![]() Hmmm…More and more data and indicators that the U.S. economy is weaker than most people think.

Hmmm…More and more data and indicators that the U.S. economy is weaker than most people think.

Economic Outlook from Freight’s Perspective Negative Shipment Volume Hits Five Months in a Row

(…) Whether it is a result of contagion or trade disputes, there is growing evidence from freight flows that the economy is materially slowing. (…) since the end of World War II, there has never been an economic contraction without there first being a contraction in freight flows. (…) the volume of freight in multiple modes is materially slowing and suggests an increasingly bearish economic outlook for the U.S. domestic economy. (…) the Cass Shipments Index has turned negative and is now signaling economic stagnation with the potential for contraction.

(…) Beyond our concern that the Cass Freight Shipments Index is negative on a YoY basis for the fifth month in a row,

- We are concerned about the severe declines in international airfreight volumes (especially in Asia) and the recent swoon in railroad volumes in auto and building materials; (…) If the overall volume wasn’t distressing enough, the volumes of the three largest airports (Hong Kong, Shanghai, and Incheon) are experiencing the highest rates of contraction. Even more alarming, the inbound volumes for Shanghai have plummeted. This concerns us since it is the inbound shipment of high value/low density parts and pieces that are assembled into the high-value tech devices that are shipped to the rest of the world. Hence, in markets such as Shanghai, the inbound volumes predict the outbound volumes and the strength of the high-tech manufacturing economy.

- We see the weakness in spot market pricing for transportation services, especially in trucking, as consistent with and a confirmation of the negative trend in the Cass Shipments Index;

- As volumes of chemical shipments have lost momentum in recent weeks, despite the rally in the price of WTI crude, our concerns of the global slowdown spreading to the U.S., and the trade dispute reaching a ‘point of no return’ from an economic perspective, grow. (…)

Evidence is accumulating that this is more than ‘just a pause.’ (…)

Spot pricing (not including fuel surcharge) in all three modes of truckload freight (dry van, reefer, and flatbed) has already been falling for ten months. Spot pricing, using dry van as a proxy, has fallen 24.7% from its peak in June 2018 and is now 30.9% below contract pricing (which we see as unsustainable); The cost of fuel (and resulting fuel surcharge) is included in the Cass Expenditures Index, and since the cost of diesel was roughly flat (only up 0.9%) in April, we don’t see it currently as the driving factor; (…)

OECD Leading Economic Indicators Demonstrate Growing Weakness

(…) In terms of the level, all the LEI indexes are below 100 indicating a slowdown. The ratio to six months ago finds all countries/regions lower than six months ago and lower than the six months before that as well (except for Greece over the recent six months). (…)

The table also offers a look at the OECD LEIs ranked over all values since December 1994. Over that 24-year period, the strongest of the LEIs right now is in its 20th percentile decile in with none as high as their respective 25th percentile. France, Germany and Japan log the relative strongest LEI readings in March. The U.S. with a rank standing in its 15.8 percentile is one of the weaker country readings in the table, surpassed in significant measure only by the weakness in the U.K. The U.K. is suffering from Brexit fever, a long lasting and seemingly incurable ‘disease.’ (…)

The OECD LEIs are falling on a broad trend to weaker growth. With the U.S.-China trade conflict in gear and Brexit dragging on in Europe and both episodes will be further weakening global trends that already are sliding.

The OECD LEIs have slipped ahead of past recessions as much as they have weakened already. However, in recessions they slid quite a bit more after the recession began. China already has expended a lot of energy and run up already substantial debt levels to try to extend growth in the face of trade pressure. Yet, growth in China is about to come under even greater pressure. The U.S. has already used fiscal policy in this cycle. Central banks are for the most part already full stop on stimulus, the Fed being the main exception. While in the U.S. Federal Reserve is running a wait-and-see policy, it seems as though the bigger more dangerous and global risk is on the downside – not from inflation on the upside. We’ll see if policymakers figure this out in time or not.

Gundlach Says Weakness Appearing in U.S. Economic Indicators

(…) The probability of a recession in the next two years “would be extremely high,” Gundlach said. “Twelve months I’d give you a recession probability that’s 50-50. Next six months I’d probably have it down at 30%.” (…)

ZEW Global Expectations Are Set Back

ZEW macro-indicators of current conditions show some strengthening month-to-month. However, only the U.S. has a queue standings anything close to strong (in the 80th percentile). Japan has a firm standing in its 75th percentile with the euro area and France in their 60th percentile also solid but less firm standings. Germany, the U.K. and Italy have queue standings in the bottom 30th percentile range of their respective historic queues of data.

