Longer than usual post. I hope it’s useful.

RECESSION WATCH

The Conference Board’s Composite Index of Leading Economic Indicators increased 0.5% (7.0% y/y) during September following an unrevised 0.4% August gain. A 0.5% rise had been expected in the Action Economics Forecast Survey. The index is comprised of 10 components which tend to precede changes in the overall economy.

Movement amongst the components of the index remained mixed last month. Improvement was paced by a rise in consumer expectations for business/economic conditions, a higher ISM new orders index, the leading credit index and a steeper interest rate spread between 10-Year Treasuries & Fed funds. Initial claims for unemployment insurance, stock prices, orders for nondefense capital goods excluding aircraft, as well as orders for consumer goods & materials also improved. The length of the average workweek for production workers and building permits had negative effects.

Three-month growth in the leading index held steady at 6.7% (AR), but remained below its 10.3% December 2017 peak.

The Index of Coincident Economic Indicators increased a lessened 0.1% (2.4% y/y) in September. (…) Three-month growth in the coincident index of 1.9% (AR) remained improved from 1.6% growth early in the year, but below its 3.6% peak as of December.

The Index of Lagging Economic Indicators eased 0.1% last month (+2.4% y/y) following an unrevised 0.2% August gain. (…) The three-month change in the lagging index fell to -0.4%, down from a high of 5.1% growth in February.

The ratio of coincident-to-lagging indicators is often considered to be another leading indicator of economic activity. As economic slack diminishes relative to current performance, the ratio will rise. It improved slightly to 99.1 last month.

These Advisors Perspectives charts flatly dismiss any thoughts of a U.S. recession anytime soon:

Steve Blumenthal shares his own recession charts

- None of his 5 indicators is currently flashing a U.S. recession.

