Milder Inflation Opens Door Wider to September Cut U.S. inflation eased substantially in June, to 3%, extending a recent slowdown in price increases that opens a path for the Fed to cut rates by the end of summer.

The consumer-price index, a measure of goods and services costs across the economy, fell slightly from May, dropping the year-over-year inflation rate to 3%, which was the lowest since June 2023.

Core prices, which exclude volatile food and energy items and are seen as a better gauge of underlying inflation, rose 0.1% [0.06% unrounded] since May. That was the mildest increase since January 2021, when large swaths of the economy were still frozen by the pandemic. (…)

San Francisco Fed President Mary Daly told reporters Thursday she expected interest-rate cuts could be warranted before too long but refrained from endorsing a move at the July meeting.

The decision over whether to cut rates at one meeting versus the next wasn’t particularly meaningful for the broader economy as long as “people understand where we’re likely to be headed,” Daly said. Placing more emphasis on maintaining a strong labor market, as Powell did this week, “is a fairly big communications signal” about where the Fed is moving, she said. (…)

Declines in large tech stocks pulled the S&P 500 lower on Thursday. But the Russell 2000, an index of small and midsize companies, posted a big gain, reflecting enthusiasm about the inflation report.

A move by the Fed to start cutting interest rates could be especially helpful to smaller businesses because they tend to have more floating-rate debt than larger companies.

U.S. Treasurys also staged a robust rally, driving their yields lower. The yield on the benchmark 10-year Treasury note settled at 4.192%, down from 4.280% Wednesday. (…)

- The slowdown in core CPI inflation was broad-based, with core goods prices once again declining and core services inflation advancing only 0.1% compared to the previous six-month average gain of 0.4%.

- Over the past three months, the core CPI has increased at a 2.1% annualized pace.

(…) Similar to the May CPI report — which Fed Chair Jerome Powell described this week as “really good” following an unexpected flare-up in the first quarter — the June reading will go a long way toward giving Powell and his colleagues the confidence they need to cut rates, likely starting in September. (…)

“Probably the most significant aspect of the June report is the downshift in housing inflation,” said Julia Coronado, the founder of MacroPolicy Perspectives LLC and former Fed economist. “It looks broad-based and durable, and numerous Fed officials have indicated a downshift would boost their confidence that inflation is indeed returning to 2% in a sustainable way.” (…)

After the CPI report, Treasuries rallied and traders all but fully priced in September and December rate cuts. They also marked up the odds of a reduction in November to better than even — a move that would come right after the presidential election. Before Thursday, traders and policymakers were divided as to whether there would be just one or two cuts this year. (…)

June BLS rent measures finally were where everybody has been wanting them (the black line is at +0.29 MoM, its pre-pandemic average). One month is not a trend, however.

Zillow rent growth averaged 0.23% MoM in the last 3 months. New leases are not declining as most everybody predicted. Housing remains very tight.

And the BLS data still need to catch up with “the market”.

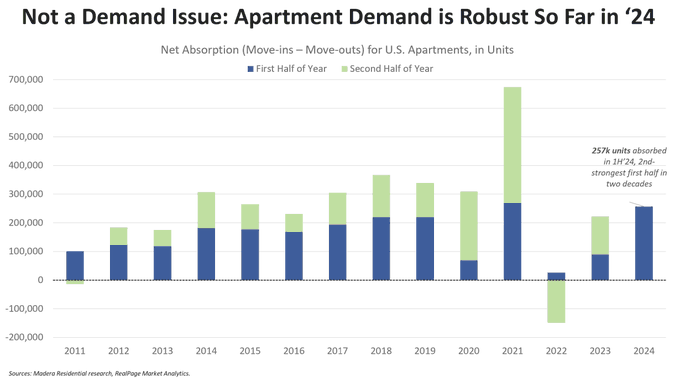

- The U.S. added 257k apartment renters in the first half of 2024, the 2nd-largest of any first half since 2000. (@jayparsons)

Cuts Are Back in the Air After Inflation Surprise So what if Powell’s congressional testimony was boring? He’s now got the data he needs, and markets are penciling in September.