Moreover, all the country/region moving averages are weakening from 12-months to six-months to three-months. ZEW experts see widespread deterioration in current macroeconomic conditions.

Expectations are negative up and down the line. But contrarily, they show some gradual improvement – except for the U.S. where deterioration is quite modest. There is some significant improvement in Germany, France and Italy. Expectations standings are all below the 50% mark (below their respective medians). Expectations coalesce around the 25th percentile level or lower. These are very weak expectations. (…)

Trump Sees China Trade Deal ‘When the Time Is Right’ President promises to protect farmers hit by retaliatory tariffs and leans on Fed as fight with Beijing escalates

“When the time is right, we will make a deal with China,” Mr. Trump said on Twitter on Tuesday. “My respect and friendship with President Xi [Jinping] is unlimited but, as I have told him many times before, this must be a great deal for the United States or it just doesn’t make any sense.”

In remarks to reporters outside the White House later in the morning, Mr. Trump said the U.S. is having “a little squabble” with China, but he believes that a deal can “absolutely happen.” (…)

-

GOP senators raise alarms, criticize Trump as U.S.-China trade war heats up They say tariffs are hurting their rural constituents, and they’re considering options to aid farmers.

Goldman Sachs:

The main economic channel through which tariffs affect the US economy is higher inflation, and a couple of recent academic studies suggest that the impact from higher tariffs to date has been somewhat larger than previously estimated. Using very detailed data, they show that a) Chinese exporters did not absorb any of the tariffs in their profit margins and b) import-competing US producers raised their prices in response. Building on these studies, we now estimate that the Trump tariffs imposed so far—not only on China but also goods such as washing machines and steel—are currently boosting core PCE inflation by 0.2pp. That impact could rise to 0.6pp under the across-the-board tariff scenario (and to 0.9pp if the administration also imposes a 25% auto tariff). (…)

The risk to our 2½% growth forecast for the second half of 2019 has therefore moved to the downside.

China is likely to be hit somewhat harder in each scenario, but there are three reasons why we don’t expect growth to collapse. First, we estimate that Chinese value-added in exports to the US now amounts to only 2½% of GDP, partly reflecting rapid growth in the domestic economy over the past decade. Second, China is likely to cushion the impact of higher tariffs by allowing the renminbi to depreciate moderately. And third, our analysis suggests that most of the 2018 slowdown was caused by the fall in credit growth from 15% in late 2017 to 10% in early 2019, not the tariffs. With credit growth now more stable, our China CAI has reaccelerated from 5% to about 7%, despite the tariffs imposed to date. This is probably the near-term peak, but we still see growth stabilizing in a 6%-7% range, even with the renewed trade tensions.

China’s Economy Slows Ahead of Trump’s New Tariffs Economic activity in China cooled across the board last month, undoing a brief surge earlier in the year and raising questions about the vitality of the world’s second-largest economy.

(…) Value-added industrial output, a measure of factory production, rose 5.4% in April from a year earlier, slowing from an 8.5% year-over-year increase in March, the National Bureau of Statistics said. (…)

Retail sales rose 7.2% in April from a year earlier, decelerating from March’s 8.7% growth—the slowest pace in more than 16 years.

Investment in buildings, large machinery and other fixed assets also slowed to 6.1% in the January-April period, compared with a 6.3% pace in the first three months. (…)

Housing sales by value bucked the slowing trend, rising 10.6% in the first four months over the year-ago period, with the pickup likely owing to easier access to credit. That compares with a 7.5% increase in the first quarter. (…)

(

(Caveats: The March data was inflated by two one-offs: most important, a big cut to value-added tax from April 1. Even before the tariff news, manufacturers were probably rushing shipments to secure higher export tax rebates before the cut kicked in. Now comes the payback. On top of that, a late Lunar New Year holiday in 2018 meant a very weak March last year—and misleadingly strong year-over-year comparisons in 2019. (WSJ)

-

China: Expect faster activity growth after April’s weak data

(…) Industrial production slowed sharply to 5.4% YoY from 8.5% YoY. The slowdown is partly a result of the slower execution of infrastructure projects and partly the continuous disruption of ride-hailing apps on the production of automobiles. Automobile production fell 15.8% YoY in April from -11.8% in Jan-April.

