The U.S. economy added 256,000 jobs last month and the unemployment rate edged down, the Labor Department said Friday.

December’s gain in nonfarm payrolls was well above the 155,000 jobs that economists had expected, according to a Wall Street Journal survey. The 4.1% unemployment rate was also better than the expected 4.2%.

The results were the latest sign that the U.S. labor market has recovered from its midyear stumble and may even be gaining steam. But Friday’s job report also shuts the door on a rate cut at the Federal Reserve’s next meeting, which is Jan. 28-29, and reduces the chances of a cut at its subsequent meeting in March. (…)

Perfect!

Financial markets did not see it that way but, in most, if not all aspects, Friday’s employment report was perfect.

Monthly data can be volatile and confusing and subject to bizarre seasonal adjustments. For example, job growth rebounded in the retail trade sector in December (+43k) following November’s decline, a +72k swing, likely reflecting the reversal of residual seasonality from a later-than-usual Thanksgiving holiday:

But smoother quarterly data reveal the real trend: the labor market has stabilized in Q3 and Q4 at +155k/month on average. Not too hot, not too cold.

The stacked MoM contributions from the 3 components of labor income has also stabilized at about +0.4% or 5.0% annualized, thanks to stable wages:

Last 4 months of 2024:

- employment growth averaged 155k per month, a stable 1.4% annualized rate. Weekly hours are steady.

- total hourly earnings rose 4.0% a.r., slowing to +3.9% in the last 2 months and +3.4% in December when they were up 3.9% YoY, stable since August.

- service-providing wages rose 4.1% a.r., slowing to +3.9% in the last 2 months and +3.1% in December when they were up 3.9% YoY, stable since October.

Wages for production and non-supervisory employees are growing more slowly, up 3.8% YoY in December, down from 4.0% in October. Services wages: +3.7% YoY in December.

Labor income keeps growing at a 5.0% nominal rate with employment contributing 1.4% and wages 3.5%, compatible with inflation around 2.0% given 1.5% productivity growth.

Importantly, the fear that services wages would linger or rise above 4.0% and boost inflation is dissipating, confirming what PMI reports have been saying in recent months. Demand for services is strong (employment +231k in December) but wages are not exploding, actually now growing at less than 4.0%.

December CPI is out Wednesday. Wells Fargo sees core CPI up 0.2% after +0.3% in November with services up 0.3% (after +0.27%). This would reassure investors that we might be in a slowflationary growth economy thanks to rising productivity.

Which ties with what follows:

AI CORNER

We are getting more and more real world examples of AI applications

Artificial intelligence agents have emerged as one of the most exciting aspects of generative AI for business because they take chatbots to the next level, performing complex tasks without help from humans.

These autonomous AI agents can follow instructions and do things from checking a car rental reservation at the airport to screening potential sales leads.

Software companies from Salesforce to ServiceNow, Microsoft and Workday last year all announced their own AI agents, which they say can help businesses be even more hands-off in areas like recruiting employees, contacting potential sales leads, creating marketing content and managing their information-technology.

If these AI agents work as promised, they could also provide businesses with the return on investment they have been looking for out of generative AI. According to some corporate technology leaders, that means the ability to tie the technology to a reduction in the number of hours employees work, or even how many new people they need to hire. (…)

By 2028, at least 15% of daily business decisions will be made autonomously through agentic AI—up from 0% in 2024, Gartner said. But, also by that time, 25% of enterprise breaches will be tied to AI agent abuse. (…)

At New Jersey-based Johnson & Johnson, AI agents are being used to help the healthcare giant with the chemical synthesis process in drug discovery. (…)

Without the help of these technologies, J&J’s scientists would go through multiple iterations of the same process manually, ensuring the right conditions are in place to optimize the switch. (…)

AI agents are becoming key players in research at Moody’s, the New York-based financial analysis and software company.

Many aspects of research, including industry comparisons and looking at companies’ Securities and Exchange Commission filings, were already outsourced to lower-cost areas outside the U.S., said Nick Reed, the company’s chief product officer. Now, some of that work is being done by autonomous AI agents—specifically those that work in conjunction with other agents.

The company has developed a total of 35 agents, some for smaller tasks like project management, and linked them up with agents for supervising them, creating what Reed calls a “multi-agent system.”