(…) Investors are nearly 100% certain of a Fed cut in September. For that to happen, the next set of employment and inflation data must continue their current trends. With Powell indicating that he was worried by the risk that tightness in the labor market could put upward pressure on prices, a September easing looks almost certain should the next couple of employment reports show further pain. At 4.1%, the latest jobless rate is the highest since late 2021.

Bloomberg Economics’ Anna Wong argues that Powell’s first statement since the June jobs report was an important contrast to the Fed’s stance in the past two years, when it explicitly prioritized price stability:

Given our forecast for the unemployment rate to climb to 4.5% in 4Q, we expect that by year-end, the Fed will be prioritizing the employment leg of its mandate.

The following chart illustrates how hard jobs are to come by, with the number of people who have been unemployed for more than 15 weeks reaching its highest in more than two years. (…)

Before the June figures rolled in, Powell stressed the importance of “good inflation data” during his congressional testimony. With both headline and core CPI coming in weaker than expected, he now has what he wanted. It’s even more comforting that various statistical measures prepared by different research groups at the Fed all confirm the disinflation trend.

The Cleveland Fed’s trimmed mean measure, which excludes the most significant outliers in either direction and takes the average of the rest, fell to its lowest in three years. That trend is backed by the Atlanta Fed’s sticky price index, which concentrates on goods and services whose prices take a while to change and seldom fall. Surges in this measure are difficult to reverse, meaning any rise will unsettle the central bank. Although it’s still above 4%, the index is at its lowest in more than two years:

If the disinflation in CPI is good news, then the slowdown in services inflation, especially core services less housing — the so-called supercore — was even better. Since the start of the year, this metric has been running hot, but the latest print showed a consecutive month of decline, with the number coming in at -0.05% following -0.04% last month:

(…) Typically, slowing inflation is interpreted to mean consumer weakness, leading to a cut-down in discretionary spending. However, if the CPI data on food away from home is anything to go by, then consumers still have an appetite. ClearBridge Investment’s Josh Jamner suggests that the rise in the prices of this discretionary category should allay fears of consumer weakness. As shown in this chart, food at home remains relatively flat:

None of this proves that a Goldilocks economy is here. There are still risks in both directions. But as it stands at the moment, the chances that the economy can be landed safely, with the aid of some rate cuts, look much better than they did a few weeks ago.

- CPI Data Are Evidence Inflation on 2% Path, Fed’s Goolsbee Says Fed is tightening by not moving

(…) Two other policymakers also spoke following the latest consumer price index data. San Francisco Fed President Mary Daly said given recent data on employment and inflation, some adjustment to interest rates will likely be warranted — though she stopped short of offering a specific timeline for cuts.

St. Louis Fed chief Alberto Musalem suggested he needed some more convincing to lower borrowing costs. Musalem said the CPI figures pointed to “encouraging further progress towards lower inflation,” but he’d like more evidence of easing price pressures. (…)

Ed Yardeni:

We still don’t think rate cuts are necessary. Indeed, the Atlanta Fed’s GDPNow tracking model now estimates that real GDP rose 2.0% (saar) during Q2, up from the previous 1.5% estimate. Rate cuts could fuel the meltup given that there’s $6.15 trillion in money market mutual funds (chart).

- PepsiCo, After Years of Price Hikes, Sounds an Alarm on Consumer Spending Sales volume for PepsiCo’s Frito-Lay North America business dropped 4% in the latest quarter.

The snacks-and-soda giant reported a 1% increase in revenue and 2% drop in sales volume in the June quarter globally. Sales volume for its North America beverage business fell 3%. (…)

Shares of Conagra Brands declined in Thursday trading after the maker of Slim Jim meat snacks and Vlasic pickles reported lower sales for its latest quarter and issued a disappointing profit outlook for its current fiscal year. (…)

The Labor Market

Initial claims fell by 17k last week. It looks like claims are following last year’s unusual seasonal pattern, suggesting that labor demand is not waning much, if at all.

From Axios:

Just 13% of U.S. workers are now earning less than $15 an hour, compared to nearly 32% two years ago, per new Oxfam data.

Even accounting for inflation — $15 an hour in 2024 has the same buying power as about $14 did in 2022 — this is remarkable progress.

Oxfam revised its definition of a low-wage worker this year, from those earning less than $15 an hour to those earning less than $17.