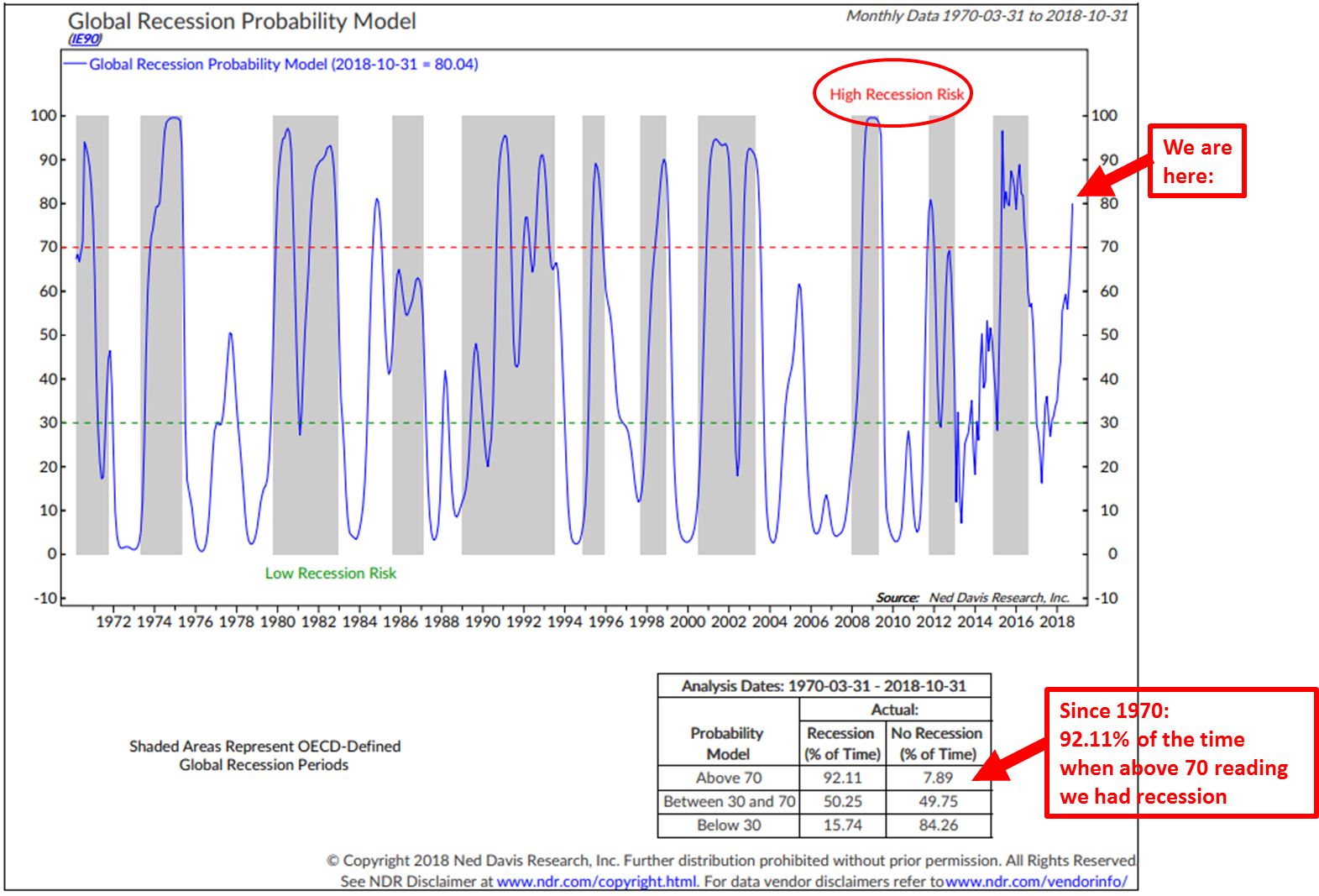

VanEck’s David Schassler shares this NDR chart which also signals strong odds of continued expansion:

However

- Expect a global recession. It either has begun or will begin shortly. Though no guarantee, as 7.89% of the time since 1970 when the global economic indicators that make up this model were above 70, a recession did not occur.

Since 1970, there have been 11 OECD-defined “global” recessions but only 6 of them also saw a U.S. recession. Years of “global” recessions saving the U.S. were 1986, 1995, 1998, 2012 and 2015-16.

Now, before Americans trumpet their cyclical domination, lets recall that, since 1950, the Fed has embarked on thirteen rate hiking cycles. Ten of these have resulted in recessions. The other three ended up in a so-called “soft landing” which is a term we will hear a lot in 2019 because this is what the Fed is trying to engineer in order to ease the demand pressures created by the Trump fiscal largesse when resources are already stretched.

The 1965-66 soft landing did not prevent a bear market. The 1983-84 and 1994-95 soft landings only saw a stock market correction but neither had serious inflation problems to correct and both occurred when the unemployment rate was still fairly high.

What about the yield curve, the almost infallible recession indicator? Shying away from inversion?

Jeffrey Gundlach sees a steepener and a lower dollar (Forbes).

It seems quite likely that the 30-year will be headed towards 4% in the not too distant future and that would mean a steeper yield curve. The movement now in the long end has been occurring faster than the changes in the perception of the Fed, which hasn’t changed much. The long end is going up by 50 basis points in a month, which is a pretty quick annual rate and will probably continue as long as we have this situation with moving higher rates. (…)

The U.S. 10-year has an uncanny tendency to find itself at the average of U.S. nominal GDP and the German 10-year yield. Right now, U.S. nominal GDP is at 5.4. We think we know it’s going to 5.75 once the data for the third quarter are announced.

So we might be seeing 5.75 nominal and 55 basis points of German 10-years, not even assuming that goes up. Add those two together, you get 6.3. Divide by 2, you get 3.15. Voila, that’s exactly where the 10-year is today.

Those are the two things that we need to be thinking about: nominal GDP of the United States and German 10-years are going to drive rates higher for 10-year treasury yields. (…)

We believe the dollar is going to go down. The fact that the dollar is starting to fall again enforces that view. When the dollar goes down, you’re going to be better off in emerging markets.

That is music to the ears of the FOMC.

That is music to the ears of the FOMC.

A strong economy is not a reason to buy equities. The big cyclical gains come from buying at the sound of cannons. Be careful when hearing the sound of violins as currently played by the media. Especially when the Fed is openly trying to soften the music…the odds are that it will entirely mute it. If that happens, a shortage of seats can surprise as Chuck Prince learned some 10 years ago:

The Citigroup chief executive told the Financial Times that the party would end at some point but there was so much liquidity it would not be disrupted by the turmoil in the US subprime mortgage market.

He denied that Citigroup, one of the biggest providers of finance to private equity deals, was pulling back.

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing,” he said in an interview with the FT in Japan.

