UNEMPLOYMENT INSURANCE WEEKLY CLAIMS

In the week ending December 12, the advance figure for seasonally adjusted initial claims was 885,000, an increase of 23,000 from the previous week’s revised level. The previous week’s level was revised up by 9,000 from 853,000 to 862,000. The 4-week moving average was 812,500, an increase of 34,250 from the previous week’s revised average. The previous week’s average was revised up by 2,250 from 776,000 to 778,250.

U.S. Retail Sales Post Broad-based Declines During November

Total retail sales including food service & drinking establishments declined 1.1% (+4.1% y/y) during November after edging 0.1% lower in October, revised from +0.3%. These declines followed five consecutive months of strong gains. A 0.3% sales decline during November had been expected in the Action Economics Forecast Survey. (…)

In the retail control group, which excludes autos, gas stations, building materials & food services, retail sales fell 0.5% (+9.5% y/y) following a 0.1% slip, which came after three consecutive months of roughly 1.0% improvement. Retail sales excluding restaurants declined 0.8% last month (+7.1% y/y) after easing slightly in October.

Sales of motor vehicle & parts dealerships fell 1.7% last month (+6.0% y/y), following no change in October and a 3.1% September improvement. This compares to a 3.1% fall in unit light vehicle sales reported for November. (…) As individuals stayed home due to the coronavirus outbreak, building materials & garden store sales firmed 1.1% (18.7% y/y) following two months of slight increase.

Sales of nonstore retailers improved 0.2% (29.2% y/y) following a 2.4% October gain. (…) Shopping in department stores continued to weaken as sales plunged 7.7% (-19.0% y/y), the largest of three declines in the last four months.

As individuals stayed home, food and beverage store sales jumped 1.6% last month (10.9% y/y), the first increase in four months. (…) Eating out was sharply reduced as restaurant and drinking establishment sales weakened 4.0% last month (-17.2% y/y), after strengthening for five of the prior six months.

It is not easy to get a clear picture of the fundamental trends in retail spending. The best measure in my view is Control Sales ex-food (stores and services). This series was rising at a 1.8% annualized rate in the pre-pandemic Aug-Jan period. It crashed initially in Feb-April but exploded since from spending on deferred needs and as unavailable services and the CARES act checks freed money for discretionary spending.

This is the trend in actual sales with the red line being the average since March which is 3.5% above the previous 9 months average, as close to reality as possible in my view.

The other reality is that sales have stalled MoM in October and dropped 1.1% in November as needs got filled and discretionary money declined.

Other data show that spending has continued to lag since the Thanksgiving holiday. JPMorgan Chase & Co.’s tracker of 30 million credit and debit cardholders recorded a 3.5% decline in spending from a year earlier in the week through Dec. 12. Credit- and debit-card data collected by research firm Affinity Solutions and research group Opportunity Insights showed that overall spending was down 1.7% in the week ended Dec. 6 compared with January levels. (…)

“We’ve got to be braced for a period of two, three, four months of extreme vulnerability for the economy,” James Knightley, an economist at ING Financial Markets LLC, said. Mr. Knightley expects gross domestic product to contract about 1.2% in the first quarter of 2021 after increasing around 1.5% to 2% in the fourth quarter. Mr. Knightley said he “can’t see containment measures wound down meaningfully until vaccination is at a critical mass.” (WSJ)

The U.S. Flash December PMI: Recovery momentum wanes amid rising virus cases and supply delays

Adjusted for seasonal factors, the IHS Markit Flash U.S. Composite PMI Output Index posted 55.7 in December, down from November’s 68-month high of 58.6. The rate of expansion was sharp overall, despite easing to a three-month low. The loss of momentum was most notable in the service sector, where additional restrictions and softer demand impacted consumer-facing business once again.