- Fewer than 1 in 4 workers (23.2%) in the U.S. now fall into that category, the group says.

- That’s more than 39 million people, including 34 million who are over age 20, according to the report. (In 2022, many more workers — 52 million — earned less than $15 an hour.

Data: Oxfam; Chart: Rahul Mukherjee/Axios

Big Tech Tumbles Most Since 2022 as Rate Bets Spur Rotation Rate cut bets spark rotation out of Big Tech and into laggards

(…) The reshuffle led to some stunning stats. The S&P 500 dropped 0.9% even as nearly 400 of its members rallied. A version of the benchmark index that strips out market-cap bias surged 1.2%, beating the weighted index by the most since November 2020. The Russell 2000 Index — whose members tend to have lower credit ratings and higher borrowing needs — powered higher by 3.6%, its best performance relative to the S&P 500 since March 2020. And a Bloomberg index that tracks the Magnificent 7 tumbled 4.2%, its sharpest decline since October 2022. (…)

Steve Sosnick Chief Strategist Interactive Brokers:

A prolonged sell-off in some of the biggest names could pressure the main indices that investors watch, even if the majority of stocks remain initially unscathed. That in turn could cause investors to lighten their exposure to key index-based investments, such as ETFs like SPY and QQQ. If that occurs, then the selling could swamp the index as a whole, hurting the now laggard value stocks nonetheless.

They would outperform on a relative basis in that scenario but could still get swamped by selling anyway. Remember, when one buys a “diversified” SPX-linked index fund or ETF, about 35% of it is concentrated in the eight stocks referenced above. That is far less diversification than many investors realize.

China’s Record Trade Surplus Risks Further Straining Ties Exports rose to highest in almost two years while imports fell

Exports soared to $308 billion in June, expanding for a third straight month to the highest level in almost two years, the customs administration said Friday. Imports fell to $209 billion, leaving a trade surplus of $99 billion for the month. (…)

![]() The big shift in China export strategy continues:

The big shift in China export strategy continues:

- Exports to the US rose 6.6% YoY in June while exports to the EU increased 4.1%.

- Exports to ASEAN countries rose 15.0% in June.

This Goldman Sachs chart illustrates the rising importance of Latin American, ASEAN and African countries in China trade since the Trump presidency.

The One-Child Policy Supercharged China’s Economic Miracle. Now It’s Paying the Price. Revised U.N. data shows the speed of China’s aging after it accelerated its “demographic dividend.”

The policy supercharged the country’s workforce: By caring for fewer children, young people could be more productive and put aside more money. For years, just as China was opening its economy, the share of working-age Chinese grew faster than the parts of the population that didn’t work. That was a big factor in China’s economic miracle.

There was a price and China is now paying it. Limiting births then means fewer workers now, and fewer women to give birth. A United Nations forecast published Thursday shows how quickly China is aging, a demographic crunch that the U.N. predicts will cut China’s population by more than half by the end of the century. (…)

A young population has helped drive economic growth in developing countries across the world, including in China’s neighbor Japan starting in the 1950s. Economists call it a demographic dividend—the window, generally of a few decades, when a country has far more working-age people than young and elderly dependents. As such countries grow wealthier, people naturally choose to have fewer children and the population starts to age.

That was also the trajectory in China—just faster.

Knowingly or not, China essentially borrowed from its own future by accelerating its so-called demographic window. How the effects of the policy have sped up China’s demographic bind is scrambling the long-term models demographers usually work with. (…)

For example, in its just-published global estimates, the U.N. expects China’s population to drop from 1.4 billion today to 639 million by 2100, a much steeper drop than the 766.7 million it predicted just two years ago.

Even so, the U.N.’s prediction looks optimistic compared with other estimates. Researchers from Victoria University in Australia and the Shanghai Academy of Social Sciences have predicted that China will have just 525 million people by the end of the century. (…)

The population of Chinese aged 20-64—the age when people are most likely to work—grew faster than children and the elderly in the years after the one-child policy was implemented. Before the policy ended, the trajectories had already reversed.

The broader group of other countries shows a smoother ride with the demographic window lasting well into the 2040s. (…)

Now, slowing economic growth and demographic changes feed off each other for a gloomy outlook.