So you think you can dance? Be aware of the contemporary debt mountain we’re all dancing on:

(…) In six short years, the outstanding value of leveraged loans in the US has doubled to $1.1trn, according to S&P Global Market Intelligence’s LCD. Europe’s share is smaller but it is growing quickly as well. As a share of new corporate issuance in the United States, highly-leveraged loan deals—where debt is at least 5 times ebitda —make up roughly half, surpassing levels seen in the lead-up to the financial crisis. In Europe, the ratio is even higher, at approximately 60 per cent. Here’s a chart from the IMF’s Financial Stability Report published earlier this month, which shows the growing dominance of leveraged loans:

(…) To put this into context, the leveraged loan boom comes at a time when governments, non-financial companies and households around the world have become awash in debt. Since the global financial crisis, which ushered in nearly a decade of quantitative easing and ultra-low borrowing costs, the non-financial sector in advanced and emerging market economies has fallen about $150trn in the red. That amounts to roughly 250 per cent of GDP. Here’s another chart from the same IMF report showing the surge:

(…) To put this into context, the leveraged loan boom comes at a time when governments, non-financial companies and households around the world have become awash in debt. Since the global financial crisis, which ushered in nearly a decade of quantitative easing and ultra-low borrowing costs, the non-financial sector in advanced and emerging market economies has fallen about $150trn in the red. That amounts to roughly 250 per cent of GDP. Here’s another chart from the same IMF report showing the surge:

(…) According to the rating agency Moody’s, roughly 80 per cent of US leveraged loans in the first quarter were considered “covenant-lite,” compared with less than 25 per cent in 2006 and 2007. (…)

Making matters worse, many of these leveraged loans are being packaged into collateralised loan obligations (CLOs) to be bought and sold by investors. Mutual funds have become major buyers of these instruments, and when the unwind comes—as is all but certain—here’s how the BIS thinks it could play out:

Mark-to-market losses could spur fund redemptions, induce fire sales and further depress prices. These dynamics may affect not only investors holding these loans, but also the broader economy by blocking the flow of funds to the leveraged credit market.”

Per the Fed, that most definitely sounds like a risk to financial stability.

Speaking of mark-to-market, here’s how this rather unknown accounting rule to many young investors, can impact you:

Oups!! OZK lost 27% to $25 last Friday. The stock was $50 last July. The bank announced Friday that it is taking a $45m writedown on two commercial real estate (CRE) loans secured by a mall property in South Carolina and a residential development in North Carolina. The mall had a Sears store and the resid credit turned sour after high end units did not sell as expected.

Since the summer, OZK has seen its equity value shrink by $3.2B, 72 times the markdown, a pretty large “loss multiple” if there is one. BTW, OZK’s loan portfolio, per the WSJ, is $14.4B. Mr. Market just marked it down by 22%.

Here’s what George Gleason, OZK’s Chairman and CEO for 40 years, told Chris Whalen of the Institutional Risk Analyst back in August 2017:

Real Estate Specialties Group (RESG), our large real estate group, does business across the nation with many of the best sponsors on many of the best properties on extremely conservative terms. At June 30, 2017, assuming every loan in the group was fully advanced, our weighted average loan-to-cost would be about 49% and our weighted average loan-to-value would be about 42%. We are extremely conservative, approving a mid to low single digit percentage of the loans we see. Because of our expertise in CRE and the value we bring to our clients, we see a huge volume of business and that allows us to be very selective.

The bank has practically no debt (0.09 D/E) and the stock is now selling below book. Not a recommendation in any way. Just to show how Mr. Market can react to bad surprises, such as mark-to-market. The last time the stock was $25 was in 2013 when EPS were $1/sh. Q3’18 EPS were $0.58 after the markdown.

It’s been a while we’ve heard about deflationary trends:

The National Association of Realtors reported that sales of existing homes during September declined 3.4% to 5.150 million (SAAR, -4.1%). August’s figure was revised slightly lower to 5.330 million. Sales have declined for six consecutive months and were at the lowest level since November 2015, off 10.0% from the November 2017 peak. Expectations had been for 5.31 million sales in the Action Economics Forecast Survey.

The median price of all existing homes sold declined 2.8% last month (+4.2% y/y) to $258,100. Prices hit a record $273,800 in June. The average sales price fell 2.4% (+2.5% y/y) to $296,800.

