U.S. SERVICES PMIs

S&P Global: Sharp rise in business activity as new orders return to growth

The seasonally adjusted S&P Global US Services PMI® Business Activity Index rose to a one-year high of 54.8 in May, up sharply from a reading of 51.3 in April. The index pointed to a marked expansion of services activity during the month. Output has now increased in each of the past 16 months.

The increase in business activity reflected a renewed expansion of new orders, which rose modestly in May following a first reduction in six months during April. Some respondents to the survey indicated that marketing activity had helped them to secure new business, while others pointed to improvements in economic conditions.

In contrast to the picture for overall new business, however, new export orders decreased for the fourth month running in May. Panellists reported that price rises had impacted external demand. Moreover, the pace of decline was solid and the fastest since January 2023.

Despite the pick-up in total new orders, service providers continued to lower their staffing levels in May, the second month running in which this has been the case. The drop in workforce numbers often reflected the non-replacement of leavers. The pace of job cuts was only slight, however, and weaker than that seen in April as some firms looked to hire staff in response to renewed growth of new orders.

Companies were still able to keep on top of workloads, as shown by a fourth consecutive fall in backlogs of work. That said, the latest reduction in outstanding business was only marginal and the weakest in the current sequence as higher new orders imparted some pressure on capacity.

While employment decreased further in May, higher staff costs were again the key factor behind a sharp rise in overall input prices as wages were increased. The pace of input cost inflation quickened from April and was sharper than the pre-pandemic average. Panellists also reported higher shipping costs.

Likewise, a faster increase in selling prices was recorded in May. Firms raised their charges at a solid pace, extending the current sequence of inflation to four years.

Signs of demand improving was a factor behind a slight strengthening of business confidence, which nonetheless remained softer than the series average. Other factors set to support growth of business activity over the coming year are planned marketing efforts, plus hopes for a softening of inflation and reduction in interest rates.

Looking at business trends across the combined manufacturing and service sectors, the S&P Global US Composite PMI Output Index* rose to 54.5 in May, up sharply from 51.3 in April. The index signaled a marked monthly increase in business activity, and one that was the strongest since April 2022. Growth accelerated across both the manufacturing and service sectors.

Companies increased output amid a renewed rise in new orders, following a slight fall in April. New export business also expanded, albeit marginally.

Meanwhile, employment was broadly unchanged as a solid increase in manufacturing was cancelled out by lower staffing levels in services.

Input costs continued to rise sharply,with the rate of inflation quickening in May. Selling price inflation also accelerated.

Finally, business confidence improved slightly from the previous month as companies remained optimistic that output will increase over the coming year.

Andrew Harker, Economics Director at S&P Global Market Intelligence, said:

“A return to growth of new business following April’s blip supported a marked strengthening of growth in the US service sector in May. Coming on the back of a similar acceleration in the manufacturing sector, the data suggest a healthy pace of expansion in the US private sector approaching the midway point of the year.

“It was not all positive in May, however, with services employment down for the second month running as firms wait to see whether the renewed rise in new business will be sustained before committing to new hires.

“Despite lower employment, wage pressures remained a key factor pushing up input costs, which increased sharply again in May and prompted a faster increase in selling prices, providing further evidence that inflation remains sticky.”