Moody’s agents are given specific instructions, personalities and access to data and research. As a result, they can come to different conclusions, especially for complex topics like analyzing the financial fitness of a company that appears healthy, but is facing geopolitical risk. (…)

EBay is using AI agents to help write code and create marketing campaigns. The company also plans to roll out agents that can help buyers find items and sellers list goods. (…)

As its agents become more sophisticated, they’ll be able to act more autonomously—writing more code on their own, line by line, as human developers would, he added. (…)

Telecommunications giant Deutsche Telekom, which has roughly 80,000 employees in Germany, has rolled out an AI agent for its employees to ask any question about internal policies and benefits, and for its service staff to ask questions about its products and services. (…)

The Spanish company Cosentino, which makes countertop surfaces and other stone materials for homes and buildings, has brought on a “digital workforce” of AI agents to fill the gaps in its customer service staff, said Rafael Domene, the company’s CIO. (…)

Now, its “digital staff” have entirely replaced the work of three to four people previously involved in clearing customer orders, and those staff are focusing on other areas of service, according to Domene.

Want to know more about “agents”? The new wave: Agentic AI

The KPMG Quarterly Pulse Survey captures perspectives from 100 U.S.-based C-suite and business leaders representing organizations with an annual revenue of $1 billion or more.

Most leaders (67%) expect AI to fundamentally transform their businesses within the next two years. (…) “The data also shows growing momentum around AI agents, with over half of organizations exploring their use. Leaders are putting real dollars behind agents, but with mounting pressure to demonstrate ROI, getting the value story right is critical.” (…)

Over half (51%) of organizations are exploring the use of AI agents today. Leaders expect to utilize the capability for administrative duties (60%), call center tasks (54%) and to develop new business materials (53%) within the next 12 months. Yet, we are still in the early stages of implementation as only 12% are deploying AI agents currently. (…)

Half of leaders are currently scaling their GenAI technology, up from 10% six months ago. However, only a third (31%) of leaders anticipate being able to measure ROI in the next six months, and as of today, none believe they have reached that stage in their GenAI implementation.

“The dynamic nature of AI demands new ways to measure value—beyond the limits of a conventional business case. As leaders work to define the right metrics, those measures must be tightly aligned with the business strategy and should account for the cost of not investing,” Chase continued. (…)

More than 80% are planning to include GenAI as part of their organization’s formal performance development track. Yet just a quarter (24%) of employees are currently leveraging AI embedded into existing workflows (…).

Productivity is now the top ROI metric (79%) for the first time since Q1 2024. Profitability is a close second and increased more than any other metric from Q1 to Q4, jumping from 35% to 73%. (…)

Today, only 7% of organizations have appointed board members with GenAI expertise, although 91% plan to do so. (…)

Employee adoption is a top three challenge in 2025, and 81% of leaders are planning on including GenAI in their performance reviews,19% are doing so already.

54% of organizations are using GenAI productivity tools at least once a week. Another 24% are using GenAI embedded into existing workflows at least once a week.

(…) While most organizations (76.2%) report that they have been using earlier forms of AI, such as machine learning, for more than three years, it has been the arrival of generative AI that has fueled the rapid growth of AI utilization and adoption. This year’s survey findings suggest that we are experiencing a once-in-a-generation transformational moment, akin to the founding of the internet in the 1990s. (…)

Even with fears of disinformation, misinformation, potential job displacement, risk of ethical bias, and other concerns, 96.6% of organizations see the overall impact of AI as beneficial. In fact, this year seemed to convince many leaders that AI is, in fact, the real deal, with 89.0% reporting that AI is expected to be the most transformational technology in a generation, up from 64.2% in last year’s survey.

- 98.4% of organizations said that they were increasing investments in AI and data, up from 82.2% last year. In addition, 90.5% say that AI and data investments are a top priority, up from 87.9%.

- 93.7% report that they’ve seen some business value from their AI investment, meaning that they are seeing quantifiable business results, which can be measured by metrics including increased customer acquisition and retention, improved customer satisfaction, and revenue and productivity improvements.