“People always count on the [Chinese] government to do more to prop up the economy but the reality is that there’s not a lot the government can do,” Wang said.

Over the next decades, China’s population is likely to show a contrast from, say, India, where the age distribution is following a more natural progression, or the U.S., where immigrant inflows help counteract the aging of the population.

By the end of the century, the U.S. population will be about two-thirds of China’s, compared with less than a quarter now, according to the U.N.’s latest projections. And by then, India, which has overtaken China as the world’s most populous country, will have more than twice as many people as China.

The real demographic impact in China won’t fully hit until the middle of the century, when many of those born during the one-child policy will reach retirement—while still caring for aging parents, said Wang.

By 2050, the U.N. now projects 31% of Chinese will be 65 or older. By 2100, the share will be 46%, approaching half of the population. In the U.S., the share is expected to be 23% and 28%, respectively.

The U.N.’s revised forecasts see Chinese births dropping below nine million this year. In 2022, it had predicted that 10.6 million would be born in China in 2024. The U.N. now expects China will have only 3.1 million newborns a year by 2100. (…)

China expects a glut of more than 40 million new retirees—more than the population of Canada—over the five-year period ending in 2025.

The old-age support ratio, a rough indicator of the number of workers for each retiree used by the Organization for Economic Cooperation and Development, is projected to decline from more than four now to fewer than two in 2050, according to The Wall Street Journal’s calculations of the U.N.’s latest data. It will likely reach one worker per retiree by the end of the century.

In reality, due to China’s low retirement age, with women clocking out as early as 50 and men at 60, the support ratio could be even lower. (…)

Republicans Are Fracturing on the Economy Skeptics of big business and free trade are at odds with libertarians over the agenda for a second Trump presidency

Republicans will gather for their convention in Milwaukee next week united behind presidential candidate Donald Trump but divided on what the party stands for.

There are, of course, widely aired disagreements over abortion and the war in Ukraine. But a potentially more consequential division has opened over economics. On one side is a pro-business libertarian wing that backs low taxes, free trade and international openness. On the other is a growing contingent of conservatives skeptical of big business, ambivalent about tax cuts and vocally supportive of tariffs.

While both wings back Trump, who straddles this divide, they have different priorities should Trump win this fall’s election and Republicans retake control of Congress. Which side prevails has huge implications for the economy and business. (…)

You can trace the origins of this intraparty split to the end of the Cold War in the early 1990s, which robbed Republicans of the common enemy that united social conservatives, national-security hawks and free-market libertarians.

In the 2000s, China’s rise—which hollowed out many manufacturing communities—along with wars in Iraq and Afghanistan and illegal immigration, discredited globalization and international intervention among the working-class voters who had become the Republican base.

Trump rode this shift to the Republican nomination in 2016 and then the White House. Beyond his love of tariffs, though, Trump has provided no holistic alternative economic vision. So others have filled the void. One is Florida Sen. Marco Rubio who, in a 2019 speech, pressed the GOP to be more pro-worker and less reflexively pro-business, criticized stock buybacks and praised an expanded child tax credit and industrial policy—that is, federal support for strategic sectors. (…)

A central tenet of this conservative view is that making things, i.e., manufacturing, is essential to balanced growth and national sovereignty. While supply-siders deride tariffs as taxes (except when imposed on China), Cass considers them essential to supporting manufacturing, a view shared by Robert Lighthizer, the former Trump trade ambassador, who is on American Compass’s advisory board. (…)

Besides free trade, national conservatives question Republicans’ deference to American corporations. Though not antibusiness, they abhor the boardroom embrace of progressive causes such as diversity, equity and climate change, and want to rein it in with whatever tools are at their disposal, from antitrust law to state authority over corporate governance.

“The widely held for-profit corporation is a threat…no conservative should let go unaddressed,” Ryan Newman, general counsel to Florida Gov. Ron DeSantis, who clashed with Walt Disney over Florida’s prohibition on classroom discussion of sexuality and gender, told a national conservatism audience.