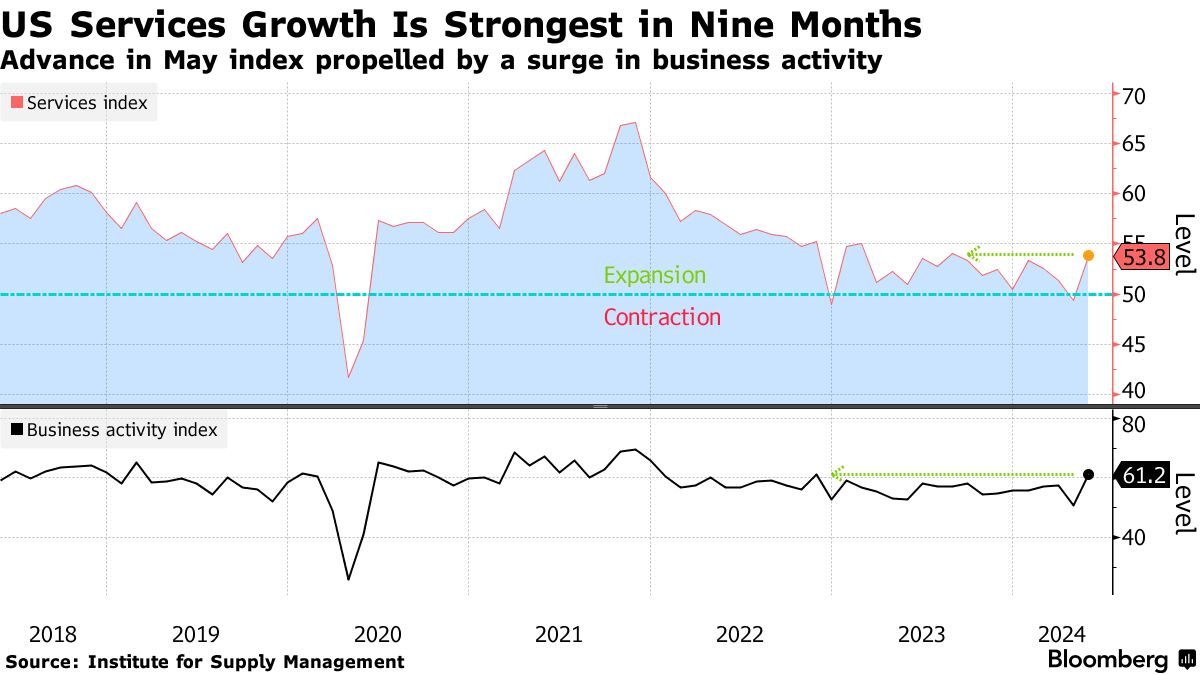

ISM:

In May, the Services PMI® registered 53.8 percent, 4.4 percentage points higher than April’s reading of 49.4 percent. The contraction in April ended a string of 15 months of services sector growth following a composite index reading of 49 percent in December 2022; the last contraction before that was in May 2020 (45.4 percent).

- The Business Activity Index registered 61.2 percent in May, which is 10.3 percentage points higher than the 50.9 percent recorded in April.

- The New Orders Index expanded in May for the 17th consecutive month after contracting in December 2022 for the first time since May 2020; the figure of 54.1 percent is 1.9 percentage points higher than the April reading of 52.2 percent.

- The Employment Index contracted for the fifth time in six months, though at a slower rate in May with a reading of 47.1 percent, a 1.2-percentage point increase compared to the 45.9 percent recorded in April.

- The Prices Index registered 58.1 percent in May, a 1.1-percentage point decrease from April’s reading of 59.2 percent. Wells Fargo notes that “not one of the 18 industries included in this release reported decreasing prices paid for the second consecutive month.”

- Thirteen [of 18] industries reported growth in May.

This Wells Fargo chart shows that the ISM Services index remains historically low, unlike S&P Global’s.

Demand for services was strong in May after being softish January to April. Both surveys note weak employment however. ISM respondents indicate weak retail/wholesale demand.

Both surveys signal continued wage and overall inflation pressures.

Canada Services PMI: Return to modest growth signalled in May

Underpinned by a rise in new business, Canada’s services economy experienced an increase in activity during May for the first time in a year. Modest growth encouraged staff recruitment in some cases, enabling firms to keep on top of workloads. Cost pressures remained significant, however, amid reports of higher salaries being awarded. Firms passed on these increased operating expenses wherever possible.

Bank of Canada Cuts Rates to Become First G-7 Central Bank to Ease Policy Gov. Tiff Macklem signals more cuts are possible as inflation cools

Canada’s central bank said a cut was warranted because officials are now increasingly confident that inflation is moving closer to their 2% target. Bank of Canada Gov. Tiff Macklem said more rate cuts could be in the offing should inflation show further signs of slowing, though he added the pace of reductions would likely be gradual. He also warned households, businesses and governments that rates are unlikely to return to pre-pandemic levels. (…)

The latest data for April estimated prices in Canada rose from a year ago by 2.7%—or the fourth straight month it was below 3%, which is the upper end of the central bank’s inflation-targeting range. The average of the Bank of Canada’s preferred measures of core inflation, which strips out volatile items like food and energy, cooled in May to 2.75%—the lowest level in nearly three years. Furthermore, Macklem said, the proportion of components in Canada’s consumer-price index basket that rose more than 3% is now closer to historical average.