- The source of this value is significant: 74.8% see it as coming from productivity gain and customer service improvement, notably through efficiencies resulting from the application of generative AI into traditional production processes.

- 23.9% reported implementing AI in production at scale this year, up from just 4.9% last year.

- This year marked the appearance of the chief AI officer as a rapidly emerging role, with 33.1% reporting having now filled this role, and 43.9% saying that a chief AI officer should be appointed at their organization.

- A growing percentage of AI and data leaders (36.3%) now report to the most senior business leadership of their organization: the CEO, president, or COO. This signifies a recognition that reliance on data has become increasingly central to all aspects of corporate decision-making. (…)

Thankfully, David is immersed in AI deployment. He found a recent Carnegie Mellon University paper which attempts to measure the actual usefulness (ROI) of AI uses:

(…) To measure the progress of these LLM agents’ performance on performing real-world professional tasks, in this paper, we introduce TheAgentCompany, an extensible benchmark for evaluating AI agents that interact with the world in similar ways to those of a digital worker: by browsing the Web, writing code, running programs, and communicating with other coworkers. We build a self-contained environment with internal web sites and data that mimics a small software company environment, and create a variety of

tasks that may be performed by workers in such a company. We test baseline agents powered by both closed API-based and open-weights language models (LMs), and find that with the most competitive agent, 24% of the tasks can be completed autonomously.

(…) Unsurprisingly, current state-of-the-art agents fail to solve a majority of the tasks, suggesting that there is a big gap for current AI agents to autonomously perform most of the jobs a human worker would do, even in a relatively simplified benchmarking setting. (…) tasks that involve social interaction with other humans, navigating through complex user interfaces designed for professionals, and tasks that are typically performed in private, without a significant open and publicly available resources, are the most challenging.

However, we believe that currently new LLMs are making significant progress: not only are they becoming more and more capable in terms of raw performance, but also more cost-efficient. Open-weights models are closing the gap between proprietary frontier models too, and the newer models are getting smaller (e.g. Llama 3.3 70B) but with equivalent performance to previous huge models, also showcasing that efficiency will further improve. (…)

AI is also increasingly used in Asia:

Singapore’s Atlas, a B2B travel technology provider, utilizes Alibaba Cloud’s LLM Qwen and Model Studio platform for its digital chatbot that offers 24/7 customer support, addressing partner inquiries related to booking processes and payment options while achieving a 45% reduction in operational costs.

Drunk Elephant, a skincare brand acquired by Shiseido in 2019, deployed Alibaba Cloud’s latest foundation model Qwen-max in its customer chatbot to enhance customer interactions in China.

David also monitors progress in LLMs throughout the world. He sees Chinese models performing very well, at lower costs, against Western LLMs in spite of their technological challenges. Contrary to most Western models, Chinese LLMs are open source, allowing for better collaboration and faster innovation at reduced costs.

In late 2023, Bloomberg argued that “without adequate processing power Alibaba cannot hope to compete in the AI arena (…)”.

In 2024, Alibaba unveiled a full-stack AI infrastructure with optimized computing efficiency, achieving over 99% model training efficiency and 20% improved resource utilization. It also introduced CUBE DC 5.0, a next generation data center architecture that reduces deployment times by up to 50%.

BABA has had 5 consecutive quarters of triple-digit AI-related revenue growth per its Q3’24 earnings report. It has a 7.9% global cloud market share (AWS 39%, MSFT 23%) but holds a 39% share of China’s cloud market and is challenging Western companies in all markets (other than North America) with high performance and low prices.

Forrester says that Alibaba offers a “powerful cloud-native infrastructure into more accessible offerings for both developers and operators, with data and analytics as a standout. It is a good fit for Chinese-based enterprises or international corporations requiring cloud scale across APAC and parts of Africa, Europe and Latin America.”