By region, home sales in the South declined 5.4% (-0.5% y/y) to 2.110 million units, the lowest point since November 2015. Home sales in the West fell 3.6% (-12.2% y/y) to 1.080 million, also equaling the 2015 low. Home sales in the Northeast fell 2.9% (-5.6% y/y) to 680,000 units. Sales in the Midwest held steady m/m (-1.5% y/y) at 1.280 million units.

Sales of existing single-family homes fell 3.4% last month (-4.0% y/y) to 4.580 million units. Sales of co-ops & condos declined 3.4% (-5.0% y/y) to 570,000 units.

The number of homes on the market increased 1.1% y/y. (…)

(…) Banks have spent much of the past 10 years chasing ultra-creditworthy borrowers. Yet that slice of the market, which has grown as the economy has improved, is largely tapped out.

As a result, lenders have been asking credit-reporting firms and FICO to figure out a way to help them boost lending without taking on significantly more risk. And regulators have expressed interest in exploring ways to increase access to affordable lending for consumers who have no or low credit scores. (…)

FICO said about seven million applicants who have low credit scores as a result of thin borrowing histories would likely see their scores improve under the new system. Separately, some 26 million subprime borrowers will end up with higher credit scores, FICO said, with nearly four million seeing an increase of at least 20 points.

Consumers with an average balance of at least $400 who haven’t overdrawn in the prior three months would likely get a boost, FICO said. (…)

What did Mark Twain say about history not repeating itself but…?

(…) the Cass Freight Shipments Index is clearly signaling that the U.S. economy, at least for now, continues to be extraordinarily strong. Simply stated, when shipment volume is up 8.2% it is the result of an expanding economy. We are hard pressed to imagine a scenario, barring a catastrophic geopolitical event, in which such a strong rate of freight flow expansion was possible or even a precursor to an economic contraction.

Our confidence in this outlook is emboldened by the knowledge that, since the end of World War II (the period for which we have reliable data), there has never been an economic contraction without there first being a contraction in freight flows. Conversely, during the same period, there has never been an economic expansion without there first being an expansion in freight flows.

The Cass Expenditures Index is signaling continued strong pricing power for those in the marketplace who move freight. Demand is exceeding capacity in most modes of transportation by a significant margin. In turn, pricing power has erupted in those modes to levels that continue to spark overall inflationary concerns in the broader economy.

With the Expenditures Index up 19.3%, we understand those concerns, but are comforted by two factors: the cost of fuel (and resulting fuel surcharge) is included in the Expenditures Index and the cost of diesel was up 17.3% in September; almost all modes of transportation are using the current environment of pricing power to create capacity. Especially to the extent that pricing is materially exceeding the marginal cost of creating that capacity, market participants are investing heavily in the exact activities which kill pricing power in commodity markets (i.e., expansion of capacity with the belief that current pricing power will endure for an extended period of time).

Cass says that its data confirm that there has been advanced buying to beat import tariffs earlier this year and that import volumes declined as a result in July and August.

Having now worked past that period, September inbound volumes were up 2.3% which is clear evidence that the retail economy is continuing to grow.

The proof is in the pudding: freight costs continue to explode with September’s apparent inflation rate reaching 10% YoY.

The consumer price index recorded an annual pace of 2.2 percent, the lowest in four months and a drop from 2.8 percent in August, Statistics Canada said Friday from Ottawa. Economists had expected inflation of 2.7 percent. Core measures of inflation — considered a better indicator of underlying pressures — also ticked lower and averaged 2 percent last month. (…)

- Monthly inflation dropped 0.4 percent in September, versus analyst expectations for a 0.1 percent gain. It’s the largest monthly drop this year and the first back-to-back monthly declines since 2016 after prices fell 0.1 percent in August

- On a seasonally adjusted basis, prices were down 0.1 percent, the first month over month drop since May 2017

- All three measures of core inflation fell. The “common” rate dropped to 1.9 percent from 2.0 percent, the “median” declined to 2.0 percent from 2.1 percent and the “trim” rate fell to 2.1 percent from 2.2 percent

So many ways to skin a cat, particularly in China. There was a deluge of stats last week. Let’s see if we can make some sense out of them:

- GDP in the third quarter grew 1.6%, compared with growth of 1.8% in April-June.