“This all means restrictive monetary policy is working to relieve price pressures,” he said.

The Bank of Canada lowered its target for the overnight rate to 4.75% from 5%, where it sat for 11 months. Over a 16-month period ended last July, the Bank of Canada delivered 4.75 percentage points of rate increases to pull inflation down from a June 2022 peak of 8.1%. The sharp rise in interest rates has hit harder in Canada relative to the U.S., in part because of the country’s elevated household and corporate debt levels and its reliance on housing to drive growth. (…)

First-quarter gross domestic product in Canada rose 1.7% annualized, well below the central bank’s forecast of 2.8% growth, and inched up 0.5% from a year earlier. Per capita GDP has declined in six of the past seven quarters. Meanwhile, the unemployment rate sits at a 27-month high, and job vacancies have fallen to their lowest level in over three years. (…)

Bank of Canada’s Pivot Opens Path for Others to Diverge From Fed

Macklem made it clear that Canada’s interest rate policy doesn’t need to move in lockstep with that of its southern neighbor, despite the potential for downward pressure on the loonie. It was a bold signal that divergence in rates isn’t a huge concern for one of the largest US trading partners.

More central banks are weighing rate cuts, even as the Federal Reserve likely won’t start easing until later this year — if it cuts at all. The European Central Bank is expected to lower borrowing costs Thursday, while the Swiss National Bank and Sweden’s Riksbank have already pivoted to easier policy. (…)

- “The overall message from today’s statement and press conference was more dovish than we expected. While we continue to forecast cuts in September and December (for an additional 50bp of easing in 2024), we see a July cut as a clear possibility if upcoming inflation prints are in line with the recent trend.” (Goldman Sachs)

MONEY FLOWS…

Goldman Sees ‘Wall of Money’ Fueling Stock Market’s Summer Party Passive inflows, early July strength set up continuing rally

A flood of cash from passive equity allocations will pour into the stock market in early July, setting up a continuing rally through the early summer, according to Goldman Sachs Group Inc.’s trading desk.

“New quarter (Q3), new half year (2H), this is when a wall of money comes into the equity market quickly,” Scott Rubner, Goldman’s global markets division managing director and tactical specialist, wrote in a note to clients Wednesday.

In addition, share prices should benefit from strong seasonal trends and rising engagement from retail investors. “I am seeing a re-emergence in retail traders during the summer, they tend to come around in July,” he wrote.

Since 1928, the first 15 days of July have been the best two-week trading period of the year for equities, and they tend to fade after July 17, according to Rubner. (…)

By Rubner’s calculations, roughly nine basis points of new capital gets put to work every July. For this year, that would be $26 billion based on $29 trillion in passive assets available for investment. (…)

But it’s a one-way flow:

- “Investors who think today’s #stock market is somehow vastly different from 1999/2000’s #bubble simply aren’t paying attention.” (RBA)

-

Bear markets are rising in big tech

(…) One metric that can’t be explained away is the number of stocks in bear markets. We use the common definition of a 20% drawdown from the most recent 52-week high as a bear market.

Oddly, more and more NDX stocks are falling into that definition. This is a change from the initial phase of the rally and is quite similar to the rally in the fall of 2021, when the index rose while more of its stocks fell into bear markets.

Over the past 25 years, there have been more than 100 trading days when a divergence like this has been in effect. These are days when the NDX closed at a 52-week high, yet at least 13% more stocks fell into bear markets than the lowest level over the past year. In other words, the index was rising, but more and more stocks were off more than 20% from their highs. (…)

Warning signs have been building in recent weeks, particularly on the Nasdaq and, even more notably, among the tech stocks in the Nasdaq 100. The index has been doing just fine, but participation is lagging badly. These conditions can persist for weeks or even months, but forward returns over the medium term tend to be weak by the time they’ve reached the current levels. (…)

BTW: US antitrust enforcer says ‘urgent’ scrutiny needed over Big Tech’s control of AI Jonathan Kanter pushes for ‘meaningful intervention’ over concentration of power in artificial intelligence sector