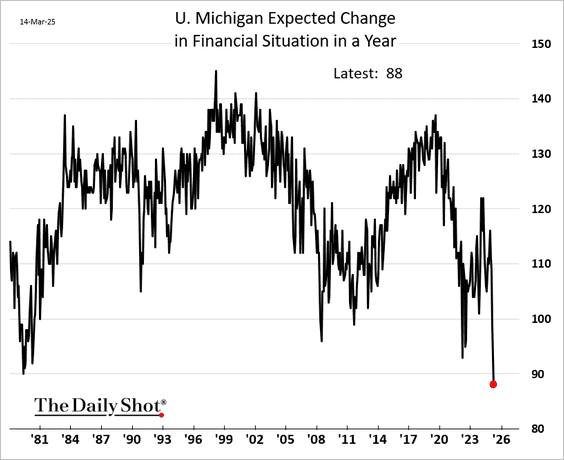

HARD SOFT DATA

CEOs won’t say it face to face but they are fearless with anonymous surveys:

Empire State Manufacturing Survey

Business activity dropped significantly in New York State in March, according to firms responding to the Empire State Manufacturing Survey. The headline general business conditions index fell twenty-six points to -20.0.

The new orders index fell twenty-six points to -14.9.

The index for number of employees held steady at -4.1, and the average workweek index was -2.5, pointing to a slight decline in both employment and hours worked.

Both price indexes climbed for a third consecutive month. The prices paid index rose five points to 44.9, its highest level in more than two years, and the prices received index rose three points to 22.4, its highest reading since May 2023.

Firms continued to grow less optimistic about the outlook. After dropping fifteen points last month, the index for future business activity fell another ten points to 12.7. Capital spending plans remained soft. Input price increases are expected to remain significant.

High inventories and declining orders are not a good recipe. The above is for manufacturing. What about services?

- Business Leaders Survey A monthly survey of service firms in New York State, northern New Jersey and southwestern Connecticut

Business activity fell at a substantial pace in the New York-Northern New Jersey region, according to the March survey. The headline business activity index fell nine points to -19.3. Nineteen percent of respondents reported that conditions improved over the month while 38 percent said that conditions worsened. The business climate index dropped sixteen points to -51.7, its lowest level in four years, with nearly 60 percent of respondents saying that the business climate was worse than normal.

The employment index was little changed at -4.7, indicating that employment levels continued to decline slightly. The wages index fell six points to 35.8, indicating that wage increases moderated somewhat.

The prices paid index moved up eight points to 58.8, its highest level in nearly two years, a sign that input price increases picked up. After rising eight points last month, the prices received index held steady at 28.7. The supply availability index was -2.8, suggesting supply availability was slightly lower.

The index for future business activity plunged twenty-five points to -3.3, its first negative reading since 2023, suggesting that firms on the whole do not expect activity to increase in the months ahead.

The index for the future business climate fell twenty-three points to -26.9, part of a cumulative decline of forty points over the past two months, suggesting the business climate is expected to remain worse than normal.

The future employment index fell to its lowest level since December 2020, with negligible employment growth expected over the next six months. The future supply availability index remained firmly below zero at -18.7, with about 31 percent of firms expecting supply availability to be worse in six months. Capital spending edged down

Let’s see how the FOMC deals with such hard soft data. Remember that Powell said “the economy’s fine” two weeks ago.

TARIFFS WATCH: In the Real World

- Last fall, Molson Hart ordered $100,000 worth of stuffed animals from China to sell through his Texas-based company, Viahart Educational Toy Co. In January, the toys were loaded onto ships for voyages across the Pacific Ocean and through the Panama Canal. In February and again in March, President Trump imposed new tariffs on China. The toys arrived in Houston on March 12, days after the 20% tariff took effect. The cost to Hart: an additional $20,000.

- Zach Frew, the co-founder of Boston-based Grounded Labs, contracted to place a container of his company’s devices, which make designs using sand art, on a ship leaving China on Jan. 29. But his shipment was bumped to a different ship at the last minute, a common occurrence in ocean shipping that usually adds time but not cost. Instead, this time, the container ended up departing Feb. 5 at an extra cost of nearly $23,000, as the products inside were by then subject to Trump’s 10% duty on all Chinese imports. Frew now has two more containers on the way that face estimated additional tariffs of $54,000 after the 20% levy kicked in. “It’s investments that we can’t make in the business,” he said.

- Jordan Dewart, president of Mexico operations for logistics provider Redwood Logistics, said one auto-parts shipment was hit with a bill for about $50,000 during the brief period the 25% tariff on goods from Mexico was in effect after the trucker carrying the load was delayed by a flat tire.

- “It’s going to cost me an additional $850,000 in additional tariffs that I did not plan,” said Gregorich, who noted that other levies could be placed on the shipments depending how his products are classified. “That’s a lot of capital it’s eating up.” Gregorich said he plans to raise prices to help cover the costs.