Retail sales growth dropped to 7.2% YoY from 8.7% YoY. The slower growth is broad-based. This is worrying as April was a month when China’s stock market rose amid good progress in trade talks, so consumer sentiment should have been better. This is significant. We think it’s likely that some consumers were worried about their job security or wage growth and so tightened their purse strings. This is also reflected in the sales of clothing falling to -1.1% YoY from 6.6.%. When clothing sales shrink it signals consumers want to save rather than to spend.

We believe that the Chinese government will not wait for another set of data before it speeds up stimulus measures.

Premier Li mentioned recently that tax cuts needs to be implemented effectively. We believe an import-tax rebate for exporters could be possible. In addition, we expect that local governments, which control the speed of infrastructure project completions, will press contractors to speed up construction.

We also expect the People’s Bank of China to have targeted liquidity injection measures in May or June so that smaller exporters and their suppliers can get credit at a lower interest rate from banks. (…) (ING)

Germany’s Economy Rebounds Despite Darkening Trade Outlook

(…) The German economy expanded by 0.4% in the three months to March from the previous quarter, driven by vibrant private consumption and a booming construction sector, according to a first estimate published Wednesday by national statistics agency Destatis. (…)

The EU’s statistics agency Wednesday raised its estimate of annualized growth in the three months through March to 1.6% from 1.5%, an acceleration from the 0.9% expansion recorded in the final quarter of last year. (…)

U.S. Small Business Optimism Improves

(…) Expected pricing power fell sharply last month as 21% of firms were planning to raise prices. That was down m/m and lower than November’s ten-year high of 29%. Current pricing pressure improved. A net 13% of firms were raising average selling prices, up slightly m/m, but still below the 19% high last May.

Labor market readings showed modest m/m improvement. The 20% of respondents planning to increase employment was the most this year, but remained below the record 26% in August.

Pressure to raise worker compensation rose m/m as a higher 34% of firms were raising worker pay. The 20% that were planning to raise compensation was steady m/m, but down from the near-record 25% in November. (…)

From the NFIB report (with my annotations):

U.S. Import Prices Climb More Slowly Than Expected Figure for April is tied to strengthening dollar

Import prices rose 0.2% in April from the previous month, the Labor Department said Tuesday. Economists surveyed by The Wall Street Journal had expected a 0.6% advance. (…)

Import prices were restrained last month by a 0.6% decline in prices non-petroleum goods compared with March. Within this category of goods, the most striking components were capital goods and “non-petroleum industrial supplies and materials,” both of which saw the biggest monthly price declines since 2009. Consumer-goods prices fell 0.3% in April from March, while prices for autos and parts slipped 0.1%. (…)

The WSJ Dollar Index, which tracks the greenback against a basket of foreign currencies, has appreciated 2.3% since late January and is up 4.4% from a year earlier. The import price index was down 0.2% from a year earlier. (…)

In February, the Federal Reserve Bank of San Francisco estimated that tariffs implemented on Chinese imports at that time added 0.1 percentage point (ppt) to consumer price inflation and 0.4 ppt to price inflation for business investment goods. They forecasted an across the board 25% tariff on all Chinese imports would raise consumer prices by an additional 0.3 ppt and investment prices an additional 1 ppt. (Haver Analytics)

U.S. Embassy Staff to Leave Iraq as Iran Tensions Mount The U.S. ordered all its nonemergency staff to leave Iraq immediately, amid heightened tensions with Iran over recent attacks against oil tankers and facilities in the Persian Gulf region.

U.S. Embassy Staff to Leave Iraq as Iran Tensions Mount The U.S. ordered all its nonemergency staff to leave Iraq immediately, amid heightened tensions with Iran over recent attacks against oil tankers and facilities in the Persian Gulf region.

The decision comes amid fears that Iran-allied militia in Iraq could target U.S. citizens and soldiers in the country. (…)

The U.S., citing unspecified intelligence about increased Iranian threats last week, began a series of military deployments in the region that have included an aircraft carrier, a bomber task force and other ships and personnel.

Tensions in the region have sharply risen this week after a U.S. claim that Iran was behind attacks on four oil tankers near a strategic Persian Gulf waterway over the weekend. Tehran on Tuesday denied it was behind the attacks and said Washington and its Middle East allies were attempting to frame the country. (…)

While the U.S. and Iran in recent years have been careful not to get into a military confrontation, concerns have grown that a cornered Iranian regime could lash out, either directly with its own forces or through proxies, at Western facilities or perhaps those of the U.S.’s Arab allies in the Persian Gulf region. (…)

The WaPo editorial:

-

We’re drifting toward war with Iran. Trump needs to take a diplomatic way out. The president has cornered himself into bad choices.