- Electricity output growth, meanwhile, slowed from 7.3% YoY in August to 4.6% in September.

- Retail sales grew 9.3% in the first three quarters of 2018, a sharp drop from 10.4% in the year-earlier period.

- Real retail sales rose 7.3% during the first three quarters, down from 9.3% during the same period last year and 9.8% two years ago.

- Auto sales by larger firms rose 0.2% YoY during the first nine months of this year, after rising 6.2% during same period last year, apparently a consequence of the government’s efforts to de-risk the financial system.

- Retail sales growth rebounded in September, picking up to 9.2% YoY from 9.0% in August. Ex-autos, retail looks ok.

- New home sales rose 3.3% (on a square meter-basis) during the first three quarters, compared to 7.6% during the same period last year. “That is impressive given that more than 100 cities have implemented purchase restrictions designed to cool the market. And these sales involve a lot of cash: the minimum down payment is 20% of the purchase price and most banks require 30% cash.” (Andy Rothman)

- The consumer story continued to be supported by strong real income growth (6.6% YoY during the first three quarters of this year, vs 7.5% during the same period last year), mild consumer price inflation (2.5% in September), high household savings and low household debt. (Andy Rothman)

- Infrastructure investment rose by only 4.2% during the first eight months of the year, compared to a 19.8% pace during the same period in 2017. But Beijing allowed work on previously planned projects to resume last month, and while infrastructure investment still declined 1.8% YoY, the decline was 2.5 percentage points less than the decline in August. Investment in real estate, which accounts for about 22% of total FAI, rose 7.9% during the first eight months of the year (the latest available data), compared to 5.1% during the same period last year, as inventories of new homes declined. (Andy Rothman)

- Manufacturing capital expenditure, which accounts for about 31% of FAI, rose 8.7% in the first three quarters, up from 6.8% during the first half of this year and 4.2% in the first three quarters of last year. Investment by privately owned (as opposed to state-owned) firms rose 8.7% during the first three quarters. (Andy Rothman)

- Chinese exports grew at an average monthly pace of 11.7% during the third quarter, a slight improvement from an average of 11.5% monthly growth in the quarter before. Much of that burst, however, came from manufacturers racing to fill holiday orders and ship out goods before the trade conflict gets worse. That, in effect, is borrowing from future growth.

- Exports to the U.S. rose 14% YoY in September, the fastest pace of the last seven months, and roughly the same as a year ago.

- Growth in the construction sector slowed to 2.5% from a year earlier compared with 4.0% in the previous quarter

- The financial sector also grew at a slower pace of 4.0% while information technology continued to expand at a fast clip of 32.8%, compared with 31.7% in the second quarter.

- Manufacturing growth further slowed to 6.0% from 6.6% in the second quarter

- Third-quarter services growth edged up to 7.9% from 7.8% in the second.

- The services sector accounted for 53.1% of GDP value in the first three quarters, slowing from 54.1 in the first half, while consumption contributed 78% to growth in the six-month period.

At the Canton export fair, some Chinese vendors said they could make up for some reduction in U.S. orders by selling to other countries. Others boasted that their clients were already thinking about ways to reroute shipping via Taiwan, Mexico and other places not subject to higher U.S. tariffs. A common pitch: China remains No. 1 in the world at delivering well-made products at competitive prices.

China has become primarily a domestic consumption story and recent stats remain quite positive. The Chinese economy is not about to collapse. Good thing for everybody except, perhaps, for the hard core occupants of the White House.

Independent data shows that the Chinese economy is fairly stable within a narrow 52-53 range on the Markit PMI scale in spite of the heavy turbulence, underscoring its reduced dependence on foreign trade.

(…) China was the top spot for foreign direct investment globally in the first half of 2018—with investment up 6% to $70 billion, according to a United Nations report—edging out last year’s champion, the U.S. Chinese figures also put FDI already put to use up 6.4% through September year to date, the fastest since 2015. (…)

Inflows to real estate were up 31% in the first eight months of 2018 compared with the same period last year. But manufacturing investment has recovered strongly, too, rising by almost 13% year to date through August, a big turnaround considering that such investment fell for 22 straight months from late 2015 to early 2017. (…)

Since 2014, Hong Kong, Taiwan, Japan and Korea have accounted for close to 80% of direct investment into mainland China, up from just 46% in 2008.