Ethan Mollick, the co-director of the Generative AI Labs at the Wharton School at the University of Pennsylvania, last December 19:

The last month has transformed the state of AI, with the pace picking up dramatically in just the last week. AI labs have unleashed a flood of new products – some revolutionary, others incremental – making it hard for anyone to keep up. Several of these changes are, I believe, genuine breakthroughs that will reshape AI’s (and maybe our) future. Here is where we now stand. (…)

A bombshell of a medical working paper from Harvard, Stanford, and other researchers concluded that “o1-preview demonstrates superhuman performance [emphasis mine] in differential diagnosis, diagnostic clinical reasoning, and management reasoning, superior in multiple domains compared to prior model generations and human physicians.” The paper has not been through peer review yet, and it does not suggest that AI can replace doctors, but it, along with the results above, does suggest a changing world where not using AI as a second opinion may soon be a mistake. (…)

We have had AI voice models for a few months, but the last week saw the introduction of a new capability – vision. Both ChatGPT and Gemini can now see live video and interact with voice simultaneously. For example, I can now share a live screen with Gemini’s new small Gen3 model, Gemini 2.0 Flash. You should watch it give me feedback on a draft of this post to see what this feels like.

Or even better, try it yourself for free. Seriously, it is worth experiencing what this system can do. Gemini 2.0 Flash is still a small model with a limited memory, but you start to see the point here. Models that can interact with humans in real time through the most common human senses – vision and voice – turn AI into present companions, in the room with you, rather than entities trapped in a chat box on your computer. The fact that ChatGPT Advanced Voice Mode can do the same thing from your phone means this capability is widely available to millions of users. The implications are going to be quite profound as AI becomes more present in our lives.

AI image creation has become really impressive over the past year, with models that can run on my laptop producing images that are indistinguishable from real photographs. They have also become much easier to direct, responding appropriately for the prompts “otter on a plane using bluetooth” and “otter on a plane using wifi.” If you want to experiment yourself, Google’s ImageFX is a really easy interface for using the powerful Imagen 3 model which was released in the last week.

But the real leap in the last week has come from AI text-to-video generators. (…) OpenAI released its powerful Sora tool and then Google, in what has become a theme of late, released its even more powerful Veo 2 video creator. You can play with Sora now if you subscribe to ChatGPT Plus, and it is worth doing, but I got early access to Veo 2 (coming in a month or two, apparently) and it is… astonishing. (…)

What’s remarkable isn’t just the individual breakthroughs – AIs checking math papers, generating nearly cinema-quality video clips, or running on gaming PCs. It’s the pace and breadth of change. A year ago, GPT-4 felt like a glimpse of the future. Now it’s basically running on phones, while new models are catching errors that slip past academic peer review. This isn’t steady progress – we’re watching AI take uneven leaps past our ability to easily gauge its implications. And this suggests that the opportunity to shape how these technologies transform your field exists now, when the situation is fluid, and not after the transformation is complete.

Exports rose 10.7% YoY in December in dollar terms, while imports climbed 1.0%. In November, exports rose 6.7% while imports declined 3.9%.

(…) Exports accounted for nearly a quarter of the economy’s expansion in 2024, although that support now faces external challenges from the US and other trade partners. (…)

Exports to the US rose to the highest in more than two years in December, hitting almost $49 billion and taking the total for the year to $525 billion.

The value of shipments to all markets rose almost every month last year, pushing it above the 2022 highs during the pandemic. Exports rose nearly 11% to $336 billion in December, the second-highest month on record and behind only December 2021, when Chinese firms saw a surge of pandemic-led demand. Outbound shipments for the whole of last year were worth $3.6 trillion. (…)

Efforts to dodge levies have also boosted exports to Southeast Asia, with shipments of electronic components to Vietnam soaring since the first trade war. The country overtook Japan as China’s third-largest export destination for the first time last year, driven mostly by a surge in shipments of electronics parts that are assembled and then exported to the US and elsewhere.

Despite shipping record amounts of goods, Chinese exporters have been getting less money for their products, with export prices falling for more than a year as deflation inside China gets worse and pushes down the cost of goods.

As a result, the growth in the volume of Chinese trade has outpaced value, with total export volumes rising 7.3% through November, according to the Ministry of Transport, faster than the 5.4% rise in values. (…)

The surplus with the US fell to $361 billion last year, the lowest in three years, but that was still well above the pre-pandemic levels. The surplus with the 10 Southeast Asian nations in Asean soared to a record, and that with the European Union rose to almost $250 billion. (…)

The FT reports that corporate profits in China for companies with more than Rmb20mn ($2.7mn) in revenue declined by an average of 4.7% YoY between January and November on revenues up 1.8%. One quarter of companies lost money in 2024.