BRITISH FOREIGN SECRETARY Jeremy Hunt concisely described the two big dangers embedded in the growing tensions between the United States and Iran. There is, he said Monday, “the risk of a conflict happening by accident, with an escalation that is unintended really on either side but ends with some kind of conflict.” And there is also the possibility that Iran will be put “back on the path to renuclearization.” What he didn’t say was this: Both those dangers result directly from the Trump administration’s escalation of pressure on the Iranian regime in recent months — a policy with no evident end goal and thus no plausible positive outcome.

President Trump and his top aides insist they are not seeking war, but the measures they have adopted in the past month — including an attempt to shut down all Iranian exports of oil, as well as steel, copper and other products — appear to have brought them perilously close to it. Facing an economic crisis, the Islamic republic has predictably responded by threatening to resume high-level enrichment of uranium — the most dangerous activity stopped by the nuclear deal that Mr. Trump unwisely scrapped.

(…) If Tehran is deemed responsible [for the attacks on tankers], Mr. Trump will come under pressure to deliver on threats of “a bad problem for Iran if something happens,” as he put it Monday. The Pentagon has dispatched additional forces to the region, and the New York Times reported that plans have been drawn up to send tens of thousands more U.S. troops.

The Times also reported on U.S. intelligence that Iran may be seeking to provoke Mr. Trump into a military action. If so, it’s not hard to see why. The United States is poorly prepared for another conflict in the region; it has the support of none of its NATO allies, not even — as Mr. Hunt made clear — Britain. The use of force probably would not stop Iran from resuming its nuclear program or force a change of regime, short of a full-scale military invasion. That would find scant support from Americans, and for good reason: Until Mr. Trump began his escalation, Iran was observing the nuclear deal and did not pose an imminent threat to the United States.

Mr. Trump says he’s interested in negotiating with the regime of Ayatollah Ali Khamenei, but it’s not clear his top aides agree with him; they have laid out a series of demands they know Tehran will not meet. Mr. Pompeo conceded the other day that the U.S. strategy was unlikely to coerce Iranian leaders into concessions, but suggested that “what can change is, the people can change the government.” But the United States has been waiting in vain for a popular revolution in Tehran for decades.

As we pointed out previously, Mr. Trump is in danger of being cornered into choosing between a counterproductive use of force and allowing Iran to cross red lines. The way out is to return to diplomacy, in concert with European allies. The president should curb his hawkish aides and take that course before it is too late.

- Iran and the US risk igniting the Middle East tinderbox

- Europeans warn Iran and US against triggering a conflict

Rising U.S. oil output helps fill gap left by Iran, Venezuela: IEA The world will require very little extra oil from OPEC this year as booming U.S. output will offset falling exports from Iran and Venezuela, the International Energy Agency said on Wednesday.

(…) “There is certainly scope for other producers to step up production,” it said, adding that it estimated OPEC states in April had produced about 440,000 barrels per day (bpd) less than the amount agreed in a production pact, with Saudi Arabia producing 500,000 bpd below its allocation.

The IEA said there was a “modest offset to supply worries from the demand side”, as it expected growth in global oil demand to be 1.3 million bpd in 2019, or 90,000 bpd less than previously forecast. It said 2018 demand growth had been estimated at 1.2 million bpd.

It said global oil demand would average 100.4 million bpd in 2019, exceeding 100 million bpd for the first time. (…)

U.S. production of oil and condensates was forecast to rise by 1.7 million bpd in 2019. Crude oil would account for about 1.2 million bpd of that rise, the IEA said, although it added that said this would be lower than U.S. crude oil output growth of 1.6 million bpd in 2018.

The IEA said reduced rig counts and maintenance in the Gulf of Mexico had affected U.S. output in the first half of the year, but an uptick in drilling permits and hydraulic fracturing, or fracking, early in the year would lift output.

China’s LNG tariff threatens Trump energy export goal A 25% levy means US liquefied natural gas would probably have to go elsewhere

EARNINGS WATCH

The earnings season is almost over. It has been a good one given the very low expectations. The beat rate is 75% and the surprise factor +6.1% leading to earnings rising 1.3% (+2.7% ex-Energy). Q2 estimates have not changed much, however (+1.1%, +1.2% ex-E). Pre-announcements are running slightly worse than at the same time during Q1’19.