In other words, although China has shot itself in the foot by antagonizing U.S. companies, its intrinsic advantages remain substantial: world-class infrastructure, an educated and still-cheap labor force, and, most of all, scale. (…)

(…) Taxpayers can claim deductions for expenses on health care, education, mortgage interest or rent and supporting elderly relatives, state-run Xinhua News Agency reported, citing the draft plan released by the Ministry of Finance and State Administration of Taxation. (…)

The announcement had been widely expected after China raised the personal income tax-free threshold to 5,000 yuan per month from 3,500 yuan earlier this year. (…)

From Justin Leverenz, manager of the Oppenheimer Developing Markets funds via Barron’s:

About 20% to 30% of the incoming undergraduates at top U.S. schools are Chinese, as are about half those in U.S. graduate schools in life sciences, physics, and math. China has the world’s most significant pool of intellectual talent; it has a lot of capital and a lot of data—whether in ride-sharing with DiDi, commercial data with Alibaba Group Holding [BABA], or transactional data with Alibaba’s Alipay.

Data is the fundamental ingredient in artificial intelligence and algorithms. China is going to be a formidable competitor, and there are some wonderful opportunities to invest in, including Alibaba, arguably one of the most audacious companies on the planet. But the U.S. can’t permit the rise of China as an equal, and Beijing doesn’t have the domestic political capacity to make significant concessions, so this tension is going to be a permanent state of affairs.

The Art of the Deal:

The Art of the Deal:

In an interview with the Financial Times, Larry Kudlow, director of the National Economic Council, complained that China had offered no sign that it was willing to meet US demands in a way that could lead to a breakthrough.

Kudlow said that the problem is that “they don’t respond. Nothing. Nada.” “I’ve never seen anything like it”.

Looks like things are not going according to plan. Like NAFTA which was concluded at the last minute, after passing 7 deadlines, with a face-saving reshuffling of letters.

Is Kudlow sending a message, like “help us help you” in Chinese?

Here’s the olive branch?

But Mr Kudlow said he believed the weakness of the Chinese currency recently was because of market forces rather than any deliberate policy.

When is the last time Kudlow was so nice with the Chinese? I bet it was on Halloween days many, many moons ago, begging people to slip coins into his Unicef box.

Let’s watch the renminbi now, already down 10%, essentially offsetting current tariffs.

Lastly, the crucial factor: “The thing that worries me the most is a blue wave in two weeks,” he said.

Unlike the FT, I think this increases expectations of a truce.

OIL

For the third consecutive year, the only source of non-OPEC supply growth has come from the U.S. shale oil fields.

Goehring & Rozencwajg Associates, an investment company focused on natural resources, warned last September of a coming slowdown in U.S. shale oil production growth.

While shale oil in the United States has been a terrific success story, we believe the ultimate sizes of the shale basins in the United States have been overstated. In particular, we believe the Eagle Ford and Bakken shales are exhibiting their first signs of exhaustion. While the Permian Basin still has substantial development potential ahead, it cannot meet global demand growth alone.

(…) back in the fall of 2014 with oil prices at $70 per barrel, there were 270 rigs turning in the Eagle Ford and 190 rigs turning in the Bakken. Oil prices proceeded to fall by 65% before bottoming in February 2016 at $26 per barrel. Drilling activity bottomed a few months later in May with only 32 rigs turning in the Eagle Ford and 24 rigs turning in the Bakken (down 88% in both cases). Since then, oil prices have once again broken through $70 per barrel, however the rig count in each of these fields remains 65% and 70% below their Fall 2014 levels.

Drilling Activity in Eagle Ford and Bakken (2014 – 2018)

In the fall of 2014, the Permian basin had 560 rigs turning. Like the Bakken and Eagle Ford, drilling activity fell substantially and eventually bottomed in May 2016 nearly 80% below the fall 2014 level. However, as oil prices recovered to their late 2014 levels, drilling in the Permian has rebounded sharply and today stands only 15% below its late 2014 rate.