These are the sort of interventions once championed by the left. Indeed, some Republicans are making common cause with Democrats. Sen. J.D. Vance of Ohio has praised Lina Khan, chair of the Federal Trade Commission, for taking on corporate mergers and big tech. Sen. Tom Cotton (R., Ark.) teamed up with Sen. Sherrod Brown (D., Ohio) to impose tariffs on steel imports from Mexico. Even Trump’s 2017 tax cuts, which slashed the corporate rate, are no longer sacrosanct. Before extending them, “We should start with this question: Why should labor ever be taxed more than capital?” Missouri Republican Sen. Josh Hawley said this week.

Supply-siders, who have driven the GOP’s economic agenda since the 1980s, are aghast. Steve Moore, a former editorial writer for The Wall Street Journal and now principal at the Committee to Unleash Prosperity, has called national conservatism “dangerous” and some of its causes, like protectionism and breaking up tech giants, “loony.”

“We’ve been fighting a war on the right against regulation for 40 years, and they want to regulate,” Moore said in an interview. Their obsession with manufacturing reflects a “romantic view of the past” rather than facts that show middle-class Americans getting steadily richer, Moore said. This week Americans for Tax Reform posted an article titled “Who Said it, Oren or Warren?” highlighting similarities between Cass’s views on taxes and those of Massachusetts Democratic Sen. Elizabeth Warren.

Which camp will prevail if Trump returns to power? Trump, famously transactional and nonideological, has advisers from both: Moore and Larry Kudlow from the libertarians; Lighthizer and former budget director Russell Vought, who align more with national conservatives.

Vought helped draft the Republican National Committee platform released this week. It backs tariffs but also tax cuts and deregulation. Trump has distanced himself from “Project 2025,” a national conservative agenda for the next president overseen by Heritage. Yet he is considering both Rubio and Vance, darlings of the new right, as his vice presidential running mate. (…)

With the Democratic Party drifting leftward, a Republican Party under the sway of national conservatives could leave business and libertarians homeless. Said Toomey: “The Republican Party has been advocates of limited government for 80 years. If that sentiment gets abandoned, where do people who believe in economic freedom go?”

China Hits Back at NATO After Rare Rebuke China warned the U.S. and its allies not to “provoke confrontation” after NATO took the unusual step of explicitly identifying Beijing as a threat to its interests.

The North Atlantic Treaty Organization described China as an enabler of Russia’s war in Ukraine and expressed concern over the expansion of China’s nuclear arsenal. It also accused Beijing of acting irresponsibly in both cyberspace and outer space in a staunchly worded statement issued Wednesday at its annual summit in Washington.

Chinese Foreign Ministry spokesman Lin Jin hit back Thursday with similar vigor at a regular press briefing in Beijing, describing NATO’s statement as “full of prejudice, smears and provocations.”

Lin said NATO is threatening China’s interests by extending its reach into Asia. He said the alliance should “avoid messing up Asia the way it messed up Europe.”

The decision by NATO leaders to dispense with diplomatic restraint over China reflects heightened geopolitical tensions as the war in Ukraine drags on, and as Beijing and Moscow push for an alternative to the U.S.-led global order.

NATO has generally avoided criticizing China, which fields one of the world’s most powerful militaries. The country didn’t appear in the alliance’s main guiding document, known as the Strategic Concept, until 2022, when Beijing was first openly identified as a challenge to its interests.

Since then, China’s posture on Ukraine, its military buildup and its alleged involvement in cyberattacks and disinformation campaigns inside NATO’s borders have raised the level of concern in the West.

In its statement, NATO called on China to cease all support for Russia’s war effort, including the provision of so-called dual-use goods that have both civilian and military uses.

China’s mission to the European Union criticized NATO’s depiction of China as a “decisive enabler” of the war in Ukraine. “China has never provided lethal weapons to either party of the conflict and has exercised strict export control on dual-use goods, including civilian drones,” the mission said.

Earlier in the week, Beijing said it would continue to promote peace talks and play a constructive role in pushing for a political settlement to the war.

NATO’s warning went viral on China’s heavily controlled social-media platforms, where it attracted a flood of nationalistic commentary as it rose to No. 1 on the list of hot topics on the popular site Weibo. Some said the statement signaled that China was NATO’s next target.

“They are wrapping up the war between Russia and Ukraine and can now spare a free hand to target us,” wrote one Weibo user in a comment that garnered more than a thousand likes.