New orders continued to rise, and at one of the fastest rates since February 2019. Temporary shutdowns and client uncertainty weighed on the upturn, however. Although domestic demand continued to increase among manufacturing and service sector firms, companies registered a fall in new export sales. The decrease was the first since July, as renewed lockdowns in key export markets dampened demand from foreign clients.

As was seen during November, severe supply chain disruptions remained evident in December, with delays more prevalent than at any time since comparable data were available in 2007. As a result of demand rising but supply worsening, firms reported unprecedented supplier price rises. However, the impact of raw material shortages was exacerbated by a surge in the price of PPE. Although manufacturers raised their selling prices at the fastest rate since April 2011, seeking to pass higher costs on to customers where possible, service providers recorded a softer pace of charge inflation amid continual efforts to drive sales.

The outlook for output over the coming year remained upbeat in December, but was tempered by renewed uncertainty regarding the pandemic and surging costs. Business expectations fell to a three-month low. Hesitancy was also reflected in slower employment growth, as backlogs of work rose at only a fractional pace. Oustanding business increased further at manufacturing firms, who also stepped up their hiring efforts, but was unchanged among service providers.

The seasonally adjusted IHS Markit Flash U.S. Services PMI™ Business Activity Index registered 55.3, slipping from 58.4 in November. The rate of growth was the slowest for three months, albeit solid. As reported virus cases increased once again, firms stated that restrictions and softer demand weighed on total activity.

The rate of expansion in new business also lost momentum as clients, especially those of consumer-facing firms, reportedly expressed greater hesitancy in placing orders. Moreover, reimposed lockdowns in many key export markets led to the first fall in exports since May.

Meanwhile, service providers registered previously unseen increases in input prices during December. The rate of cost inflation accelerated once again to a new record high, as supplier prices and the soaring cost of PPE pushed cost burdens up. Firms only partially passed on higher prices, however, in an effort to boost sales.

Business confidence was relatively strong in December, despite slipping from that seen in November. The lower degree of optimism in a rise in output over the coming year reportedly stemmed from pandemic uncertainty and a weak global economic outlook.

At the same time, pressure on capacity waned and was unchanged from that seen in November, as firms slowed their expansion in hiring.

Manufacturing firms indicated the second-fastest improvement in operating conditions since April 2018, as highlighted by the IHS Markit Flash U.S. Manufacturing Purchasing Managers’ Index™ (PMI™) posting 56.5 in December, down slightly from 56.7 in November.

Although expansions in output and new orders remained strong overall, the headline figure was broadly sustained by the greatest deterioration in vendor performance since data collection began in May 2007. Supplier delivery times were extended following severe raw material shortages and supplier capacity and logistical constraints.

Consequently, input costs increased further in December, and at the sharpest rate since April 2018. Firms were able to partially pass-on higher costs to clients, however, as selling prices rose at the steepest pace since April 2011.

Although input buying rose once again, supplier delays led to the continued depletion of inventories, with stocks of finished goods falling at a sharper pace.

Encouragingly, manufacturers were historically upbeat regarding the outlook for output over the coming year, despite pandemic and economic uncertainty dampening expectations compared to those seen in November. At the same time, goods producers increased workforce numbers at a faster pace amid another monthly rise in backlogs of work.

I refer you to yesterday’s Daily Edge discussing the difference between actual production data and diffusion indices such as PMIs.

-

Lawmakers Near Virus Aid Deal Including Stimulus Checks “We’re still talking and I think we’re going to get there,” Senate Majority Leader Mitch McConnell (R., Ky.) said Wednesday afternoon.

The package under discussion was expected to include, along with direct checks, $300 a week in enhanced unemployment insurance, funding for vaccine distribution, schools, small businesses and health-care providers, rental assistance and other relief measures. Its size, at just under $900 billion (…). Lawmakers expect to attach the aid bill to a full-year spending bill needed to keep the government running after its current funding expires at 12:01 a.m. Saturday.