- “I was hoarding,” Shugar said. “I thought, I need to buy this because there’s going to be a tariff coming.” He said he loaded up on black fabric for tuxedo bow ties, bestselling solids like red and navy, and florals for the spring wedding season. He avoided tariffs on that shipment. But he now has less cash on hand to invest in his business. “My eye’s off the ball. I can’t focus on growth,” Shugar said. “It is chaotic for us as a small business.”

- Millions of dollars’ worth of wine is already paid for and on U.S.-bound ships, Fass says.

If those imports are suddenly hit with 200% tariffs on arrival, most importers simply won’t have the money to pay what they owe. - According to Bank of America aggregated credit and debit card data, small businesses are slowing their card spending across the board. Notably, for small manufacturing firms with annual revenues of <$500K, their payments growth fell 5.7% year-over-year (YoY) in February. Travel and hardware had a sharp deterioration in the past month, possibly as business looked to cut costs amid weakening demand and growing uncertainty. Across four major industries, manufacturing, finance and construction payments growth per small business client was negative in February while retail was positive.

-

Buy Canadian movement starts to take a sizable bite out of U.S. business

(…) U.S. tour operators are reporting booking declines of as much as 85 per cent, while American distilleries are losing major deals. Meanwhile, Canadian grocers are posting a bump in domestic product sales of up to 10 per cent. (…)

“To use some of the words I hear from tour company members of the National Tour Association, the drop-off is ‘astronomical’ when speaking about Canadians booking group travel to the United States,” said Catherine Prather, president of the Kentucky-based organization, which specializes in group tours.

One National Tour Association member operator reported just two bookings for U.S. tours in the past two weeks compared to 39 bookings during the same period in 2024, she said. Another Canadian operator, with 85 per cent of their business focused on tours to the U.S., had to scrap every U.S. departure for March, April and May due to client cancellations.

Ms. Prather said Canadian operators and hospitality businesses represent 7 per cent of NTA’s membership, with many focusing a chunk of their business on tours to the U.S. “One of those tour operators has just responded with the latest cancellations – his business will be down 75 per cent this year,” she said. (…)

Traffic across some major border crossings in tourism states such as New York has dropped by 12 per cent in the first two weeks of February alone, said Mr. Fram. (…)

The U.S. Travel Association warned in February that even a 10 per cent drop in Canadian visitors would lead to more than $2.1-billion in spending losses and a threat to 14,000 jobs. (…)

Sobeys Inc. parent, Empire Company Ltd., also reported a spike in Canadian product sales in its last quarterly results while purchases of U.S. goods as a percentage of total sales were “rapidly dropping,” according to CEO Michael Medline. (…)

Pierre Cléroux, vice-president of research and chief economist at the Business Development Bank of Canada, told The Globe and Mail that if every Canadian household redirected $25 a week from foreign products to Canadian ones, it would boost GDP by 0.7 per cent and create 60,000 jobs.

According to his modelling, if Canadians also cut international travel by 10 per cent and spent that money domestically, the combined effect would raise GDP by 1 per cent and create 74,000 jobs. (…)

- Germany’s Defense Splurge Set to Favor European Companies

-

U.S. trade actions have raised questions about validity of USMCA, Carney says “By applying unilateral tariffs for a variety of specious reasons, Trump has violated the very premises of the USMCA,”

BTW:

Import prices rose 0.4% in February, above expectations. Import prices ex-petroleum also rose 0.4%, above expectations. Prices for imports from China rose 0.5 percent in February, after rising 0.2 percent in January. The February advance was the largest 1-month increase since a 0.5-percent rise in March 2022.

Goldman estimates that the core PCE price index rose 0.34% in February (vs. our expectation of 0.29% prior to import prices data), corresponding to a year-over-year rate of +2.75%. Additionally, we expect that the headline PCE price index increased 0.30% in February, or increased 2.50% from a year earlier.

FLOWS MATTER

The Mag-7 companies may be the least fundamentally impacted by the tariff chaos. Yet they tanked the most.

The rotation out of US and into foreign stocks suggests that global investors have been mostly selling the Magnificent-7. Rather than buying the S&P 493 (as we’d expected), they’ve been buying foreign stocks with lower valuation multiples, especially Chinese technology and German industrial stocks (chart). In addition, thanks to Trump Tariff Turmoil 2.0, recession fears are more widespread in the US than in China and Germany, because the latter two are stimulating their economies.

The forward P/E of the US MSCI stock price index still well exceeds those of the other major MSCI stock price indexes. (Ed Yardeni)

Source: BofA Global Research

Source: BofA Global Research

- “The extraordinary returns for the US equity market over the past two years has really been driven to a meaningful amount by the seven large companies that go by the sobriquet the Magnificent Seven. Unfortunately from a portfolio management perspective, it’s been Maleficent Seven. It’s been the real source of pain in the market this year.” (Goldman Sachs’ David Kostin)

- “There have been significant inflows from abroad into US equity markets, and foreign investors are now significantly overweight US equities. Combined with the dollar’s decline and the ongoing overvaluation of the Magnificent 7, the downside risks to the S&P 500 as a result of foreigners selling are significant.” (Apollo’s Torsten Slok)