State-owned companies’ profits fell 8.4% while private or foreign companies had a 1.0% decline. Deflation is tough to navigate.

EARNINGS WATCH

The Q4’24 earnings season begins this week but we already have the 22 early reporters: a 77% beat rate and a +4.9% surprise factor with aggregate earnings up 26.8% YoY on revenues up 5.3%.

Three months ago, the same companies (21 in fact) recorded a 76% beat rate and a +3.5% surprise factor with aggregate earnings up 23.8% on revenues up 2.7%.

Three months ago, analysts expected S&P 500 earnings to rise 5.0% on revenues rising 4.0%.

Today, in spite of more subdued pre-announcements, analysts are expecting earnings to rise 9.5% on revenues up 5.3%. Ex-Energy: +12.4% in Q4 after +11.8% in Q3.

Double digit growth forecasts persist throughout 2025.

Banks kick off the season Wednesday and Thursday facing a high bar of 18.0% earnings gains following +8.6% in Q3. Revenue growth is also sustained, actually accelerating from +4.8% ex-E in Q4’24 reaching +6.9% in Q4’25. Only Health Care and Utes will experience slowing revenue growth if analysts are right. No disinflation in those numbers!

Goldman Sachs warns that the bar for 4Q earnings season is elevated relative to recent quarters.

Consensus expectations for 4Q 2024 earnings growth are nearly the highest since 4Q 2021, exceeded only slightly by the expected 9% year/year EPS growth ahead of 2Q 2024 earnings season. Over the last 11 quarters, realized S&P 500 EPS growth has exceeded consensus estimates by a quarterly average of 4 pp. We expect that corporates will continue to report solid earnings growth this quarter but that the magnitude of beats will likely be smaller than in recent quarters given the higher bar.

The S&P 500 trailing earnings are now $241.94. Full year 2024: $243.34e. Forward EPS: $272.92e. Full year 2025: $273.91e.

The P/E is now 24.0x vs 21.8x at the end of 2023 and 2022 respectively. We sure need good earnings growth this year.

The Rule of 20 P/E is 27.3 on trailing earnings with inflation at 3.3%.

This 36% overvaluation (from 20.0) shrinks to 18% using 2025 EPS and inflation of 2.5%, two rather optimistic but not blue sky forecasts.

The spread between the blue (S&P 500) and yellow (R20 Fair Value) lines above is the graphic measure of the overvaluation from the long term median R20 value (20.0). Valuation per se is not a timing tool but the trend in the R20 Fair Value has generally been critical.

Positive earnings growth amid a slowflation environment could keep equity markets buoyant. A cautious Fed, mindful of inflation but not overly restrictive is thus preferable to one too lenient or too hawkish.