The aid package under discussion on Wednesday was expected to exclude the two thorniest issues: funding for state and local governments and liability protections for businesses and other entities operating during the pandemic, according to lawmakers. (…)

Senate Majority Whip John Thune (R., S.D.) told reporters Wednesday he expected the checks would be in the $600 to $700 range per individual. (…)

Fed Reinforces Plans to Provide Open-Ended Stimulus Most central bank officials also project interest rates will remain near zero for at least three years.

(…) The Fed has been buying $80 billion in Treasurys and $40 billion in mortgage bonds a month since June while pledging to maintain those purchases “over coming months.” On Wednesday, the central bank stated those purchases would continue “until substantial further progress has been made” toward broader employment and inflation goals. Officials don’t expect to reach those goals for years, according to projections they released Wednesday.

“Together these measures will ensure that monetary policy will continue to deliver powerful support for the economy until the recovery is complete,” Fed Chairman Jerome Powell said at a news conference after Wednesday’s meeting.

The projections show most officials thought they would hold short-term rates near zero for least three more years despite a somewhat more optimistic economic outlook than they had in September, before drugmakers had developed highly effective Covid-19 vaccines.

Many officials projected such low rates would be needed even though they projected inflation would be at the Fed’s 2% target and unemployment would fall below 4% by the end of 2023. Those projections reflect a change in the central bank’s framework adopted this summer that took a more relaxed view toward inflation. (…)

Mr. Powell said when the Fed believes it is close to meeting its new benchmark of substantial progress, “we will say so, undoubtedly, well in advance of any time when we would actually consider gradually tapering the pace of purchases.” (…)

Feeling Good?

Read at your own risk…

Goldman Says Tesla Inclusion Won’t Make S&P 500 Much Pricier

Although the electric carmaker’s eye-watering rally has pushed its shares near 170 times the consensus 2021 earnings estimate, its addition will only have a minimal impact on the benchmark’s valuations because of a nuance in index metric calculations, confounding the “instinctive conclusion” of many investors, Goldman strategists led by David J. Kostin wrote in a Dec. 16 note. (…)

“Given Tesla’s large size and elevated multiple, many investors erroneously intuit that the company’s inclusion into the S&P 500 will lift the index’s current 22x P/E multiple — which already registers close to the highest levels on record — by two multiple turns or more,” Kostin and his colleagues wrote. Instead, “it will lift the index P/E ratio by just 0.4 multiple turns.”

Directly from David Kostin:

The S&P 500 P/E multiple is generally calculated as total constituent market cap divided by total constituent earnings. Both metrics are adjusted for each company in proportion to the free float of shares, as determined by S&P. Mathematically, this calculation is equivalent to an earnings-weighted average of constituent P/E multiples, rather than a market cap-weighted average, because earnings is in the denominator of the ratio. Although Tesla will hold a 1.5% market cap weight in the index, based on consensus 2021 estimates its earnings will represent just 0.2% of the S&P 500 total.

Including Tesla’s expected earnings, the bottom-up consensus 2021 EPS estimate should move from $169 today to $167.

Kostin also calculated the cap-weighted P/E for our not-disinterested interest:

Tesla’s inclusion should lift the cap-weighted P/E by two turns, from 28.9x to 31.0x. That post-inclusion multiple will register at the 96th percentile since 1980, compared with a 99th percentile rank for the aggregate P/E.

One clear piece of evidence that investors do not typically use a market-cap weighted P/E multiple is that in late 1999 and early 2000 no one was discussing a forward P/E for the stock market of 45x. Instead, investors at the time were focused on the record high index P/E of 24x. Fast-forward to today, and the same disconnect exists. No one discusses a stock market trading at a P/E of 29x (the cap-weighted P/E) but investors are certainly focused on the current elevated P/E of 22x (the aggregate P/E).

Stepping back from the arithmetic of how index valuations are computed, investors then and now are acutely aware of the “super-cap premium” commanded by select companies. In 2000, CSCO and GE traded at forward P/Es of 130x and 40x, respectively. Today, AMZN trades at a forward P/E of 70x and TSLA trades at 170x.