Drilling Activity in the Permian (2014 – 2018)

(…) Our analysis tells us that the only material difference between the plays is that the Permian has ample Tier 1 drilling inventory remaining whereas the Bakken and Eagle Ford are in the process of running out. If we are correct, we would expect to see production from the Bakken and Eagle Ford begin to disappoint in the quarters to come. (…)

This next item, only seen in the FT, could be a significant development for 2019

This next item, only seen in the FT, could be a significant development for 2019

Paal Kibsgaard, CEO of Schlumberger, said that in addition to a shortage of pipeline capacity that was slowing growth in the Permian Basin of Texas and New Mexico, the heart of the US shale boom, there were other problems that could mean some forecasts of future output would have to be revised down. (…)

“The well-established market consensus that the Permian can continue to provide 1.5 million barrels per day of annual production growth for the foreseeable future is starting to be called into question,” he said. (…)

Mr Kibsgaard said: “We are already starting to see a similar reduction in unit well productivity to that already seen in the Eagle Ford, suggesting that the Permian growth potential could be lower than earlier expected.”

Add the lack of pipeline to move the shale basin oil resulting in discounted prices which may incite producers to slow exploration and development until new capacity arrives, and we could have a period when the supply of U.S. shale oil could surprise negatively. Canadian producers are also stuck with deeply discounted oil thanks to pipeline shortages. All this right when we already have to deal with sharply lower supply from Iran and Venezuela.

The surprise could be much higher oil prices, often a silent trigger for economic troubles (e.g. 1974, 1980, 1990, 2007-08 and 2011. Emerging markets are already reeling from a strong USD. What if Brent gets to $100+?

TECHNICALS WATCH

Let’s start with one of Steve Blumenthal’s charts. The 13/34–Week EMA Trend Chart remains positive but both the 13W and 34W lines are now pointing down. They must cross downward for a bear signal.

Lowry’s Research continues to view the probabilities as “strongly” suggesting that the current market pullback represents “a normal pause in an ongoing bull market”.

However, it is seeing “some signs of a more selective rally that could be consistent with an aging bull market.” In particular, the percentage of mid and small cap stocks at New 52-week Lows showed a substantial increase at the Oct. 11th market low vs. the Apr. 2nd market low. “Small Caps clearly remain the weakest market segment, but weakness now may be showing signs of expanding into Mid Caps.” Pretty typical pattern eventually reaching larger caps. We have seen the same trend in earnings revisions in the past several weeks.

From my lens, I continue to worry, more than Lowry’s, about the trends in its Buying Power vs Selling Pressure indices. Buying Power peaked in early July and has been trending down since. Selling Pressure remained low until September 20 when it began to rise. The two lines are now close to crossing. As Lowry’s says, “a reversal of the short term convergent trends of Selling Pressure and Buying Power soon would be a welcomed further confirmation of the bull market’s endurance.”

Ned Davis Research also keeps tabs of supply and demand (shared by Steve Blumenthal):

(…) A sell signal occurs when the red line (selling volume) crosses above the black line (buying volume) and a buy signal when the black line crosses above the red line. (…) Not perfect. Some whipsaws but pretty darn good. (…) however, the two lines have yet to cross.

As you know, this is a game of probabilities. The two boxes in the above chart show positive odds for equity gains but as for Lowry’s indices, a reversal of the short term convergent trends soon would be a welcomed further confirmation of the bull market’s endurance.

NDR Daily Trading Sentiment Composite plunged last week from 38.89 to 26.67, pretty deep in the “Extreme Pessimism” range. Odds suggest that the best buying opportunities occur at “Extreme Pessimism” readings below 41.5.

Source: Ned Davis Research (via Steve Blumenthal)

Last Friday, the S&P 500 Index closed right on its 200dma which is dangerously flattening.

The equal weight index is weaker:

The equal weight index is weaker:

Mid-caps are through their declining 200dma. Beware.

Mid-caps are through their declining 200dma. Beware.

Small caps are through a still rising 200dma.

Small caps are through a still rising 200dma.

Same with the Russell 2000:

Same with the Russell 2000:

Canadian equities are looking bad, however cheap they may be:

The Nasdaq 100 index is taking its cue from the S&P 500, or vice versa:

EARNINGS WATCH

Package maker Sealed Air Corp. fell the most in six months Thursday after saying higher raw material costs would crimp the bottom line. A few days earlier it was rising freight outlays at Fastenal Co., where $1.1 billion of market value was erased. On Oct. 9, paint maker PPG Industries Inc. mentioned rising expenses. The shares cratered.

