0.29 percent), though one-month annualized growth has been positive for the past four months.

- Leisure and hospitality (107.25) accelerated further ahead of other sectors, gaining 1.49 percent in January and 23.94 percent since last January.

- Up 4.43 percent year-over-year, hourly earnings growth remained at its peak level in January.

- Leisure and hospitality leads all sectors with hourly earnings growth of 10.95 percent, nearly double the next highest ranked sector, trade, transportation, and utilities (5.81 percent).

Euro-Zone Inflation Unexpectedly Hits Record, Testing ECB Stance

Consumer prices jumped 5.1% from a year ago in January, up from 5% in December. The median estimate in a Bloomberg poll of economists saw an advance of only 4.4%. None of the 44 analysts surveyed predicted inflation quickening. (…) Stripping out energy and other volatile components like food, core inflation was 2.3%, down from last month’s 2.6% reading. (…)

Some governments have stepped in to help households struggling with the soaring cost of energy, which shot up by 28.6% in January across the 19-member currency bloc.

There are also signs that supply disruptions are becoming less acute, while the statistical effect of a temporary sales tax cut in Germany is also disappearing, helping to bring down headline inflation there. (…)

Nordea:

The consensus expected both numbers to decline due to technical reasons. The dramatic change in weights inside the consumption basket in January 2021 and the base effect from a temporary VAT cut in Germany in 2H 2020, which artificially took inflation numbers up in January 2021, were now removed from the annual inflation numbers and were expected to take inflation down from December.

However, headline inflation rose marginally and given that the decline was smaller than expected in core inflation it seems that the inflationary pressures are indeed accumulating faster than expected. (…)

Although energy inflation is mostly transitory, the longer it lasts the stronger its second-round effects on wages and prices are likely to be.

There are signals that also the wider price pressures are stronger than expected. Although the non-energy industrial goods price inflation showed some signs of cooling off (partly due to temporary reasons), the monthly changes in service prices have continued to be strong. For example, in France the average monthly change in service prices over the past 3 months indicate higher annual numbers are in a pipeline and in Germany, service price inflation in monthly terms actually accelerated further in January, according to our estimates.

(…) given that the ECB has constantly underestimated inflation lately, it will be interesting to hear Lagarde’s formulation of the ECB’s view of inflation returning to below target next year. We still think the ECB will retain its baseline view, as it wants to see more data on especially wage developments, but it cannot deny the upside risks. However, even the discussion of upside risks is likely to feature stronger in the monetary policy account than the this week’s communication. (…)

- Lagarde rejects calls for ECB to act faster on inflation

- The Fed is too late to remove the punchbowl Policy is still aggressively loose, even though the recovery and surge in inflation have long been clear (Martin Wolf)

Omicron Flat-Lines Canada’s Economy at End of Strong Year

Gross domestic product was little changed during the month, Statistics Canada reported Tuesday from Ottawa. But that followed strong gains of 0.8% and 0.6% in October and November, respectively. Overall for the fourth quarter, the statistics agency said preliminary estimates show the economy grew by 1.6%, or an annualized pace of more than 6%. (…)

EARNINGS WATCH

We now have 184 companies in, a 79% beat rate and a +4.3% surprise factor.

Trailing EPS: $207.85, +27% from 2019. Full year 2022e: $224.25 +8.3%.

John Authers: Beating Expectations Isn’t What It Used To Be The pandemic-rebound mindset is over, and earnings calls are almost a sideshow as the market worries about inflation and rates.

Q4’21 was a given. The focus is on 2022 with all its headwinds:

(…) With modern data-crunching techniques, it’s possible to quantify the assessments that CEOs are offering. In general, they don’t inspire great confidence on the crucial macroeconomic issue of inflation, and the related corporate one of margins. For example, Subramanian shows that executives are no longer mentioning prices (and their chances to raise them) any more than wages (and the risk they will have to raise them) — and this turns out to be a bad sign for margins: (…)

National car crash crisis

The U.S. recorded its highest spike in traffic deaths since at least 1975, reports Axios’ Jacob Knutson.

- An estimated 31,720 people died in motor vehicle traffic crashes in the stretch between January and September 2021, up 12% from 2020.

- Fatalities increased in 38 states, the Transportation Department projected.

“This is a national crisis,” Transportation Secretary Pete Buttigieg said.