Feeling better now? If you are, better not to read what immediately follows from Almost Daily Grant. You’ve been warned:

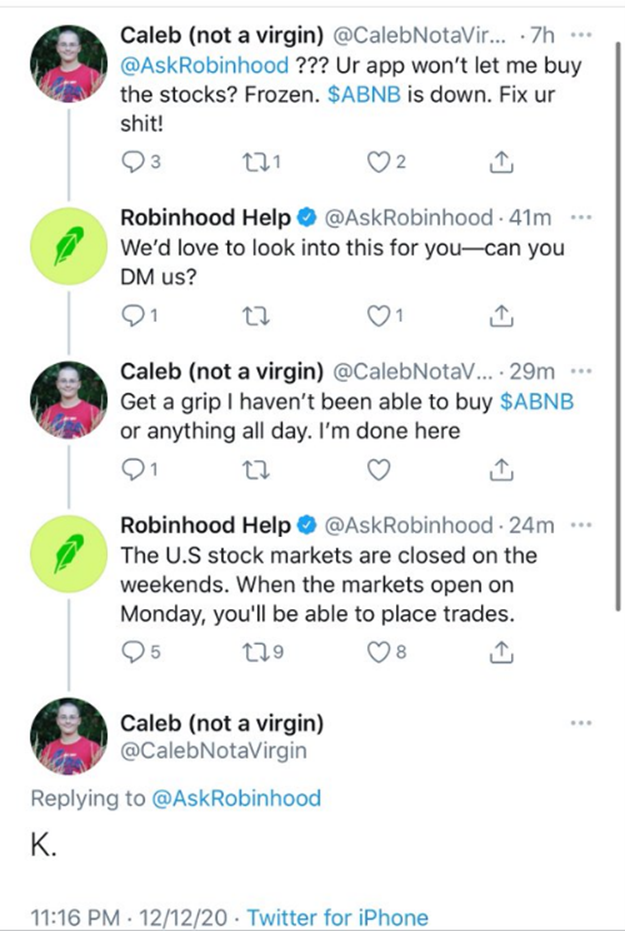

The Wall Street Journal reports today that the Massachusetts Securities Division’s enforcement arm accused the platform of exposing investors to “unnecessary trading risks,” and “falling far short of the fiduciary standard” requiring brokers to act in the best interest of the customer in providing investment advice.

According to the complaint, Robinhood permitted one novice punter to place more than 12,700 trades over a six-month period (or 101 trades per business day), while most in-state users who had engaged in options trading had either no experience or limited experience with the derivatives. Rather than framing its platform as “serious investing with substantial risk,” Robinhood is “presented as some sort of game that you might be able to win,” William Galvin, Secretary of the Commonwealth of Massachusetts, told the Journal.

Then again, you can’t win if you don’t play, as the following Twitter exchange demonstrates:

Caleb simply closed with a capital “K”, likely indicating his gratefulness for his education that U.S. equity markets are closed during weekends and also at 11:16pm. Go to bed boy, (not a virgin) (!), thanks for the info, we would not have guessed.

True story!!!! You know there will be blood. Just not when…

It reminded me when, about 20 years ago, my banker’s assistant, asked whether a deposit would hit my margin account by Friday, told me “don’t worry, there is no interest charged during weekends”. I wonder where she is working nowadays.

ADG also informs us that

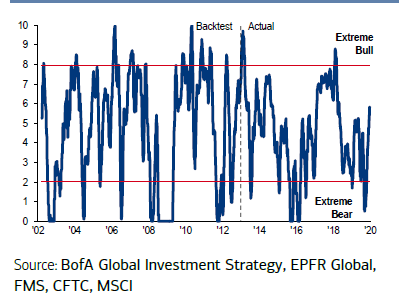

Bianco Research noted yesterday that some 1.94 million call options have changed hands using the CBOE’s rolling 22-day average, the most since 2011. The ratio of 2.37 calls per put over that period is the highest in at least 20 years.