Trailing EPS are now $163.78 following $161.93 for all of 2018.

TECHNICALS WATCH

Yesterday’s rebound showed little real enthusiasm and Lowry’s Research Bower Power vs Selling Pressure indices keep converging and are very close to reversing like near the end of October 2018.

The S&P 500 Equal Weight Index is also weaker than the weighted index.

Finished Tech Products Could Take Some Blows in Tariffs Fight Escalating volleys of tariffs by the U.S. and China stand to pile pressure on already stressed supply chains, potentially pinching technology companies and consumers on both sides.

Proposed tariffs by the U.S., released Monday, would hit finished technology products such as smartphones and smartwatches, as well as videogame consoles and other consumer products. Meanwhile, tariff increases ordered by China of as much as 25% affect some components that go into some of these products, including semiconductor packaging materials and certain types of displays. (…)

Sweden-based telecom-gear maker Ericsson AB is preparing to shift some manufacturing out of China to facilities in the U.S., Estonia, Brazil and Mexico, a spokesman said. (…)

Taiwan-based AsusTek Computer Inc. said last week that it has been moving some production bases to Taiwan and Vietnam from China to limit impact on a U.S. tariff increase on motherboards and graphic cards. (…)

Apple suppliers have said that fully moving out of China is difficult: China’s skilled workers and well-developed supply chain are difficult to replicate elsewhere in short order. (…)

Any fallout on Apple’s China production base could be troublesome for Beijing, too. Foxconn is the largest private employer in China, and the Chinese government wants to keep employment steady and prevent the trade fight from undermining a fragile recovery in the economy. (…)

One item on the U.S.’s proposed tariff list is made-in-China lithium-ion batteries. Those batteries are the most expensive component in electric vehicles, a sector China wants to dominate globally and has been subsidizing heavily.

A 25% tariff would make it tough for the Chinese imports to compete with batteries offered by Korea’s LG Chem Ltd. and Japan’s Panasonic Inc., which both already have U.S. production facilities.

Apple’s Supreme Court loss sends antitrust shock waves through Silicon Valley Apple’s loss in a high-stakes Supreme Court case on Monday could expose Silicon Valley to heightened antitrust oversight, threatening a slew of new lawsuits and other legal salvos that challenge the tech industry.

Apple’s loss in a high-stakes Supreme Court case on Monday unsettled Silicon Valley, threatening a wave of new consumer lawsuits and other legal salvos that could challenge the size and power of the tech industry.

For Apple, the 5-4 decision means that iPhone owners can proceed with a class-action case targeting the company’s App Store. The suit accuses Apple of engaging in monopolistic practices by forcing Apple device owners to buy developers’ games and other software only through the App Store, while Apple takes a cut of some of the sales made there. (…)

The ruling, in which conservative Justice Brett M. Kavanaugh joined the court’s four liberal justices, also could open the door for similar actions against a wide array of other companies such as Amazon, Google and Microsoft, all of which had urged the Supreme Court to side with the iPhone maker in legal briefs submitted by their top Washington advocates last year. (…)

The Supreme Court’s decision against Apple marks only the latest antitrust headache for the tech industry. (…)

")

")

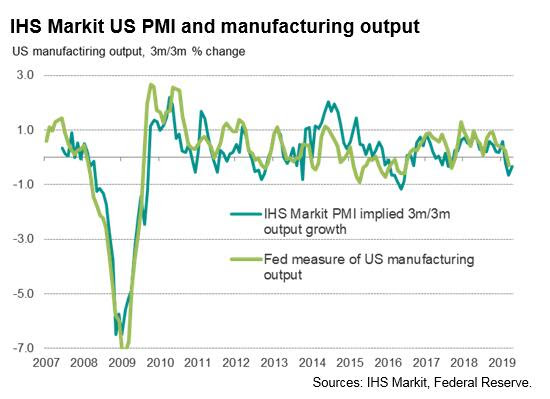

Expectations towards output growth over the coming year were also toned down in April. Companies’ expectations of future growth slid to one of the lowest seen since comparable data were first collected in 2012. Only mid-2016 has seen gloomier business prospects.

Expectations towards output growth over the coming year were also toned down in April. Companies’ expectations of future growth slid to one of the lowest seen since comparable data were first collected in 2012. Only mid-2016 has seen gloomier business prospects.

")

Related:

Related:

Source: Ned Davis Research

Source: Ned Davis Research