TECHNICALS WATCH

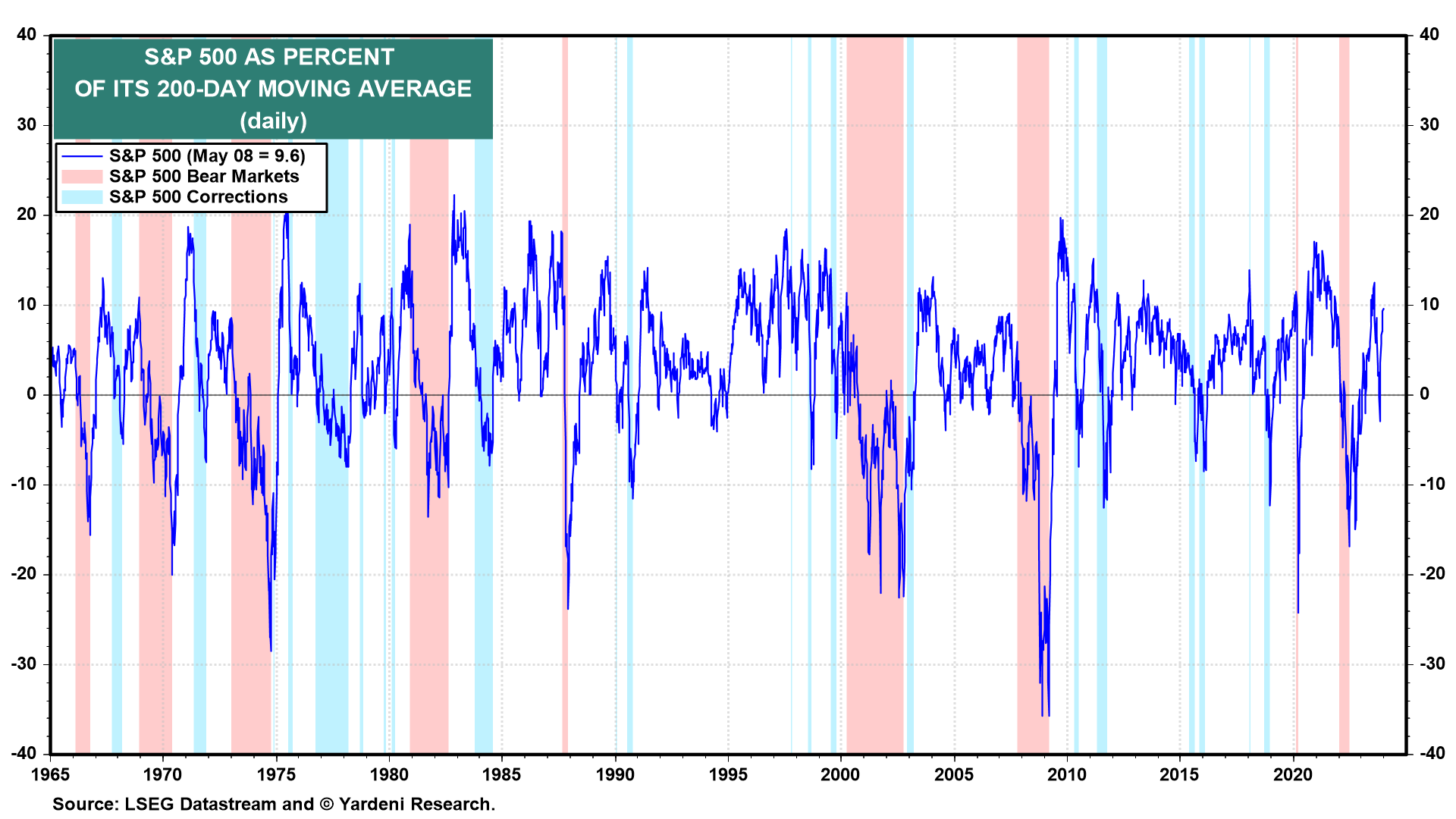

The S&P 500 has a habit of at least correcting to its 200-day moving average (now 5572)…

… but not once in 2024. In April and September, the setback stopped at the 100-dma, currently 5820:

FYI

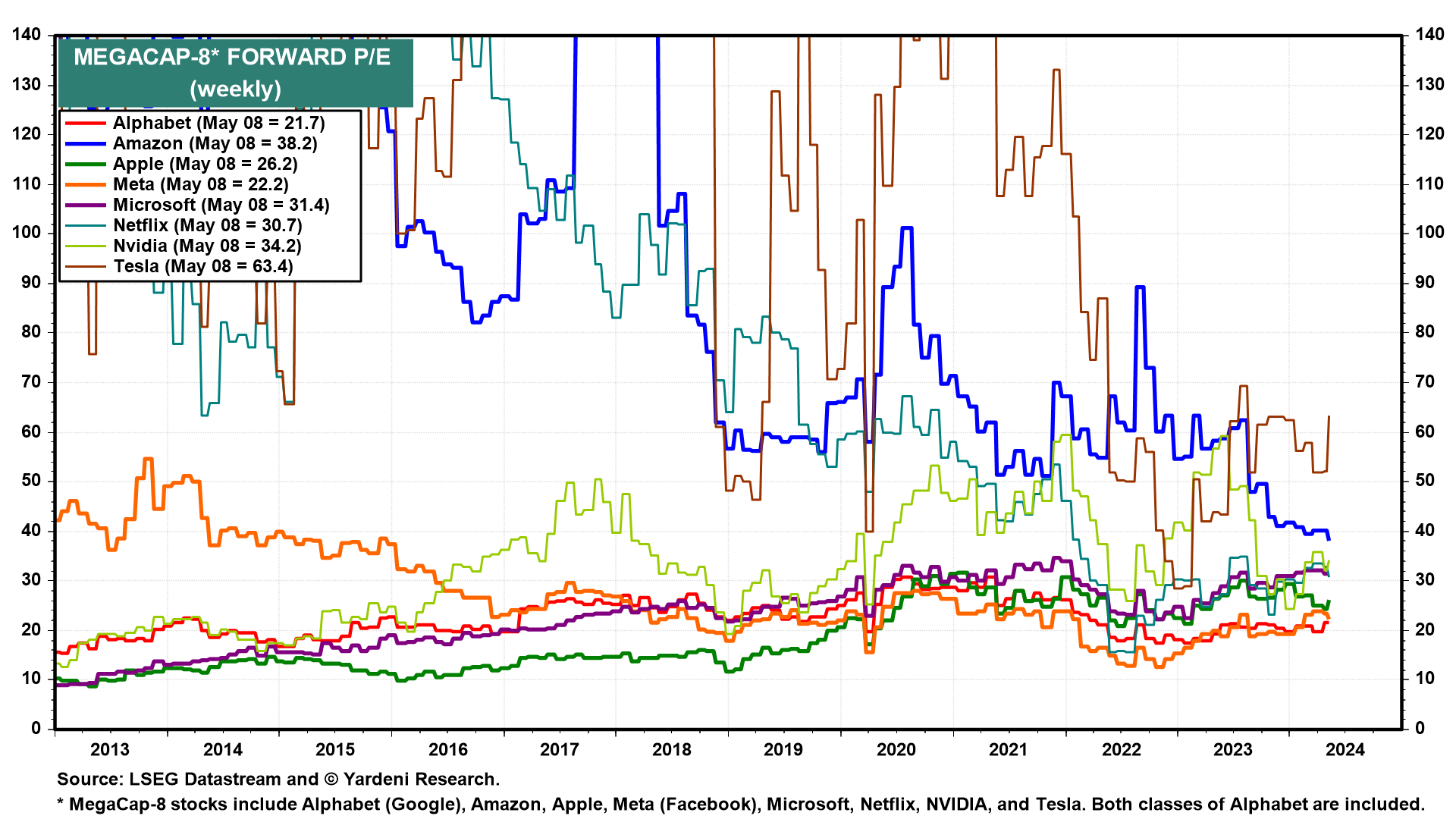

- NVDA is 2.7% above its 100-dma and 12.2% above its 200-dma ($119).

- GOOG is 10.4% above its 100-dma and 10.8% above its 200-dma ($119).

- AMZN is 9.2% above its 100-dma and 12.7% above its 200-dma ($119).

- AAPL is 1.7% above its 100-dma and 9.0% above its 200-dma ($119).

- META is 7.1% above its 100-dma and 13.7% above its 200-dma ($119).

- TSLA is 24.4% above its 100-dma and 37.8% above its 200-dma ($119).

- MSFT is 1.3% below its 100-dma and 1.5% below its 200-dma ($119).

All these moving averages are still rising except MSFT which is also the only stock on that list showing flattening exponential moving averages, indicating a potential major change in direction:

(Ed Yardeni)

(Ed Yardeni)

Between 1950 and 2021, the first quarter post elections has been wobbly for equities:

@granthawkridge

@granthawkridge

But how useful are these S&P 500 stats when the top 10 stocks account for 38.5% of the index:

@edclissold

Ed Yardeni:

(…) Some of these pullbacks, which are 5%-10% declines, could turn into corrections of more than 10% but less than 20% this coming week if Tuesday’s CPI inflation rate for December is higher than expected, causing the 10-year Treasury bond yield to revisit 2023’s high of 5.00%. (…)

The buying opportunity in stocks and bonds might be better after Inauguration Day when President Donald Trump is expected to sign a bunch of Executive Orders covering tariffs, deportation, deregulation, taxes, and energy. One of the reasons that bond yields rose on Friday, in addition to the strong jobs report, was the reported increase in consumers’ short-term and long-term inflation expectations so far during January. That suggests consumers expect higher tariffs to boost inflation. to