From railroads to retailers, signs of price pressures are starting to show at U.S. industrial companies, contributing to the worst October start for the S&P 500 since 2008. (…)

In a flat week for the S&P 500, old economy stocks bore most of the losses. Energy shares slid 1.9 percent, commodity producers lost 1.4 percent, and industrial companies fell 1 percent. (…)

Margin pressure has been one of many sagas in the industrial space of late. Earnings-related concerns going beyond rising costs have been leading to intermittent blowups around the industry for weeks, in companies from United Rentals to Textron Inc. and Snap-On Inc. Outside of the U.S., shares of Daimler AG fell Friday after the automaker issued its second profit warning in four months. (…)

Not to minimize the margins risk, I am actually very watchful for that. So far, it seems to be mainly a smaller cap problem.

We now have 84 S&P 500 company Q3 reports in and the beat rate is 79% with a beat factor of +4.1% (averaged +5.4% during the last 4 quarters). The revenue beat rate is 62% with a beat factor of +0.4% (averaged +1.3% during the last 4 quarters).

Q3 blended earnings are now seen up 22.2% (19.3% ex-Energy), up from 21.6% on Oct. 1.

Importantly, analysts have been more upbeat in their earnings revisions last week but mainly on large caps. Excluding S&P 500 companies, positive revisions were only 44% of all revisions last week:

Q4 estimates are +19.8%, down a little from +20.1% on Oct.1. Estimates for all of 2019 are unchanged at +10.2%.

Factset reports that, at this point in time, 13 companies in the index have issued EPS guidance for Q4 2018 with 9 having issued negative EPS guidance. The percentage of companies issuing negative EPS guidance is 69%, which is below the 5-year average of 71%.

Trailing EPS now stand at $155.77 or about $158.25 pro forma the tax reform for 12 months.

This week will see 160 reports to take us to the mid-point of the season.

Coming back to the above Bloomberg headline, it is interesting to note that the Vanguard Industrials ETF is down 9.7% during the last 4 weeks, in spite of the fact that 75% of the 16 S&P 500 industrial companies that have reported Q3 have exceeded estimates by 1.7% and the sector still boasts a 17% blended earnings growth rate for Q3, unchanged from Oct. 1.

As for industrial margins, Factset’s numbers show that Q3 Industrials’ margins will average 9.9% in 2018, up from 9.1% in 2017 with 77% of industrial companies reporting improved margins (70% for the whole S&P 500).

But the VIS is not acting well. Double top and declining 200dma. The higher low better hold…

Nervous market.

LOVE IT!

“Smart Money”! Good grief! The S&P 500 Index bottomed at 666 on March 6, 2009.

“Smart Money”! Good grief! The S&P 500 Index bottomed at 666 on March 6, 2009.

Interest in Midterms Surges, Along With Trump Approval Rating Voter interest in the midterm elections has surged to records within both parties, pointing to an energized electorate, a new WSJ/NBC News poll has found.

(…) Nearly two thirds of registered voters showed a high level of interest in the election—the highest ever recorded in a midterm election since the Journal/NBC poll began asking the question in 2006. (…)

Hand in hand with Republicans’ increased election interest is a rise in Mr. Trump’s job-approval rating to 47%, the highest mark of his time in office, with 49% disapproving of his performance. That is an improvement from September, when 44% approved and 52% disapproved of his performance.

Democrats still lead on the question of which party should control Congress. Among poll respondents identified as likely voters, 50% prefer Democrats, while 41% prefer Republican control, about the same as in last month’s poll. Among all registered voters, a broader group of respondents, Democrats’ advantage over the GOP is narrower—48% to 41%. (…)

Although Democrats are preferred in the national poll overall, their advantage has vanished in the House districts that matter most. In districts rated as the most competitive by the nonpartisan Cook Political Report, the parties are dead even on the question of which one should control Congress. In last month’s poll, Democrats led by 13 percentage points among registered voters and six points among likely voters. (…)

One matter of broad national consensus emerged from the poll: 80% said the U.S. today was a divided country, and 90% said the political divisions between Republicans and Democrats are a problem. (…)

From Bloomberg this morning:

President Trump surprised other Republicans this weekend by promising a middle-income tax cut before the midterms. Top party officials weren’t aware they were working on one and Congress is out of session until after the elections. The president is trying to boost his party’s chances of holding its Congressional majorities, and will attend a rally in Houston today to support Senator Ted Cruz, who faces an unexpectedly close re-election race.