That exuberance is helping facilitate some doubletake-inducing price moves. The 50-odd private equity-backed companies that have come public this year have achieved total market value increases of 660% (not a typo) on the first day of trading compared to their most recent private market valuations, Bloomberg reported over the weekend. “There is no doubt that the emergence of a much larger cohort of retail investors-slash-traders [is] moving markets,” commented Art Hogan, chief market strategist at National Securities Corp. “There seems to be an entire subculture of people that sort of follow the same things, talk to each other on social media and drive enthusiasm for individual issues. And sometimes it makes no fundamental sense to anybody.”

SentimenTrader adds that “this year has seen the fewest losing streaks in history. There have only been 32 days that were part of back-to-back losing sessions, the fewest since 1928.”

How do you fell now? Sorry! ![]()

Texas, nine U.S. states accuse Google of working with Facebook to break antitrust law

U.S. Stood Up by China at Military Safety Meeting The U.S. military accused China’s People’s Liberation Army of skipping a scheduled bilateral discussion, a rare snub that comes at a sensitive moment in the soured Washington-Beijing relationship.

Covid19

WHO vaccine scheme risks failure, leaving poor countries with no COVID shots until 2024 The scheme’s promoters say the programme is struggling from a lack of funds, supply risks and complex contractual arrangements which could make it impossible to achieve its goals.

Fortune’s David Meyer explains:

World Health Organization-affiliated COVAX is in big trouble, largely due to underfunding. Reuters reported yesterday that this factor, plus vaccine trial setbacks, distribution challenges and the complexity of supply contracts, meant billions of people could have no access to a vaccine until 2024. Just to reach its target of vaccinating a fifth of people in lower-income countries next year, COVAX needs $4.9 billion on top of the $2.1 billion already in its coffers.

So far, the biggest heroes in this story are the U.K. and the European Union—the former has pledged over $700 million for COVAX, and the EU has so far allocated over $1 billion to the effort—plus wealthy donors such as the Bill & Melinda Gates Foundation, which has committed $156 million.

Where’s the U.S. in all this? Nowhere, yet—the America-first Trump administration shunned COVAX back in September, because the World Health Organization is involved. The big question now is whether President-elect Biden will muster the U.S.’s considerable financial might (as the EU has asked him to do) to aid this globally crucial scheme.

Of course, Biden’s first concern will need to be the U.S.’s own terrifying COVID landscape. But make no mistake, the success or otherwise of COVAX will have considerable repercussions for the U.S., as it will for every other country. (…) the U.S.’s return to normal does not just rest on what happens within America’s borders.

Sweden’s king says country’s coronavirus strategy has failed Light touch approach has left it with far higher death toll than its Nordic neighbours

- New coronavirus cases are no longer skyrocketing, but are holding steady at record or near-record highs, Sam Baker and Andrew Witherspoon report. (…) The nationwide totals held steady even as the number of new infections fell in 19 states — including Iowa, South Dakota and several other states that were hit especially hard by the fall surge. A handful of populous states show significant increases, which is why the national total is still so high. California averaged roughly 32,500 new cases per day over the past week, an increase of almost 40% over last week.

Data: The COVID Tracking Project, state health departments; Map: Andrew Witherspoon/Axios

")

Red-blue COVID divide

States that voted for President Trump tend to have high coronavirus caseloads compared to how much COVID content they read online. The opposite is true of states that voted for President-elect Biden, Neal Rothschild writes from exclusive data from the social-media platform SocialFlow.

Thank You!

Thank You!

I wish to thank each and everyone of you who have generously contributed to Edge and Odds’ financial health through your donations. I try to always send a personal thank you note but I have been a little busy and I hope I did not forget anybody. Be sure to visit your SPECIAL FRIENDS PLACE (on the menu bar).

Best wishes and be safe with your family.

")

")